30,000 Feet Above the Venture Market

Are small and emerging managers paying the price for a downturn they didn’t cause?

Good morning! Before we jump into today’s piece, an event invitation:

When: Friday March 27th

Where: London (Covent Garden)

What: a screening of ‘The AI Doc’

The AI Doc: Or How I Became an Apocaloptimist purports to be the most important documentary of the year. It features Sam Altman, Dario Amodei, Demis Hassabis, Eliezer Yudkowsky, Tristan Harris, and 40 or so others wrestling with what AI means for the future of humanity.

We thought it was worth watching with a room full of people who have something interesting to say about it. Far from ridiculing it, we intend to deal with it seriously.

Whether or not you share its conclusions, what happens when the most powerful technology ever built outpaces our ability to govern it is an interesting question.

Come watch (it’s free). Then let’s argue about it.

We’ve got 4 spots left.

Now, over to Mr Gray…

“Many of the largest companies in the U.S. by market capitalization, including Apple, Google, Microsoft, and Cisco, were backed by venture firms in their early days. In addition, more than 60% of the IPOs that have occurred since 1999 have been venture-backed. Given that venture firms provide capital to highly innovative companies with the potential to create large social surpluses, distortions in their capital allocation decisions could have important welfare implications.”

Propagation of Financial Shocks: The Case of Venture Capital, by Richard R. Townsend

Every year, Venture Capital Journal surveys the institutional investors who provide the financial backbone of the venture capital industry. These limited partners, the pension funds, endowments, foundations, and family offices that allocate capital to venture funds, collectively shape the direction of innovation finance through their commitments, or their reluctance to commit.

Of the LPs surveyed, 32% said they plan to invest more in venture capital this year, while 58% intend to invest the same amount. Only 10% plan to invest less, the lowest figure recorded in at least six years. On the question of new commitments, 14% said they would make significantly more and 43% said slightly more, both figures up from the prior two years. The headline numbers seem promising.

If you look a little closer, the survey hints at allocation decisions that risk compounding many of todays problems. LPs are retreating from the smallest, earliest, and newest funds at a pace that should concern anyone who cares about the long-term health of venture capital’s engine of innovation.

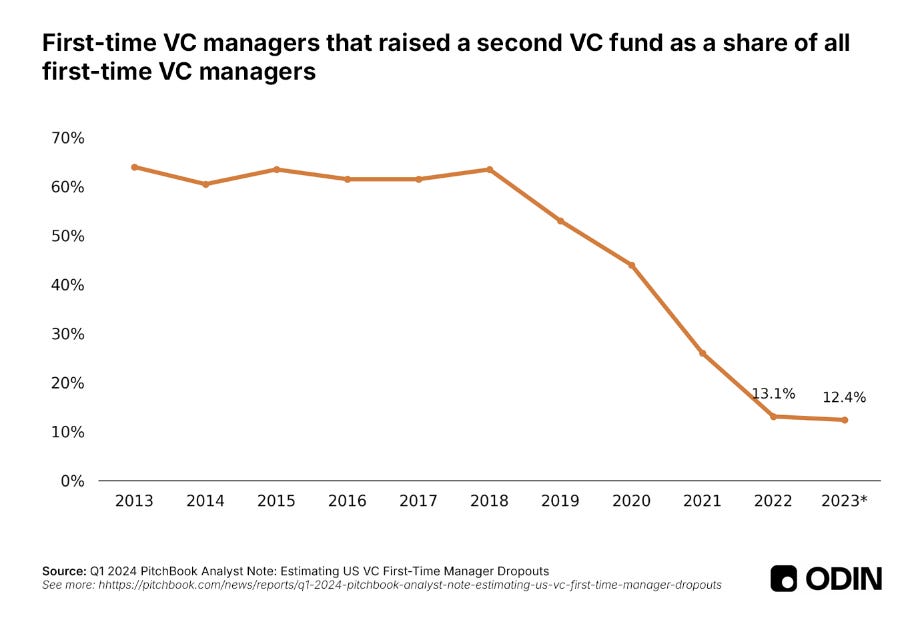

The Emerging Manager Exodus

The most striking finding in the 2026 survey is that 57% of LPs said they would not consider backing an emerging manager in the next twelve months. That figure was 33% just one year earlier. In a single year, the proportion of LPs unwilling to invest in new fund managers nearly doubled, despite consistent evidence of strong performance in that group.

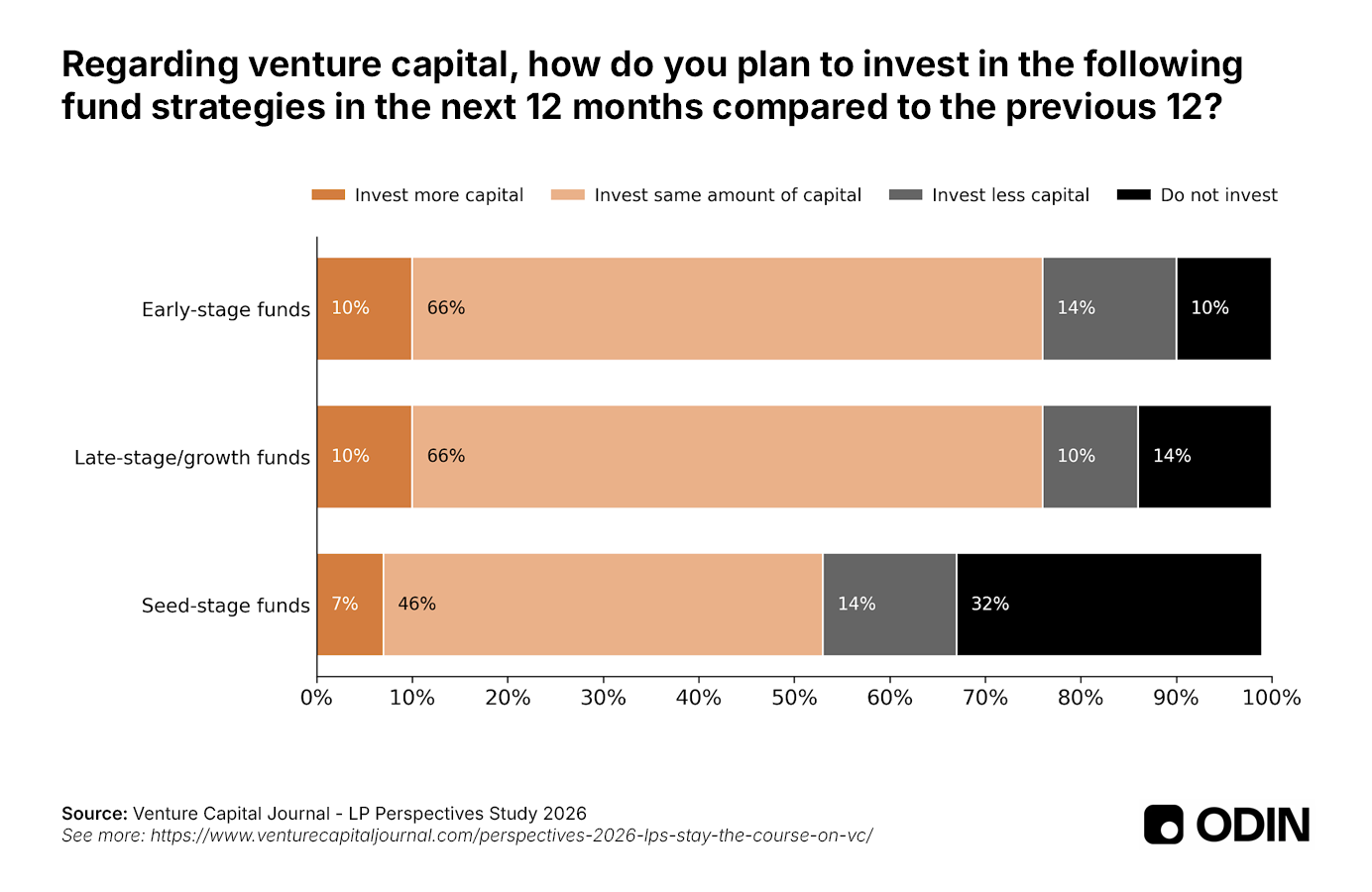

This was similarly reflected in stage preferences, where only 7% of LPs said they planned to invest more in seed-stage funds, 32% said they would not invest in seed at all, and 14% said they would invest less, leaving 46% investing about the same. Compare this with early-stage and growth funds, where 10% of LPs planned to invest more and 66% planned to hold steady. Capital is retreating to the “safety” of established names and later stages, away from the frontier.

Of course, this is something we have all sensed over the last couple of years, but it is fascinating to see the extent of the issue borne out in the data.

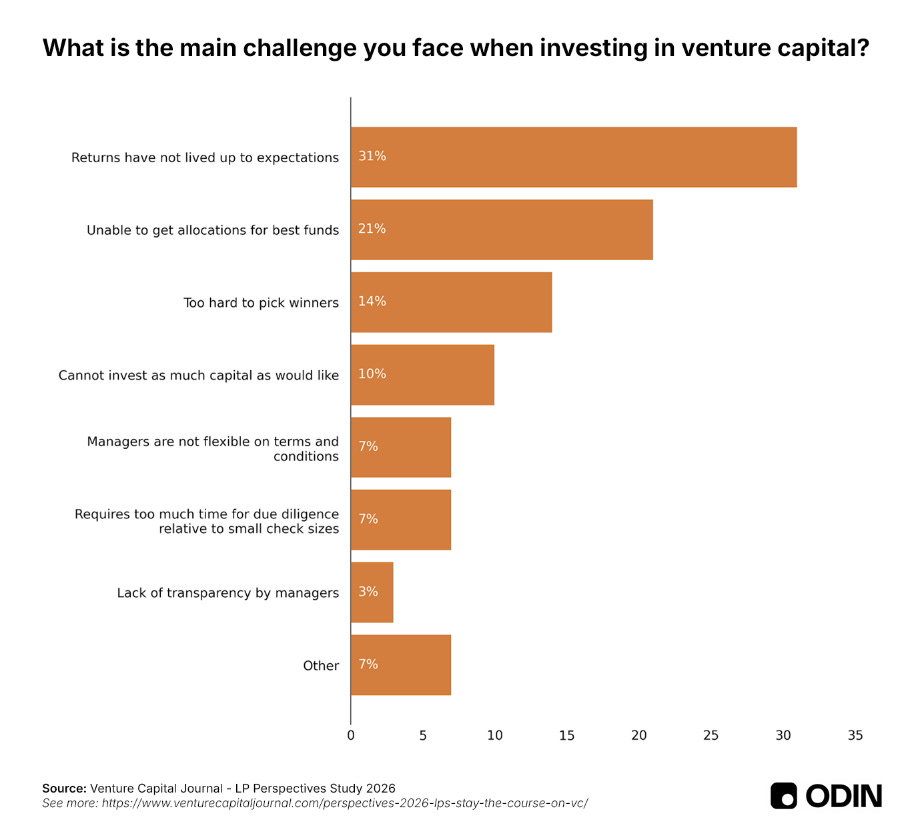

The top three reasons LPs give for their frustrations with venture capital provide some context:

31% said returns have not lived up to expectations

21% said they were unable to get allocation to the best funds

14% said it was too hard to pick winners

In reality, these are three different ways to say the same thing: performance has been disappointing due to an extended period of weak liquidity.

Others cited an inability to invest as much as they would like, inflexible terms, the burden of due diligence relative to small check sizes, and a lack of transparency by managers. These are real concerns, some of which reflect a need for greater professionalization and stronger standards in venture capital.

Problems of Venture Capital’s Own Making

“As a group becomes ten times larger, expenses increase much less than tenfold. As a result, management fees themselves become a profit center for the firm. These steady profits may create incentives of their own which may not be very appealing to investors. For instance, there will be an incentive to raise a larger fund at the expense of lower returns, which in turn may be tied to the greater concentration of capital held by a few investors; an incentive to put funds to work quickly and with a subpar amount of vetting so that a new fund can be raised sooner; and an incentive to focus on excessively safe investments that will not have as much upside but will pose less risk of a franchise-damaging visible failure.”

Venture Capital’s Role in Financing Innovation: What We Know and How Much We Still Need to Learn, by Josh Lerner and Ramana Nanda

The period from roughly 2016 to early 2022 was one of the most overheated in venture capital’s history. LPs flooded the market and the mega-funds emerged. Valuations climbed to levels disconnected from any reasonable expectation of near-term returns.

The consequences of that era are now well understood. Overcapitalization slowed exits by creating an overhang of overvalued private companies that couldn’t go public at prices their investors needed. The IPO market, which was already in decline before 2022, effectively shut for many venture-backed companies. The M&A landscape offered limited alternatives. Distributions to LPs dropped sharply. And in the most damaging cases, the loosening of governance standards enabled fraud and mismanagement at companies that had raised enormous sums with weak oversight.

Lerner and Nanda found that among publicly traded firms worldwide, seven of the top eight by market capitalization in 2020 had been backed by venture capital, and that VC-backed firms accounted for nearly 89% of recorded R&D expenditure among the cohort of post-1995 IPOs still public at the end of 2019. Venture capital, at its best, is an extraordinarily effective mechanism for financing innovation. Their concern was that structural changes in the industry were undermining that effectiveness. The concentration of capital in a small number of large funds, the narrowing of investment focus toward software and away from harder technologies, and the erosion of active governance were all trends they flagged as potentially detrimental to the broader innovation ecosystem.

Crucially, these problems are almost entirely correlated with the rise of mega-funds. The overcapitalization, the degraded governance, the herd behavior, the pursuit of capital velocity to justify ever-larger fund sizes, these are all features of the largest end of the market. The small and emerging fund managers that LPs are now abandoning were, for the most part, bystanders. Where these small firms did participate in the excesses of the boom, it was typically by chasing the same hot themes that mega-funds had already bid up, a reflection of LP demand signals.

Want to jump into the small fund gap? Do it with Odin, your full-stack partner for SPVs and fund administration

Collateral Damage

“Despite the fact that venture firms are structured to be more robust than most intermediaries, their portfolio companies can still face increased difficulty accessing capital when others that share the same investor suffer a negative shock. This can ultimately lead companies with high innovative potential to fail.”

Propagation of Financial Shocks: The Case of Venture Capital, by Richard R. Townsend

The pattern of innocent bystanders absorbing the damage of a correction they did not cause is not unique to the current cycle. There are clear examples from history, documented in a study by Richard Townsend of Dartmouth’s Tuck School of Business, examining how the collapse of the dotcom bubble in 2000 propagated through venture capital portfolios to companies with no connection to the internet sector.

Townsend’s research focused on non-information-technology companies, firms operating in sectors like biotechnology, medical devices, and energy, that happened to share venture investors with internet companies. When the bubble burst, these non-IT portfolio companies experienced a 26% larger decline in their probability of raising follow-on financing if their investors had high exposure to the internet sector, compared with similar companies whose investors did not. Indeed, after five years, the estimated probability of a company not having raised another round increased by over 8% for the affected group, a difference that, in the venture context, typically translates into company failure.

Critically, these companies were not worse investments. Townsend examined their patenting productivity, both the number of patents filed and the citations those patents received, and found no evidence that non-IT companies backed by internet-focused venture firms were of lower quality than their peers. They were just unfortunate collateral damage. Their investors’ portfolios had been contaminated by losses elsewhere, and the contamination spread to them through a mechanism that had nothing to do with the quality of their own technology or business prospects.

By exploiting the fact that many startups have multiple venture investors, Townsend was able to examine the same company across investors with varying levels of internet exposure. For the same portfolio company receiving capital from multiple venture firms, those investors with greater internet exposure were significantly more likely to drop out of follow-on rounds after the bubble collapsed. A one standard deviation increase in internet exposure was associated with a 38.5% increase in the probability of an investor dropping out, relative to an unconditional dropout rate of just 10.8% in the pre-bubble period. This within-company variation makes it far less likely that the results were driven by unobservable differences in company quality.

The Performance Paradox

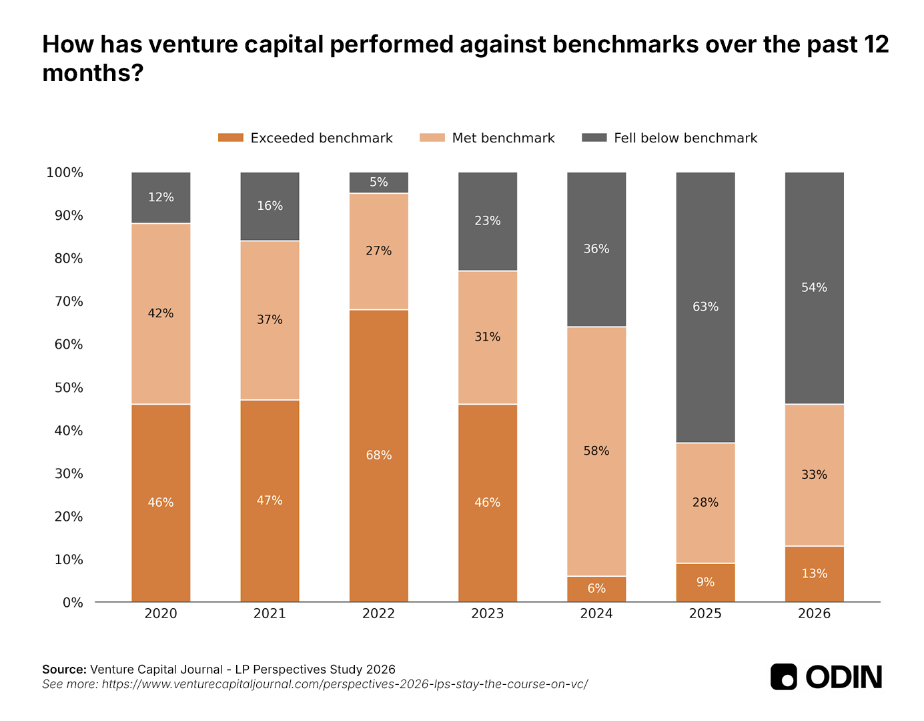

The survey data on performance perceptions highlights the extent of LP disappointment. Only 13% of respondents to the Venture Capital Journal survey said venture capital had exceeded their benchmarks for 2026, up slightly from what appears to have been a low of around 6% in 2024, but far below the roughly 46% that was typical in previous years. 53% said venture fell below benchmarks, an improvement from 63% in 2025 but still more than half of all respondents.

The anomalous year in the dataset is 2022, when 68% of LPs said venture had exceeded benchmarks over the last 12 months, the only year where the figure topped 50%. This was driven by the surge of distributions in 2021, the last gasp of the ZIRP liquidity cycle. What followed was a sharp and sustained deterioration in sentiment, with fewer than 10% of LPs satisfied with performance by 2024.

Curiously, in 2020, LP sentiment was also surprisingly low. Looking back on 2019 and facing the uncertainty of the pandemic, LPs could not see the wave of exits on the horizon. That pessimism came just before one of the best years for venture distributions in recent memory. Here, we can conclude that LP sentiment is a lagging indicator, not a predictive one. The survey measures how the market felt at the time, not how it is likely to perform in subsequent years.

If LPs are making allocation decisions based on recent disappointment, they are doing so at a moment when the drivers of that disappointment are already several years in the rearview mirror. The companies in current seed-stage portfolios were not part of the 2021 vintage frenzy, and have not yet had time to mature. Venture fund performance takes approximately eight years to become a meaningful reflection of a manager’s ability. Judging emerging managers by the returns of a period defined by mega-fund excesses is a major attribution error.

The No-Invest Equilibrium

“Like in a bank run, if current investors believe that future investors will withdraw financing from such a project, they should also withdraw their investment, even though all investors would be better off in the equilibrium in which everyone invests. This is not an irrational decision and furthermore, does not depend on information asymmetries. There are simply two equilibria – one in which everyone invests in a sector and one in which no one does.”

Financing Risk and Bubbles of Innovation, by Ramana Nanda and Matthew Rhodes-Kropf

A theoretical framework developed by Ramana Nanda and Matthew Rhodes-Kropf helps explain why the current LP retreat is so destructive. Their model of financing risk, published in a paper that has become influential in venture capital scholarship, shows that the availability of future funding is itself a determinant of present value. When investors believe that future investors will not fund a given sector or stage, they rationally withdraw, because the absence of expected future capital genuinely reduces the value of current investments.

The mechanism works through bargaining power. A startup whose investors cannot credibly signal future funding has a weaker negotiating position with potential acquirers. The acquirer faces a lower competitive threat from the startup, because the startup is less likely to survive and grow into a formidable competitor. This reduces the price the acquirer is willing to pay, which lowers the net present value of the investment, which makes the decision to withdraw capital rational.

The result is a self-fulfilling equilibrium, as the belief that funding will not be available becomes the reason that funding is not available.

Nanda and Rhodes-Kropf demonstrate that this dynamic hits innovative projects (where coordination costs are highest) the hardest. Investors can try to mitigate financing risk by committing more capital upfront, giving startups a larger cushion to survive a funding drought. But doing so destroys the real option value of staged investment, the ability to invest a little, learn, and decide whether to continue. This option value is most significant for the most uncertain, most innovative projects; precisely the kind that small seed-stage funds specialize in.

The paper is explicit that it is the most innovative sectors and firms that need the abundant funding equilibrium to invent and commercialize radically new technologies.

Townsend’s work on the dot-com collapse is a good illustration of this theory. His model shows that in principle, the direction of contagion within a venture portfolio is ambiguous. When some investments in a fund perform poorly, the remaining investments become relatively more attractive, since the venture firm has a fixed pool of capital to deploy. This reverse contagion effect, analogous to the bright side of internal capital markets, would predict that non-IT companies in internet-heavy portfolios should have benefited from the collapse, receiving more capital as their investors redirected resources away from failing internet bets.

The fact that Townsend’s evidence decisively rejected this prediction, showing that contagion was ordinary rather than reverse, tells us something important about the power of the fundraising channel. The theoretical possibility of capital reallocation within a portfolio was overwhelmed by the venture firm’s diminished capacity to raise new funds from limited partners.

Indeed, venture firms in the top quartile of internet exposure experienced a 47.5% larger decline in their fundraising capacity after the bubble burst compared with those in the bottom quartile; a fundraising shock that would cascade to their portfolio companies. The effect was strongest for young venture firms and for firms that had not raised a new fund recently, exactly the profile one would expect if the transmission channel was LP capital commitments. For companies backed by a venture firm that had just raised a fresh fund, investor internet exposure had no statistically significant effect on continuation financing.

Essentially, the damage was concentrated among companies whose investors were dependent on near-term fundraising, the firms most vulnerable to a shift in LP sentiment.

This parallel will be felt by emerging managers who raised Fund I in 2021 or 2022 are now attempting to raise successor funds in an environment where 57% of LPs have declared them off-limits. Townsend’s evidence shows that this kind of fundraising shock will propagate to portfolio companies, reducing their access to capital regardless of their underlying quality, and it does so most acutely for the youngest and most capital-constrained investors.

In summary, when 57% of LPs say they will not consider emerging managers, they are sending a signal that pushes that part of the market toward what Nanda and Rhodes-Kropf call the “No-Invest equilibrium”. Founders become less willing to take capital from emerging managers because they worry about follow-on risk, and co-investors grow cautious. The emerging managers’ portfolios lose value because the ecosystem around them is less optimistic. Returns decline, and LPs cite the declining returns as evidence that they were right to withdraw, completing the circular logic.

The Concentration Trap

“While venture funding is very efficacious in stimulating a certain kind of innovative business, the scope is increasingly limited. This concentration may be privately optimal from the perspective of the venture funds and those who provide them with capital. It is natural to worry, however, about the social implications of these shifts. For instance, promising startups developing renewable energy technologies and advanced materials, which might have broad societal benefits, may languish unfunded.”

Venture Capital’s Role in Financing Innovation: What We Know and How Much We Still Need to Learn, by Josh Lerner and Ramana Nanda

Lerner and Nanda’s research documents just how concentrated the venture capital industry has become. As of their 2020 analysis, the top 50 investors, representing roughly 5% of all venture firms, had raised half of all capital deployed between 2014 and 2018. The partners at these firms are overwhelmingly male graduates of a small number of elite universities, based in the San Francisco Bay Area. This concentration amongst investors also ends up limiting the diversity of ideas that get funded, via the well documented problems of homophily, herd behavior and heat seeking.

The authors note that while this concentration may be privately optimal for individual funds (expanding fee income, easier fundraising from LPs), it raises concerns about the cost to progress when categories of promising technology go unfunded. Additionally, such concentration dramatically raises the risk from a market correction, similar to the post-dotcom retreat documented by Townsend.

PitchBook data confirms this concentration problem has deepened in the years since. The belief that AI is the defining opportunity of this era, and that AI companies require enormous amounts of capital which small firms are ill-suited to provide, has pushed LPs further toward large funds.

There are two problems with this reasoning. The first is that the history of venture capital consistently shows that the hot theme of any given vintage is rarely where the largest outcomes emerge. Venture returns are driven by outliers, and outliers, by definition, are rarely in consensus categories. The second is that consistent allocation across stages and fund sizes is essential to a healthy venture ecosystem and good long-term performance.

“We find that consensus entrants are less viable, while non-consensus entrants are more likely to prosper. Non-consensus entrepreneurs who buck the trends are most likely to stay in the market, receive funding, and ultimately go public.”

The Non-consensus Entrepreneur: Organizational Responses to Vital Events, by Elizabeth G. Pontikes and William P. Barnett

Early-stage managers, including emerging managers who bring fresh perspectives and networks, are the entry point of the pipeline. Without adequate funding at the base, the later stages that LPs favor will eventually run short of high-quality companies to back.

LP’s Accountability for Allocation

Consider the eight categories of challenges that LPs cited in the survey. Returns not meeting expectations, inability to access the best funds, difficulty picking winners, constraints on capital deployment, inflexible terms, due diligence burdens, lack of transparency: many of these can be traced to structural features of the mega-fund era or to shortcomings in LP portfolio construction and monitoring.

If returns have disappointed, the relevant question is what funds those LPs selected and at what point in the cycle. If they were chasing oversubscribed brand-name funds during the 2020 to 2021 boom, paying for access to an overheated market, the underperformance is primarily a portfolio construction failure.

Not being able to access the “best” funds may relate to an inability to recognise promising managers early to secure allocation, or suffering from hindsight bias in relation to fund performance. Finding it too hard to pick winners may reflect a similar failure to develop the expertise required to evaluate firms and make objective judgments.

If terms are inflexible, it is worth noting that LPs have collectively failed to reform venture fund economics for decades, despite well-documented misalignments.

Indeed, Lerner and Nanda note that management fees, originally designed to cover costs for small funds, have become a significant profit center as funds have grown.

Additional research by Metrick and Yasuda shows that over $23 of every $100 invested ends up with the venture firm, the majority coming from fixed fees rather than performance-linked carry. Their study also questions the fundamental logic of larger venture capital funds.

“The VC skills that are critical in helping firms in their developmental infancy are not applicable to more mature firms that are ten times larger and already in possession of core management skills. So when successful VC firms increase the size of their fund, they cannot just scale up the size of each firm they invest in without dissipating their source of rent.”

The Economics of Private Equity Funds, by Andrew Metrick and Ayako Yasuda

In aggregate, many of the challenges expressed by LPs are what a less diplomatic observer might call a skill issue.

The problems LPs face are substantially of their own making, or of the making of the large-fund ecosystem they continue to favor. The small and emerging fund segment, which is bearing the brunt of the retrenchment, is the least connected to the dynamics that have driven the downturn.

Maintaining the Techno-Capital Interface

Nanda and Rhodes-Kropf include a finding that deserves particular attention from LPs looking to structure a venture capital portfolio. They suggest that the mix of investors should shift toward smaller participants during periods of low financing risk, because smaller and more frequent investments are well suited to periods when future capital is expected to be available. For example, a skew toward small funds in the 2014-2018 period would have produced a larger and more diverse set of opportunities to absorb capital at the peak in 2020-2022, reducing fragility and the extent of the correction which followed.

In contrast, the model predicts that smaller investors will virtually disappear from the market during downturns, as the coordination costs to continue funding non-consensus projects are simply too high. This is not a desirable outcome, just the unfortunate nature of how the market suppresses the most innovative projects during the periods when contrarian investment would be most valuable.

Indeed, Nanda and Rhodes-Kropf suggest that some genuinely valuable technologies may require robust financial markets to get through the initial period of development (i.e. Carlota Perez’ “Installation Periods”), because otherwise the financing risk is too extreme. If this is correct, then the withdrawal of LP capital from early-stage and emerging funds is a clear impediment to future innovation. The most radically new ideas, the ones most likely to produce the outsized returns that LPs claim to seek, may be unable to survive the current financing environment precisely because the investors who specialise in finding them have been cut off from capital.

A sensible LP should understand that you invest in small and emerging managers because you trust them to go out onto the frontier and find the next opportunity. You invest in mega-funds (or mid-sized firms who service the megafirm consensus) because you believe there’s a present opportunity that requires more capital. These are entirely different categories, with different risk profiles, and treating one as a substitute for the other reflects a fundamental misunderstanding of how venture returns are generated.

Importantly, any “present opportunity” was, at some point in the past, the “next opportunity”, and relied on frontier investors that provide the interface between capital and technology. If that interface is underallocated, technological progress will quickly stagnate as the stream of new opportunities dries up.

The Cost of Consolidation

The venture capital market went through a period of extreme overcapitalization driven by mega-fund competition and the entry of non-traditional investors. That period produced inflated valuations, weakened governance, and an exit overhang that continues to depress returns and distributions. LPs, surveying the damage, appear to be consolidating their commitments into the very segment of the market most responsible for these outcomes while withdrawing from the segment least connected to them.

The emerging managers who raised Fund I in 2021 or 2022, now struggling to raise a successor, are generally not victims of a meritocracy; their portfolios have not had time to produce meaningful performance data. They are victims of a market correction they did not cause, operating under a standard of judgment shaped by the excesses of a different part of the industry.

The performance of a general partner’s previous private investment funds can predict future fund performance to a degree, but that’s only with at least eight years of hindsight, according to PitchBook’s latest Allocator Solutions report. In reality, LPs typically make decisions about where to commit fresh capital about three and a half years, on average, after a fund’s predecessor has closed—making it too soon to know exactly how the GP’s latest investments will pay out to existing LPs.

Fund performance data unhelpful for LPs when it counts, by Emily Burleson

Nobody knows what the venture market will look like in five years. The LPs who were so pessimistic in 2020, convinced the market was broken, were about to get one of the best years for liquidity in a generation. The LPs who piled in during 2021, certain they understood the opportunity, funded many of the worst outcomes.

The lesson, repeated across every cycle, is that the most valuable thing an institutional investor can do in venture capital is maintain consistent allocation across stages and fund types, resist the temptation to time the market, and support the parts of the ecosystem that the consensus has abandoned. Right now, that means emerging managers and seed-stage funds.

Unfortunately, the survey suggests that most LPs are doing the opposite.

But therein lies an opportunity…

Get started with Odin, your full-stack, digital-first partner for SPVs and fund administration.