Heavy Is the Head That Wears the Crown

Exploring the "kingmaking" fallacy in venture capital; the notion that more capital can increase the odds of startup success.

“The fact is that the amount of money start-ups raise in their seed and Series A rounds is inversely correlated with success. Yes, I mean that. Less money raised leads to more success. That is the data I stare at all the time.”

As venture capital moves through cycles of hot and cold markets, investors often find themselves wondering whether they should keep pace with the market. This is particularly true in categories where rounds are the most competitive and prices are at their highest.

Essentially, is “paying up” for access to hot companies worthwhile? Can participating in outsized rounds be justified with the “kingmaking” logic, that a exceptionally well capitalised startup has a better shot at success?

On one hand, venture capital is a contrarian sport, where returns are won by making investments in categories that are overlooked and underfunded. On the other hand, there’s the temptation to optimise for momentum and downstream investment, by choosing categories with greater interest and higher velocity.

Data from four sources, covering various parts of the startup life-cycle, suggest that the disciplined investor probably comes out ahead; high prices are often a red flag. This overlaps with a variety of principles about the psychology of resources management, optionality, and risk management.

The Principle of Least Commitment

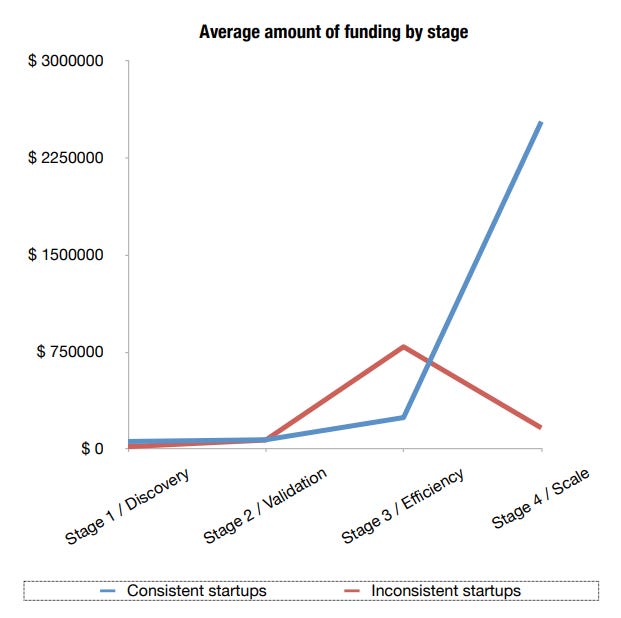

One of the major features of young startups is their flexibility and adaptability. Founders must experiment in order to find true product:market fit, which often requires a major pivot of the initial vision. In fact, there’s even evidence that executing a pivot may be a positive indicator for future success, reflecting a founder’s ability to exploit this flexibility.

This is where greed at the earliest stages can become problematic. If startups are able to raise an irrational amount of capital due to hot market effects, they often end up overinvesting in development or hiring in a way which makes them brittle.

“The more you raise, the more you spend, and spending a lot of money can be disastrous for an early stage startup. Spending a lot makes it harder to become profitable, and perhaps even worse, it makes you more rigid, because the main way to spend money is people, and the more people you have, the harder it is to change directions.”

This effect was confirmed in a comprehensive study by Startup Genome, which spun out of a wider project analysing the major causes of failure in 3,200 early stage companies. The phenomenon of raising too much capital and growing certain dimensions more quickly than others (e.g. overhiring without the appropriate revenue growth), referred to as “Premature Scaling”, was present in 70% of the cases they examined.

This finding was replicated in another report out of Zayed University, looking at the relationship between the amount of capital raised and the ultimate valuation of the company.

“The findings suggest that there is a U-shaped relationship between the amount of capital raised and post-money valuation, indicating that while capital funding has an overall positive effect on market valuation, raising too much capital has a negative impact.”

The Impact of Funding on Market Valuation in Technology StartUp Firms, by Amril Nazir and Dina Tbaishat

The conclusion here is simply that startups shouldn’t raise too little, as they must be able to run experiments and build what they need to hit the next milestone. Equally, they shouldn’t raise too much, as they need to remain disciplined and flexible.

It’s tempting to believe that you could keep that money in the bank, de-risking the company, but the truth is that you’ll be under pressure to spend on growth, whether you are ready or not.

Indeed, risk increases with capital raised when that capital is treated as a debt against future expectations. It is far more beneficial to raise minimally, and retain maximum optionality at the earliest stages. In AI research circles, this concept is referred to as the principle of least commitment.

“The least commitment principle is one of several strategies people use when they make plans, such as preparing for a day’s outing. The principle gained currency in the 1980s in the early days of artificial intelligence research. It simply means to prioritise tasks in such a way that you keep certain decisions about resources and timings as open as you can for as long as possible.

In computational terms the principle means the sequence of tasks you want to plan for has a large number of variables with interacting and conflicting constraints. Keep as many variables open, vague and with as wide a range of values as possible. The principle assumes that the creation of a plan is a search process. At some stage in the search you are bound to strike certain constraints that decide parts of the task sequence. The less constrained tasks simply fall into line.”

Raise and deploy righteous capital with Odin; fund administration for builders on the frontier.

The Principle of Indifference

“There will be certain points of time when everything collides together and reaches critical mass around a new concept or a new thing that ends up being hugely relevant to a high percentage of people or businesses. But it’s really really hard to predict those. I don’t believe anyone can.”

It’s tempting to believe that the best outcomes are known, long before they make it to an exit. In every cycle, category winners are called based on fundraising signals and rapid markups. However, these companies may end up just being early pioneers, like the internet search engines of the 90s, that will be passed by “fast followers” further down the line.

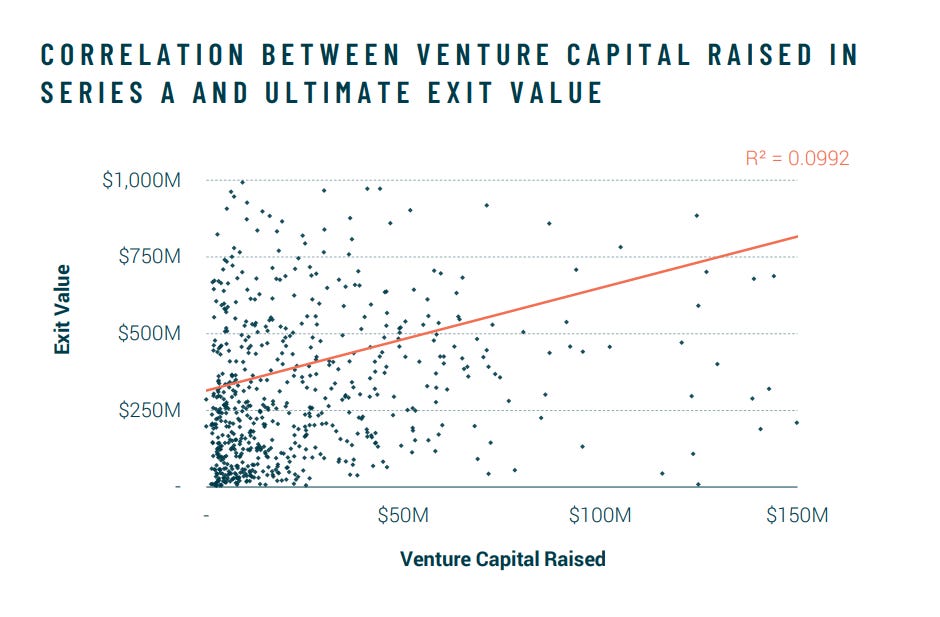

There’s also a problem of selection bias, where investors pile into high-performing companies and drive up the price, leading many to believe that a high price is indicative of performance. For this to make sense, round size growth would have to correlate with probability of future success. Otherwise, investors are just bidding-up the price and eroding their future returns.

So, does early round size have a meaningful correlation with success? According to analysis by Santé, looking at data from 1,980 exits, it would appear not.

None of this should be surprising to anyone with a good grasp on the risk that is being managed. If outcomes were so predictable, where paying more would produce a meaningfully greater likelihood of success, venture capital would have a radically different distribution of outcomes. In fact, the venture industry as we know it would be largely unnecessary.

Simplified, this is the principle of indifference. If you cannot honestly judge the likelihood of different outcomes then you must apply equal probabilities to all. In a venture capital context, that would imply all seed investments should be priced similarly, because price should follow probability. Unfortunately, investors often behave as if probability follows price.

“The principle of indifference, also known as the principle of insufficient reason, is attributed to Jacob Bernoulli, and sometimes to Laplace. Simply stated, it suggests that if there are n possible outcomes and there is no reason to view one as more likely than another, then each should be assigned a probability of 1/n. Quite appropriate for games of chance, in which dice are rolled or cards shuffled, the principle has also been referred to as the “classical” approach to probability assignments.”

The Principle of Indifference, by Cambridge University Press

The Paradox of Plenty

The problem of overcapitalisation is consistent all the way through the life of a company, not just at early stages. Indeed, research out of the University of Beijing’s School of Finance indicates, there’s a similar convexity in pre-IPO growth.

“Our results suggest that pre-IPO growth only improves the post-IPO long-run performance to a saturation point, above which pre-IPO growth negatively influences the post-IPO long-run performance. In other words, firms with lower or higher pre-IPO growth do not achieve better post-IPO long-run performance. Instead, it is the middle-level growth prior to IPO that is significantly related to the best post-IPO long-run performance.”

Pre-IPO growth, venture capital, and the long-run performance of IPOs, by Jiangjing Que and Xueyong Zhang

Essentially, there is a minimum scale at which IPOs perform well and provide a solid foundation for future growth. However, there’s also a point at which an IPO might be oversized, which is reflected in a slower growth and a less appealing opportunity for public market investors.

This appears to be connected to the amount of venture capital raised by large firms, leading to a similar problem of brittle overinvestment to that studied in early-stage companies.

“We find that the VC backed IPOs underperform non-VC backed IPOs, especially when firms have high excess cash, and propose that the higher excess cash retained in VC backed firms at IPO date may result in wasteful investment. Post-IPO real investment also confirms this notion.”

Do venture capitalists improve the operating performance of IPOs?, by Hung-Kun Chen and Woan-lih Liang

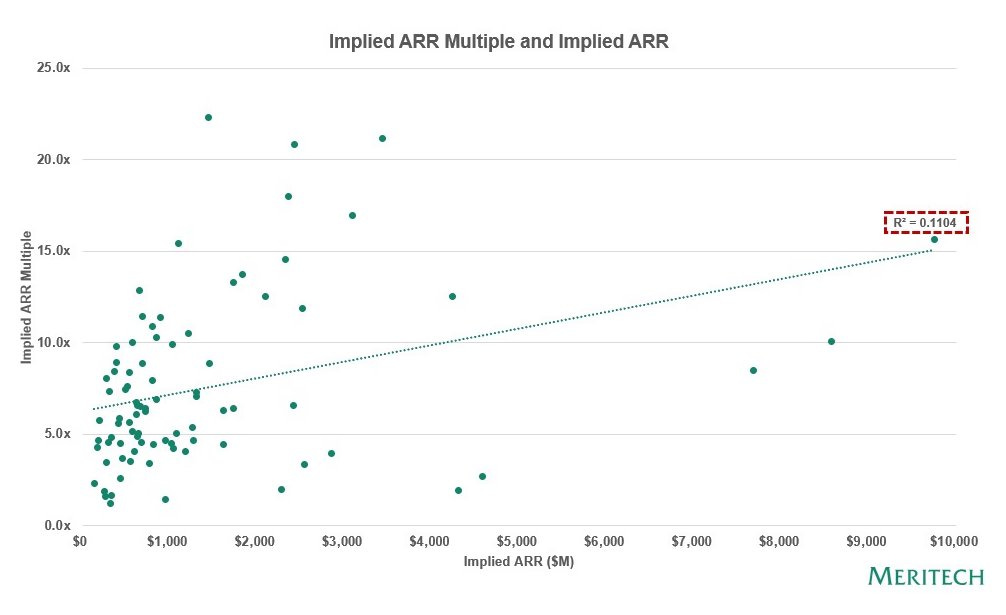

Again, this stems from a problem of selection bias, where high-performing firms often have more revenue, but more revenue does not necessarily indicate high performance. Private market investors misunderstand this, behaving as if scale supersedes other critical factors like defensibility, growth rate and profitability, and so overoptimise around scale (which has conveniently enabled larger funds).

Indeed, there’s relatively little correlation between implied ARR and the resulting ARR multiple at IPO, which would reflect a “scale premium”, and what little there is can be explained by selection bias.

So when is the right time to go public? The answer is a trade-off between scale and growth. You need to be large enough that the costs are manageable, but small enough that your growth rate remains appealing. Additionally, you need to at least indicate the potential for improving economics over time, which is often where cash incinerating venture-backed companies struggle.

“Be mindful that the public markets want fast (and durable) growth rates, improving margins, and a path to profitability (not just free cash flow positive but GAAP operating profit eventually) i.e. ‘Can you make money?’

While companies don’t need to be at $1B of ARR or revenue, you should have at least $250M of ARR or $200M in trailing revenue. Are you growing revenue 30-40%+ year-over-year with improving free cash flow margins? Is your growth rate durable? Are you a Rule of 40 business?”2024: When to IPO in the Age of Uncertainty, by Alex Clayton and Cathy Choi

In short, larger growth rounds will produce inflated exits, but they happen much later in a companies life and appear to lead to negative consequences post-IPO, including slower innovation, higher rates of failure, more fraud and weaker performance.

This is emphasised by the fact that aggressive post-lockup selloffs are associated with overvaluation, and this appears to be a particular issue for venture-backed IPOs. More than any other category of company, insiders in venture-backed companies are keen to exit their position as soon as they possibly can.

“The authors show that the IPO lockup period price reduction is strongly related to overvaluation. Zero-investment portfolios long in the lowest overvaluation quintile and short in the highest overvaluation quintile of IPO firms have positive significant returns.”

IPO overvaluation and returns prior to lockup expiration, by K. Stephen Haggard and Yaoyi Xi

The performance problems connected to overfunding relate to a broad body of research on the paradox of plenty, which looks at how resource availability changes outcomes at all levels of application, from the individual to the state.

To repeat the theme of this article, this research demonstrates a convex relationship where it is helpful to be sufficiently resourced that you can handle risk, but not so well-resourced that you become complacent.

“This article suggests that there is an inverse U-shaped relationship between slack and innovation in organizations; both too much and too little slack may be detrimental to innovation. Two related mechanisms governing this relationship are proposed: Slack fosters greater experimentation but also diminishing discipline over innovative projects, resulting in the hypothesized curvilinear relationship. Comprehensive worldwide data on 264 functional departments of two multinational corporations support the prediction.”

Is Slack Good or Bad for Innovation?, by Nitin Nohria and Ranjay Gulati

Cui bono?

Given all of the above, demonstrating that “more” is categorically not “better”, who actually benefits from kingmaking?

In practice, it’s a strategy that consumes vast sums of capital, accelerates price inflation of private companies, and enables oversized IPOs.

All of this would imply that the beneficiaries of kingmaking are the scaled venture capital firms, whose central challenge is rapidly deploying large pools of capital and generating attractive performance metrics. They’re also often the firms who promote the legitimacy of this strategy in relation to their favoured portfolio companies.

At best, kingmaking is a lazy narrative device designed to scare off competition. At worst, it’s a shallow justification for larger funds, fabricated performance and less disciplined investing.

Importantly, it serves these purposes at a cost to the long-term success of founders and their companies, which is unforgivable.

The best path, for founders who are building a generational company, is to work with investors who understand the existential importance of capital efficiency.

“I think frugality drives innovation, just like other constraints do. One of the only ways to get out of a tight box is to invent your way out.”

Raise and deploy righteous capital with Odin; fund administration for builders on the frontier.

Very insightful. Are there any studies shedding light on what "optimal capitalisation" would look like?