Private 🛑

Thoughts on opening the private equity and venture capital markets to retail investors.

Hi folks, Patrick Ryan here from Odin. We are building the ultimate tool for angel syndicates to invest together in private companies and funds, via SPVs.

For over 40 years, leading thinkers and writers have been documenting the exponential forward march of information technology, and the opportunities and risks it represents (See Altman (2021); Kurzweil (2001); Buckminster-Fuller (1981).

There is one impact of this accelerating change that we are all too aware of: the rise of startups and venture capital.

Silicon Valley is the Athens of our time. You can barely read a page in a business newspaper nowadays without seeing something about unicorns, Series-C funding or Google's latest acqui-hire.

Everyone from hedge funds to big corporates are going after the VC market, hunting for elusive unicorn fairy dust.

Why are we so obsessed with tech? Is it just a fad? Is it a bubble?

Maybe. But something deeper and longer-term is also happening…

The ever-accelerating pace of change driven by computing power (Moore's Law), combined with the "winner takes most" tendency of tech is forcing a radical redesign of capitalism in real time. The consequences are unrolling before our very eyes:

Software is eating the world.

Tech companies are using computing to automate increasing amounts of work. This effectively means that if you don't own equity in a business (preferably a technology business), you'll be poorer in future, in relative terms. This is because labour (which you currently sell for money) will be done by robots. This process is already well underway. As Sam Altman puts it, "power is shifting increasingly from labour to capital."People can sense this viscerally, and they feel a mixture of panic and excitement.

This explains Tesla, Bitcoin, Gamestop, the rise of equity crowdfunding and everything in between. They are attempts by the everyman to get a seat at the table and a share of the spoils.This problem is further compounded by macroeconomic circumstances.

Quantitative easing means the world is awash with money. It is being invested by the wealthy in financial assets, and they keep getting richer (relatively) as a result. I wrote about this in 'Elite Overproduction'.The ground is shifting beneath our feet.

The flurry of information and technological innovation coming at us faster and faster means nothing is certain or predictable. As a result, small, agile strike forces (startups) backed by walls of VC cash continue to be much better equipped to identify and capitalise on new opportunities than big, heavy tankers (corporations).New monopolies are being created.

Network effects, product embedding and increasing returns to scale - three of the defining characteristics of software companies that make them such attractive investments - have a tendency to create monopolies. This means that if you are an early shareholder in the right company, your shares have the potential to become so valuable you will never need to work again.Governments are currently unable to keep up with all of this.

They are legacy, 20th century institutions ill-equipped to handle the pace of change.

Taking a step back, something strikes me. The next twenty years - and perhaps the future long thereafter - will be shaped by three interacting forces:

Public policy

Big tech

Private equity

I am using "private equity" here as a catch all term for private markets investing - venture capital, growth equity, buyout, etc.

I’m not confident of public policymakers’ ability to catch up. As for big tech, it was actually produced by private equity.

So I believe the PE and VC market has a lot to answer for.

How capital is allocated, who allocates it, and who can even access the opportunities to invest in the first place had and will continue to have a huge impact on the world.

This decides what businesses get built and who owns them.

In today's essay, I want to continue examining an important question I ask myself every day - what is the best way to involve everyday people in this process?

I believe this is essential to building a future we can be proud of.

The Current Market

Startups are staying private much longer.

They are less hamstrung by the regulatory obligations of a publicly traded entity, not forced to deal with investors who don't know how to value them (or know they are overvalued) and better able to play their cards close to their chest. All of these factors allow them to maintain their edge.

Look at Stripe. Fintech's darling was valued at $95 billion in its most recent private funding round, putting the eleven year old company only $15 billion behind the market cap of Goldman Sachs, a 152 year-old financial services titan. I'm not saying Stripe doesn't have further to grow (I would be a fool to bet against the Collisons), but we are a long long way from Amazon's public listing at around $438m.

If you had invested in Amazon at IPO, you'd now be up about 3,000x. I can't see Stripe being worth $285 trillion any time soon (for context, that is well over 3x global GDP in 2019).

The investment behaviour driving this shift from public to private equity has been evolving for decades. The proportion of capital sitting in the private markets has been growing - at the expense of bonds and public equities - since the 80's.

Private equity AUM has grown more than sevenfold since 2002 and almost threefold since 2010, twice as fast as global public equity. Source

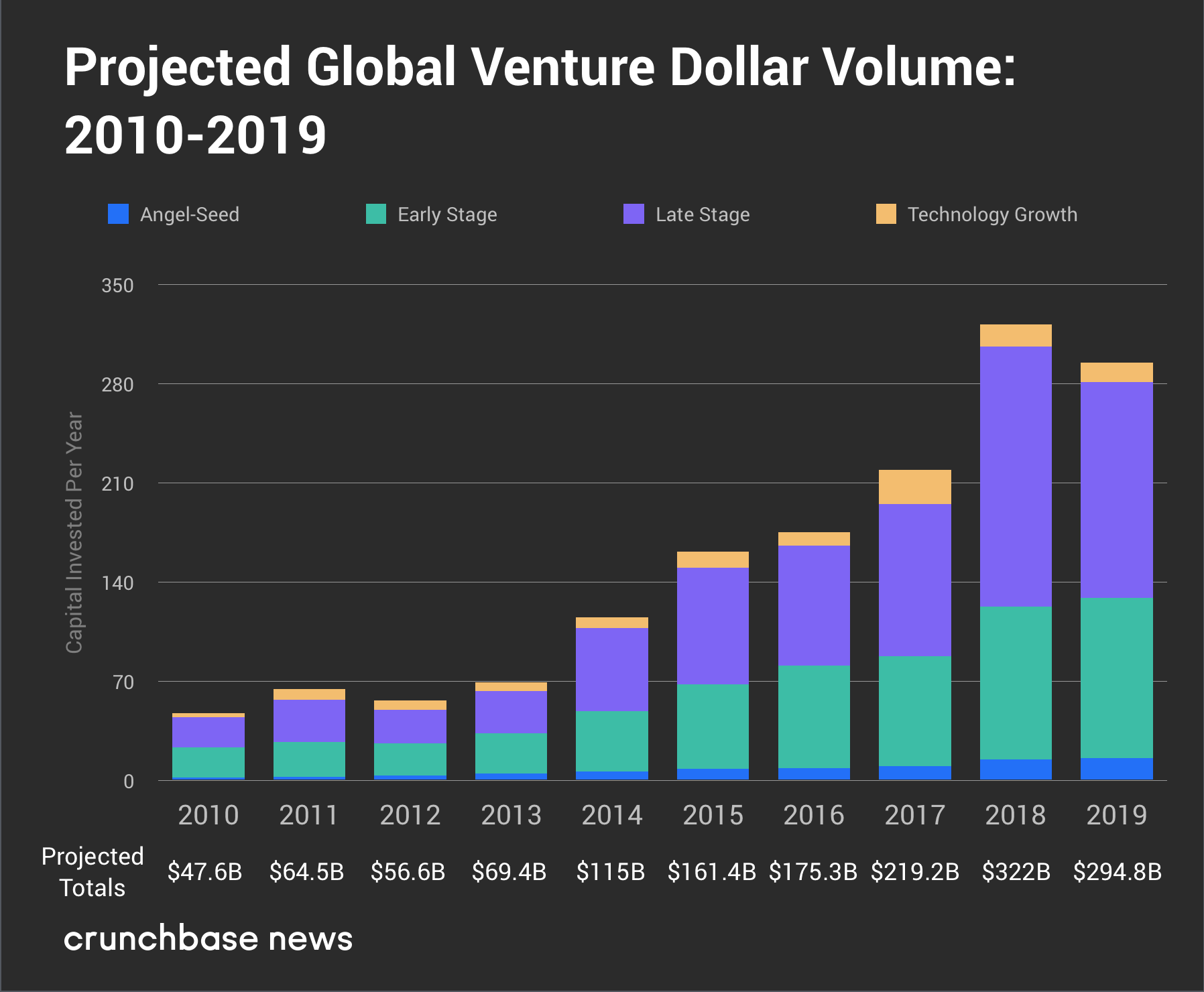

Venture capital is the fastest-growing segment of the private market. Global venture dollar volume has increased at a compound annual growth rate of 23% since 2010. This means the market grew approximately 6.5x between 2010 and 2020 - almost three times as fast as the rest of the P.E. market. Source

It is not just assets under management that have grown in VC. According to data from Cambridge Associates, indexed US Venture Capital has outperformed every other US index for the last 20 years. Source

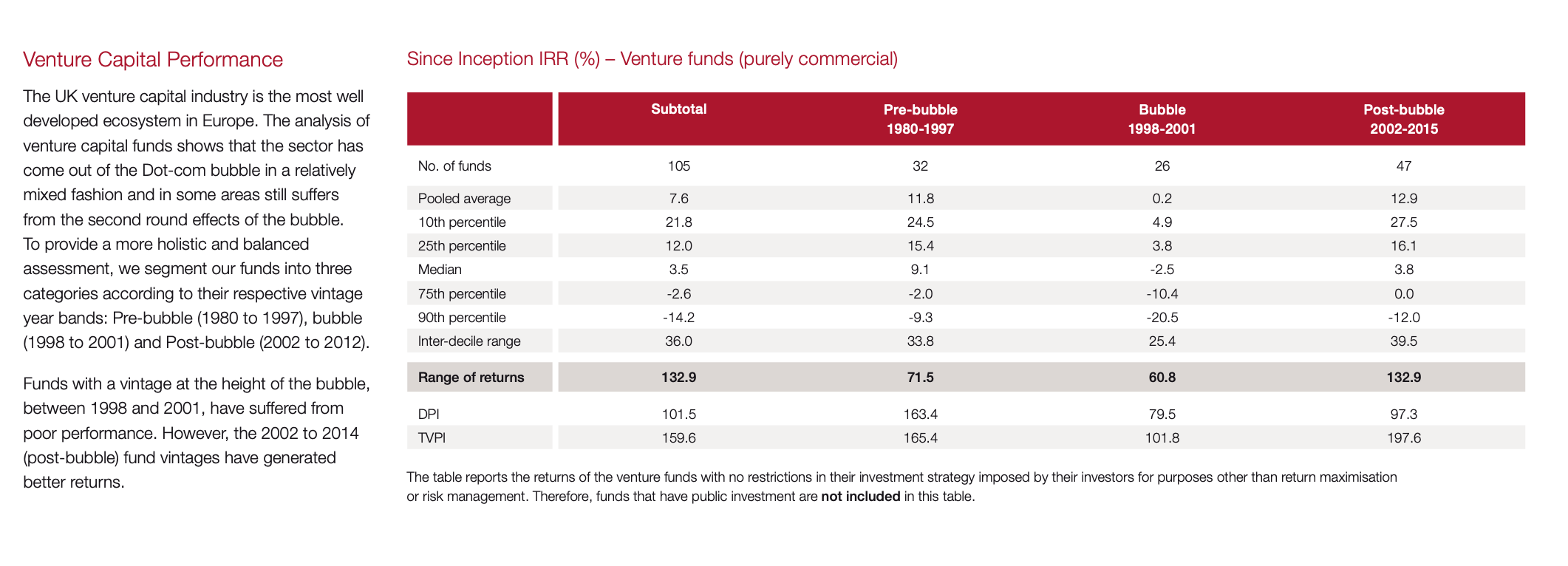

Whilst concentrated in Silicon Valley, this phenomenon is not unique to the USA, nor to China. In the United Kingdom, for example, according to BVCA data, both venture capital and private equity (buyout) significantly and consistently outperform the local public market indices in the mean. Source

Indexed UK Venture Capital has outperformed every other UK index except buyout PE for the last 15 years. Source

So why can't I invest in a VC or PE fund (or a bucket of such funds) like I can invest in an ETF or an index fund?

Good question. And actually, there are a range of ways a European retail investor can already invest directly in VC and PE funds today. Some of them are very interesting.

Invest in publicly listed funds like Draper Esprit and Augmentum.

Invest in an S/EIS fund or a VCT.

These are a tax-efficient investment vehicles that allow you to invest in a VC fund and claim up to 30% to 50% of your investment back in tax relief from the UK government (if you're a UK taxpayer).

You effectively leverage your investment for free, with no downside risk. HMRC pays for 30% to 50%, and you keep all the returns. You end up improving the return profile of your portfolio by somewhere in the order of 1.4x - 2x (You actually also reduce your downside on failed companies through loss relief, so the net multiple is probably a bit higher).

In addition, you pay zero capital gains tax on any profits...nice.

You could have invested in Passion Capital's latest fund via Seedrs, if you had your ear to the ground. No S/EIS.

AngelList Venture lets you invest in rolling funds, if you can navigate the signup process and you’re wealthy enough.

Moonfare and similar new products like Fundwiser are beginning to offer the ability for sophisticated investors to invest in baskets of alternative assets. No S/EIS, but this looks very promising.

In the coming years things will continue to improve, probably dramatically.

I believe this will be a net positive for humanity. More money in private markets hopefully means more primary capital invested in innovation, and more economic productivity as a result.

But it's going to take a little while. And there are going to be challenges along the way.

It also doesn’t necessarily mean better financial outcomes for retail investors.

You see, things are not as simple as they seem...

Risk and illiquidity

The outperformance of the private equity market comes with increased risk and less liquidity:

Startups and SME's are very fragile. A lot of them fail.

So even a fund manager with great track record can mess things up, leaving you out of pocket. Moreover, some of the data on returns that I've outlined so far is actually questionable because the returns are on paper - i.e. not realised. You can't sell the shares in these companies unless you have a buyer - and those buyers aren't always easy to find (as we'll discuss in point 2). This means your actual returns may look very different to your current paper returns.You can't cash out. You're locked in until the portfolio companies exit. Whilst Carta are making a go of it in the USA and both Funderbeam and Seedrs have tried things at small scale in Europe, there is no well-functioning secondary market (stock exchange) for startups. This means selling shares is tricky, unless you / your fund manager can find a buyer. This is a problem for many smaller investors. If you are putting money into stocks and shares with a plan to pull it out in 5 years and make a purchase, venture capital is not the place to invest it.

Power Laws and Access

In venture, as many of you know only too well, the returns are extremely unevenly distributed.

Thanks to the the VC Power Law the top funds (eg. the likes of Accel, Index, Balderton, Seedcamp and Localglobe in the UK) are doing much better than average. Top decile UK funds have delivered 27.5% since 2002, and the top quartile have delivered 16.1%. Conversely, the median fund is not worth investing in at all (second quartile only does about 4% IRR!).

The broader Private Equity market does not show the same sharp discrepancy between the median funds and the top funds, but there is still a significant difference in performance.

Essentially, this means that if you can't access top quartile VC funds, there's no point investing.

This creates a very tricky problem, since the best VC’s don’t need your money.

You see, investing in VC funds, like direct investment in startups, has a strong adverse selection tendency.

Just like the most desirable startups or the hippest nightclubs, the most desirable VCs have people fighting for access.

There is little apparent incentive for these top funds to disrupt the market and open things up to the little guy.

Maybe some will believe it is the right thing to do. It is also possible that a bucket of small ticket LP's managed by a third party would be less demanding. And winds of change are afoot in the UK (I've heard rumours aplenty) - but desire is only the first step.

I should add that, whilst I don't have any data to support it, I strongly suspect that the poorer performing funds are also sitting on more unrealised (paper) returns - since nobody wants to buy shares in their poorly performing startups. So their actual IRR may end up being even worse relative to the top performers than the BVCA data indicates.

Cost & Complexity

This is a tricky one.

Some costs are fixed and don't vary much depending on the amount of money being invested: eg. processing the investor's paperwork, administering the investments, managing distributions when an investment position is liquidated, etc.

That money is just as valuable to a smaller investor as a larger sum is to a larger investor. So they require just as much handholding and support, and they're just as upset if things go wrong (perhaps more so if they don't clearly understand the risks).

Private markets investing is less standardised and therefore more complicated than public markets, so a high demand from customers for information is common.

These things make handling small investments unattractive and unprofitable. This means more fees or more outsourcing, which eats into your returns.

Technology is beginning to emerge that solves some of these problems, but it will take time.

Regulation

The other problem in both the UK and Europe is regulation.

Patrick Newton from Form Ventures wrote a great thread on this recently.

Due to some FCA regulation I'm not going to dig into here, it's actually pretty hard for non high net-worth individuals to invest in a VC or PE fund.

There are workarounds for this issue (eg. the nominee structure in the UK, which is how S/EIS funds work). But they are just that - workarounds.

Technically, investors in EIS funds still need to self-certify as "sophisticated" (meaning they earn over £100k per annum or have net assets excluding property and pension of at least £250,000). And in practice, most of these funds don't accept investments below £25,000 anyway.

This puts such investments out of reach for all but the very wealthiest in our society.

This is in spite of the fact that the FCA is, apparently, perfectly happy for them to go and YOLO £3,000 on a crowdfunding platform, or head to the bookies and spaff it on Balko Des Flos to win the Grand National at 100-1.

Madness.

Market Froth

Essentially, right now, money printer go brrrr, investor go spend.

The current low interest rate environment, combined with QE and tales of fame and fortune from Silicon Valley, is probably pushing a lot more capital into the venture market than belongs there, or will likely remain there in future.

This is pretty obvious when you look for the signs. We are definitely witnessing hysterical behaviour amongst VC's and irrational expectations among founders at the moment.

Gil Dibner broke this down recently:

This is likely to end badly for a lot of people, and the top-performing funds will probably pull further away from the flailing pack.

Companies seeking to open the private markets to retail need a strategy that is likely to survive once the froth subsides. It must rely on aligned long-term incentives (carried interest) rather than short term ones (deal fees).

Ironically, the same could be said for a lot of VC’s, who are getting a lot richer from management fees than they are from exits.

So what's next?

In spite of the challenges, I still take the position that we should improve access to the private markets for everyone, and that, done right, allowing more small-ticket investors to participate is a good and necessary thing.

The wealth divide gets wider by the day, and we need radical, practical solutions to this problem from all areas of financial services.

In my next piece of writing, I'll cover part two of our investment thesis (a follow up to Pre-seed is coming). This will provide more detail on how we are planning to execute at Odin.

It is still early days for us, and we are testing things at small scale to start with. Please bear with us, we're working hard to build something you can all be a part of!

I will also take some time to write about other startups who are working to make investing in PE and VC more efficient, digital and accessible, picking up from some of the great work being done by Michael Sidgmore and others on this subject already.

I believe that the companies currently seeking to mainstream alternative investment may be some of the most important in history.

I'm excited to have you along for the journey.

P.R.