Unreasonable Breakthroughs

Noubar Afeyan has devoted his career to proving innovation can be systematic, and the volume of successful exits from Flagship Pioneering appears to prove his point.

“Over 25 years, I’ve learned that you can’t predict the future. You can only decide what kind of future you want to live in and do your best to build it.”

Noubar Afeyan, Co-founder of Moderna and CEO of Flagship Pioneering

The world first encountered Moderna in 2020, when the inconspicuous Massachusetts biotech announced that it was developing a vaccine to combat the pandemic.

That vaccine, mRNA-1273, would be administered hundreds of millions of times across more than seventy countries. It introduced an entirely new class of medicine, where a synthetic strand of genetic code tells the body to manufacture a protein that the immune system can then learn to recognise.

As with most overnight success stories, the technology had been in development for more than a decade before it was launched onto the world stage.

“There was no ‘aha’ moment when the mRNA breakthrough happened. The Moderna platform was built on a constellation of technologies, methods, and know-how that evolved over time.”

What Evolution Can Teach Us About Innovation, by Noubar Afeyan and Gary P. Pisano

Moderna was founded in 2010 and went public in December 2018, one year before SARS-CoV-2 emerged. Their initial public offering raised approximately $604 million, the largest biotech IPO in history at the time.

The size of the offering was extraordinary given how little the company had to show for it commercially. There was no approved product, no late-stage clinical results and no obvious near-term revenue. The company was built on the promise of the mRNA platform. The central idea, that messenger RNA could be used safely and reliably, was viewed with skepticism by much of the pharma community.

So, Moderna had remained a “non-consensus” investment for most of its life, even as a listed company. The company’s existence can largely be credited to the investor and entrepreneur who decided that the question of mRNA was important enough to deserve a real answer. That investor was Noubar Afeyan, the co-founder and chairman of Moderna and the CEO of Flagship Pioneering.

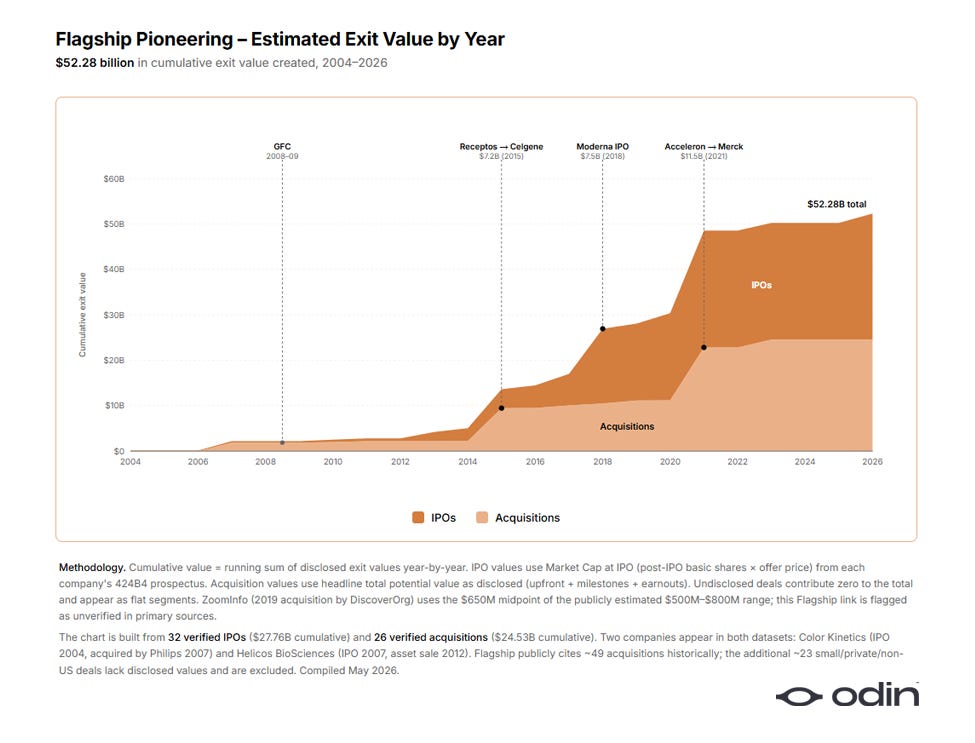

Flagship Pioneering has now originated or fostered more than 120 ventures with an aggregate market value approaching $100 billion, with about $52 billion in aggregate exit value. Moderna is the most famous, but is just one output of a process that Afeyan has demonstrated is scalable and repeatable.

Indeed, Afeyan’s view is that Moderna was not the typically idiosyncratic success story of a “venture bet”, but the predictable result of a process that he had designed to build test and develop ideas that were overlooked for being too risky or unreasonable.

“We have to be willing to embrace unreasonable propositions and unreasonable people in order to make extraordinary findings. Because the notion that utterly reasonable people doing utterly reasonable things will produce massive breakthroughs, it doesn’t compute to me.”

A Stranger in a New Land

Noubar Afeyan was born to an Armenian family in Beirut in 1962. In 1975, as the Lebanese Civil War erupted, his family fled to Canada, which gave them citizenship and a chance to begin again. He grew up in Montreal, studied at McGill University, and then arrived at MIT to work on biochemical engineering, becoming part of one of the very first PhD cohorts to be educated at the hybrid frontier of engineering and biology.

In 1987, at the age of 24, he started a company. This was an unusual move in itself, since venture funding at that time tended to flow to executives from Merck or IBM rather than to fresh PhDs without a network in the tech industry. He had no obvious right to be doing what he was doing, which he would later recognise as a strength.

“I had no connections. I was an immigrant. I came originally from Lebanon, escaped the war, went to Canada, kind of grew up in a foreign place. So I had zero expectations. Zero entitlement. I was not even American, I was Canadian.”

Noubar Afeyan, in conversation with Karim Lakhani of Harvard Business School

PerSeptive Biosystems, the company he founded, made instruments for the protein side of the emerging life sciences industry. Over ten years, five as a public company, it grew to roughly 880 employees (more than 200 of them with advanced degrees) and became the largest player in its category. In 1997, PerSeptive merged with Perkin Elmer in a stock swap valued at $360 million. Afeyan, by then in his mid-thirties, spent his last working years at Perkin Elmer’s successor, Applera, where he helped initiate Celera Genomics, the company that raced the public consortium to sequence the human genome.

While running PerSeptive, he had also been co-founding other companies on the side, partly because he kept noticing that good ideas were not finding their way into the world. The conventional view was that entrepreneurship involved a founder dedicating themselves to solving just one problem, but he didn’t see why that had to be the case.

Rejecting the Lottery

By the late 1990s, Afeyan’s experience with founding multiple companies had him pondering a Drucker-esque question that would shape the rest of his career.

“Why isn’t entrepreneurship a profession? And if it was going to be a profession, how could it be a profession?”

What bothered him was the valorisation of chaos, the heroic creation myths, and the prizes and competitions that created a lottery-like mindset about startup success. Founders were expected to live or die on a single giant outcome while investors sensibly diversified their exposure across many.

In 1999, he co-founded a firm with Ed Kania, a seasoned venture capitalist from Morgan Holland Ventures. Initially they called it NewcoGen, for “new company generation.” Two years later, after a number of people warned him it sounded like a disease, it was renamed to Flagship.

The premise was to manufacture companies, rather than to invest in them. In its earliest years the firm blended traditional venture investing with company creation, generating a series of exits that built serious credibility. Adnexus Therapeutics sold to Bristol-Myers Squibb, Accuri Cytometers sold to Becton Dickinson, Morphotek sold to Eisai, and Hypnion sold to Eli Lilly. There were also public listings such as AVEO Pharmaceuticals, Agios Pharmaceuticals and BG Medicine, and Color Kinetics.

The exits generated by the firm to date have comfortably funded the experiment that mattered most to Afeyan, which was to see whether the act of company creation could become a discipline.

“I realised that becoming a co-founder is an interesting concept relative to a solo founder and that you could do more than one thing in parallel. That led to the founding of Flagship.”

Venture Hypotheses

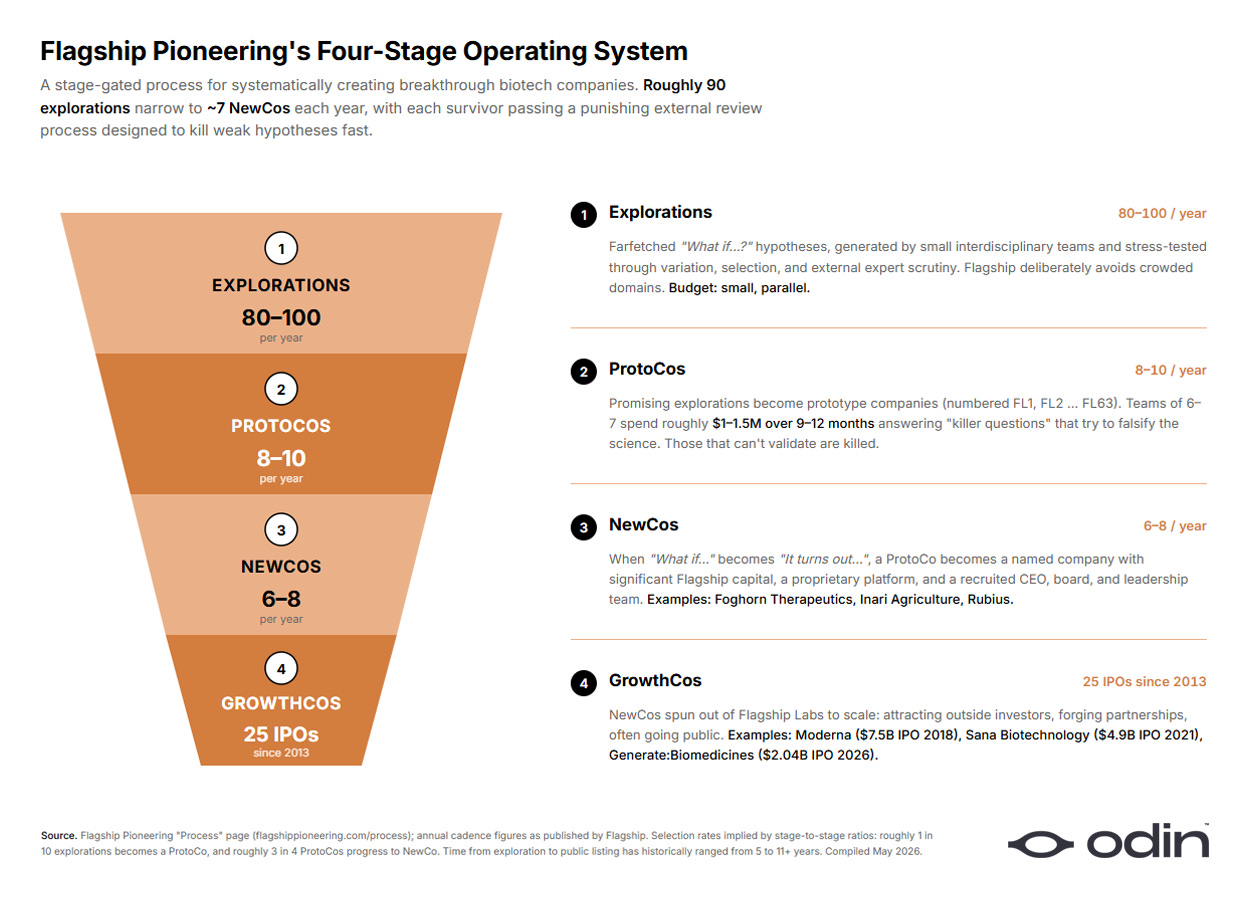

Flagship’s operating system has four stages, as it takes ideas through to full commercialisation.

In the exploration phase, small interdisciplinary teams of scientists generate “venture hypotheses,” speculative conjectures about what might be possible. Crucially, the firm runs many of these in parallel, on the order of fifty to a hundred a year, and explicitly avoids domains that are already crowded with other companies.

“We’re trying not to operate in a way that’s grounded in the present. We’re trying to say, ‘Okay, what could exist?’ And then we work backward.”

Those early hypotheses are then exposed to a punishing external review process. Flagship presents them to working scientists, large pharmaceutical companies, academic experts and informed amateurs, knowing that most will react with scepticism. Indeed, the “organised scepticism” of science is being deliberately weaponised to surface flaws and force the idea to evolve.

The hypotheses that come through that process without being killed by a fatal objection advance to the prototyping phase, which Flagship calls a ProtoCo.

“In that phase, it’s the founding team who worked on the exploration, plus maybe three or four people that have expertise in a particular scientific area. This team of maybe six or seven will engage in answering literally killer questions. We want to falsify our hypotheses experimentally.”

The prototyping budget, in line with the firm’s broader philosophy, is intentionally modest, typically $1 million to $1.5 million over nine to twelve months, designed to maximise what Afeyan calls the “learn-to-burn ratio.”

Of the hundred or so explorations begun each year, only ten or fifteen become ProtoCos, and roughly six to eight of those become NewCos, the dedicated companies that Flagship founds, funds and grows. The rest are killed. The discipline of killing weak ideas quickly is what makes it safe to test all kinds of outlandish-seeming hypotheses to begin with.

"Reasonableness in my view is the gravitational force that keeps innovation from happening. Because people enforce reasonableness in the scientific world on what you are allowed to say."

Noubar Afeyan, in conversation with Karim Lakhani of Harvard Business School

Indeed, the reason the system can pursue unreasonable ideas, Afeyan argues, is the scale at which they operate. With fifty or a hundred parallel explorations, abandoning one is not a tragedy. Within a single company, killing the idea often might mean losing the company.

Paranoid Optimism

The ingredient that holds this system together is what Afeyan calls “paranoid optimism”. This matches his description in a recent Boston Magazine profile, titled, “Moderna Cofounder Noubar Afeyan Is Afraid of Everything, And That’s His Genius.”

“I can see the scary part of just about everything, because we have to imagine it to try and go after it.”

He describes the mindset as similar to learning to switch between the gas pedal and the brake pedal. A completely optimistic founder makes reckless commitments, while the totally paranoid founder never makes it to launch. Toggling between the two modes of belief and doubt is what keeps the firm honest about what could fail, and ambitious about what might work.

“If you’re a paranoid optimist, by that I mean you’re not so optimistic that you actually get reckless, but you’re not so paranoid that you get depressed. And this constantly questioning whether it really will work, or how big it will be, or whether you should be doing something else, that doubt, doubtful optimism which is really a tortured state to be in, is perfect for evolution.”

Noubar Afeyan, in conversation with Karim Lakhani of Harvard Business School

Afeyan has come to see this mindset as something absorbed from his Armenian background. Armenian history contains a pattern of toggling between survival and thriving, of populations that have endured by simultaneously preparing for the worst and refusing to be defined by it. Lebanon, he notes, has its own version of stubborn optimism, which has sometimes carried the country through crises and sometimes prevented its people from confronting the harder truths.

It also helps to explain something more subtle about how Flagship operates internally. Afeyan describes his most distinctive working habit as a deliberate willingness to be wrong out loud.

“I think that if you’re doing something that’s never been done before, you have to be very humble to recognise that you don’t know what the right thing to do is, but also nobody else does. And in that milieu, you need to create a culture where people are willing to say things that may be wrong so that others can say other things. And over time, whatever is right can emerge.”

Embodied Platforms

As you might have gathered, Flagship is not a venture capital firm in the conventional sense, as it does not primarily fund other people’s companies. Neither is it really a research institute, since it commercialises everything it produces.

It is closest, perhaps, to an industrial company whose products are other companies.

“Flagship is itself an experiment in a new breed of company that conceives and creates and launches and develops companies. So a company that develops companies is not a traditional way one fathoms what a company does. Our products are effectively platforms that are embodied within companies.”

Flagship reorganises the usual venture capital structure so that the people doing the science are protected as well as the people with the capital, increasing their tolerance for risk and the ambition of the challenges they tackle. Within Flagship’s VentureLabs, any team working on a platform hypothesis that fails will just move on to the next, recognising failure as a valid outcome. Disproving a hypothesis is as important as proving one if your goal is process-led experimentation.

This enables something else that the usual venture model has trouble with, which is patience. Because Flagship is a principal investor in its own creations rather than a fund manager working to a defined liquidity window, it can afford to spend a decade developing a platform like Moderna without forcing the issue. Some ventures have taken nine, ten, eleven years from exploration to clinical traction. Others, such as Generate:Biomedicines, have gone faster but only because the underlying tools, in this case modern AI, suddenly caught up with the ambition.

Developing Polyintelligence

Generate:Biomedicines is the company that best illustrates where Afeyan thinks the model is heading. It emerged around six or seven years ago from a Flagship exploration that asked whether it was possible to computationally design proteins of arbitrary function. The conventional wisdom, even within the AI community, was that this required exhaustive knowledge of folding structures and underlying physics. The Flagship team believed that the necessary information was implicit in the DNA sequence itself, since nature managed without ever knowing what a protein was.

“DNA has no idea what a protein is. There’s no idea what folding is, and yet, boom, the function follows. So we said there must be an encoding of that knowledge in the DNA. There’s enough data in there somewhere. There’s patterns that are basically encoded which we don’t understand.”

Generate:Biomedicines now has more than fifteen computationally designed antibody programmes, several in or advancing to the clinic. It is also the first major biology partnership Nvidia made. Other Flagship ventures have applied similar techniques to cell biology, DNA and RNA molecules, lipid nanoparticle design and what Afeyan calls “autonomous scientific discovery,” in which AI agents generate hypotheses, specify experiments, run them and iterate without continuous human intervention.

Afeyan uses the term “polyintelligence” to describe this interaction of human intelligence, machine intelligence and what he refers to as nature’s intelligence, the logic implicit in biological systems themselves. The argument is that biology is itself a form of computation, and that AI is now sophisticated enough to read patterns inside it that humans never could.

The Hit Factory

Of course, not every Flagship company has succeeded. Biotech is a brutal business and a meaningful share of even well-funded platforms reach the clinic and stall, or never reach the clinic at all. Some of the firm’s more recent listings have suffered in the post-2021 biotech downturn.

However, Flagship’s aggregate record is hard to argue with. The firm has originated more than 120 companies, supported dozens of public listings, and is one of the few venture vehicles in history that can credibly claim to have generated a public-health outcome at the scale of a global pandemic response. In the process, Flagship has scaled its capital base into the multi-billion-dollar range.

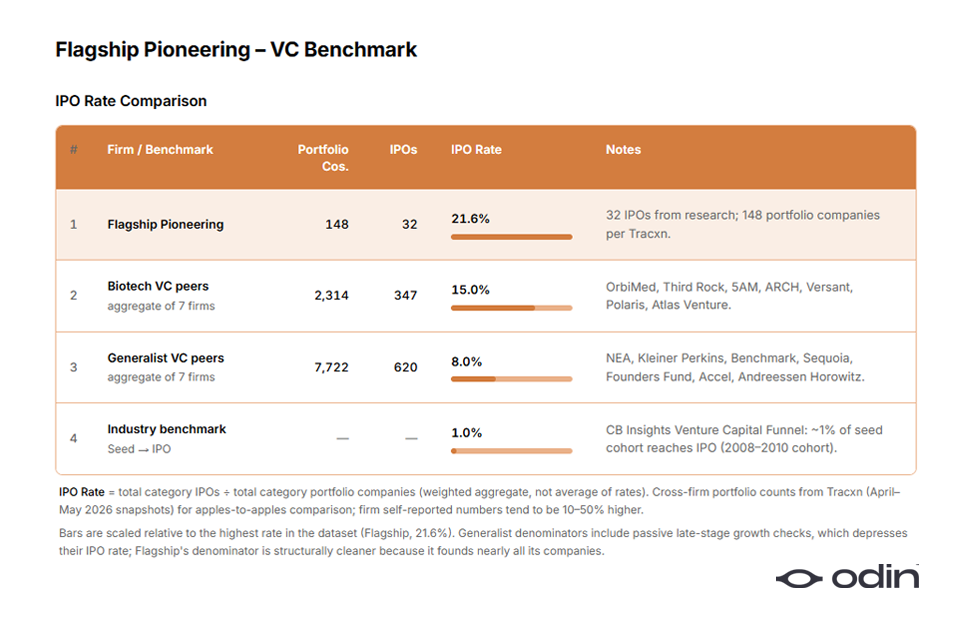

The rate of exits from Flagship’s portfolio (around 40% if you exclude acquisitions without disclosed terms) is remarkable by venture industry standards. With 21.6% of their portfolio companies achieving an IPO, the firm has double the estimated rate from a pool of “blue chip” venture firms.

There is some survivorship bias at work here, as biotech companies go through a more strenuous process prior to incorporation, though we can also see that Flagship has significantly outperformed an average of their biotech peer group.

Flagship’s success contradicts several pieces of common wisdom in venture capital.

Most venture firms pride themselves on finding the best companies; Flagship has shown that some of the most valuable companies are the ones you build yourself.

Most innovation strategies favour focused execution on a single asset; Flagship has shown that there can also be strength in optionality.

Most cultures of innovation treat the founder as protagonist; Flagship treats the process as the protagonist and the founders as a supporting cast.

However, Afeyan has cautioned against interpreting this as a recipe for success. The system, as it has been designed, depends as much on its mindset as on its methodology. A mindset has been formed by decades of learning to toggle between fear and possibility. It is also a system that suits a particular kind of work. Companies in market-led, execution-driven industries, where the customer need is obvious and the technology is established, may find emergent discovery to be overkill. Where it makes sense are the domains that the venture industry has decided are too speculative, too long-term, or too unreasonable to invest in.

“The reason we use the word ‘pioneering’ is that there’s a first-in-kind character to what we do. There are always new things to explore and new places to go. Opportunities will constantly be created for what can come next.”

Effectively, Afeyan has turned the perspective of the outsider into a methodology and applied it at scale with the development of Flagship. His willingness to pose questions that credentialed insiders wouldn’t dare to ask has been a critical asset.

His contribution to the history of innovation may end up being less about any single drug or company than about that broader proposition, which is that the patiently paranoid and optimistic pursuit of unreasonable ideas can be organised, scaled and repeated.

“We take hard earned money, we deploy it to do things that are damn near impossible once in a while. We reduce them to practice so they become not only possible but valuable. And yet people treat it like, ‘Oh well, you know, it didn’t work. There’s twenty different things we tried. One of them worked.’”

Launch and run your VC firm from your phone, with Odin

Watch our latest episode of Going Solo, with Arian Ghashghai of Earthling VC