Hitting Escape Velocity

Venture capital's rocky relationship with public markets

“We find for the overall sample, that the mean company-level return from IPO exits is 209.5 percent and the median return is 108.8 percent. By comparison, the mean return for M&A exits is 99.5 percent and the median return is −32.1 percent. The substantially lower returns for M&A exits are consistent with the concerns expressed by industry observers and prior academic work which has viewed IPOs as the primary vehicle of VC wealth creation.”

The Decline in Venture-backed IPOs: Implications for Capital Recovery (2013), by Susan Chaplinsky and Swasti Gupta-Mukherjee

Historically, public markets have been the primary customer of venture capital, offering a well-capitalised destination for the most successful venture-backed companies.

Unfortunately, that relationship is breaking down.

Exits by IPO are near historical lows, and post-IPO performance for venture-backed exits is often dismal. Combined with the influx of new (and generally less finance-literate) managers over the same period, there’s a real risk the industry might forget that handing great companies off to public market investors (for a large profit) is really pinnacle of the strategy.

All great companies eventually go public.

So, does venture capital still produce great companies?

In this article, we’ll look at the fundamentals for venture-backed IPOs, and how that relationship might be mended, via four main questions:

Why do companies go public?

When do companies go public?

What stops companies going public?

Does size matter pre-IPO? i.e. is it better to stay private for longer?

Why Do Companies Go Public?

Cost of Capital

Investors often talk about the range of challenges faced by public companies: stock price volatility, short sellers, compliance and reporting requirements… None of it sounds particularly fun for a young company that enjoys the flexibility offered by private markets.

However, as companies mature, they inevitably run into a problem with the “cost of capital”. That is, the amount of dilution they must accept to raise money, or the terms associated with any debt. Private markets have the highest cost of capital, because of the risk inherent in their opacity. For larger companies with greater capital requirements, this quickly becomes problematic.

Public companies, on the other hand, have a low cost of capital. While the standards for a public company are relatively high, and the transparency can feel uncomfortable, it means investors and lenders can better understand company health which translates into more appropriate terms.

The tipping point, where going public begins to make sense, is when most of the risk (which private market investors like, but public markets do not) has been removed from a company. Usually this implies growth is decelerating while economics are improving, as the business becomes more stable. There’s a misconception that this makes public markets unsuitable for innovative companies, or that you must be (near) profitable to IPO. Neither is true.

“We find that less profitable companies with higher investment needs are more likely to IPO. After going public, these firms increase their investments in both tangible and intangible assets relative to comparable firms that remain private. Importantly, they finance this increased investment not just through equity but also by raising more debt capital and expanding the number of banks they borrow from, suggesting the IPO facilitates their overall ability to raise funds. Finally, we show that firms’ borrowing costs conditional on their risk drop after going public.”

Access to Capital and the IPO Decision: An Analysis of US Private Firms (2024), by Andres Almazan, Nathan Swem, Sheridan Titman and Gregory Weitzner

Importantly, the lower cost of capital and the “burdensome” reporting requirements are directly connected. You cannot have one without the other, and this is actually an ideal configuration. The opacity and illiquidity of private markets give companies room to experiment without being punished for short-term failure. The transparency, scale and liquidity of public markets, on the other hand, offer a more efficient and meritocratic environment for companies that are larger and more mature.

For example, SpaceX is in the process of gearing up for an imminent IPO. It’s able to do so because a sufficient amount of risk has been removed from the business, and it needs to do so because raising from private markets has become a constraint.

“There’s a lot more capital available in the public markets than private. It might be 100x, but it’s way more than 10x. [...] Speed is important. I just repeatedly tackle the limiting factor. Whatever the limiting factor is on speed I’m going to tackle that. If capital is the limiting factor then I’ll solve for capital. If it’s not, then I’ll solve for something else.”

Finally, this has obvious implications for those who frame giant private rounds as “effectively an IPO without going public”. This is clearly not the case, as even when they raise tens of billions, private companies do not undergo anything like the same level of scrutiny. Their incentives are quite different, as private markets continue to emphasise risk-taking behavior to drive growth, and thus the outcomes are different also.

“The very act of dumping hundreds of millions of dollars into an immature private company can also have perverse effects on a company’s operating discipline. The only way to use the proceeds of such a large round is to take on massive operating losses. Historically, as a company neared an IPO level of revenues (say $50-$100mm), investors would expect convergence toward profitability. As these late-stage private companies digest these large fund raises, they are pushing profitability further and further into the future, as well as the proof that their business model actually works.”

Investors Beware: Today’s $100M+ Late-stage Private Rounds Are Very Different from an IPO, by Bill Gurley

Acquisitions

Another reason to go public is the desire to consolidate a leading position in a particular category through strategic acquisitions. Indeed, a survey of CFOs at recently-public companies in the post-dotcom era found that access to capital to drive acquisitions was the largest driver of IPO activity, reflecting the heavily competitive environment at the time.

Going through an IPO enables accelerated acquisitions via two means: firstly, through the capital raised in the IPO itself. Secondly, by converting to liquid stock the acquiring company suddenly has a much more attractive “currency” for stock-based transactions. It’s relatively common for acquisitions to include stock (about 30% of cases), particularly in ‘acquihire’ instances where the acquiring company wants to motivate talent with a stake in the acquiring company.

“We analyze post-IPO acquisition activity of IPO firms and find that there is a high incidence of newly public companies participating in mergers and acquisitions. We document substantial acquisition activity for IPO firms starting as early as their first year after the IPO. Our most striking result is that over the first five years following the IPO, newly public firms spend more money on acquisitions of other companies or assets than they do on research and development or capital expenditures, or the two combined. This suggests that newly public firms grow more through M&A than through internal investment in R&D and CAPEX.”

Going Public to Acquire: The Acquisition Motive for IPOs (2006), by Ugur Celikyurt, Merih Sevilir and Anil Shivdasani

This seems likely to grow in importance, as public companies are more often acquiring startups for access to new technologies and knowledge-driven innovation, such as the recent spate of “reverse acqui-hires” in the LLMs category.

“Firms in highly technological industries, faced with pressure to innovate and looking to expand, are increasingly acquiring startups with little interest in other assets beyond their human capital resources.”

Startup Firm Acquisitions as a Human Resource Strategy for Innovation: The Acqhire Phenomenon (2013), by Jaclyn Selby and Kyle J Mayer

Liquidity

Last but not least, the inevitable need to provide liquidity for shareholders.

With acquisitions being the main alternative to going public, there are a number critical reasons why an IPO is usually the preferred path to liquidity.

Firstly, in an acquisition, it is implicit that the founder loses control of the company to the acquirer. If the company represents their life’s work, this will be unattractive relative to an IPO where they will retain control and can steward it through the next chapter in public markets.

Secondly, there is typically greater information asymmetry between a private company and public market investors than there will be between a private company and a strategic buyer. This means, from the limited perspective of share price, and assuming normal market conditions, a company should be able to get liquidity at a more attractive share price in public markets than through acquisition. Acquirers also tend to have more pricing power, as there will be a small pool of interested buyers, producing a less competitive process relative to the efficiency of public markets.

“In our analysis of IPOs, we have taken the stance that pre-IPO owners’ prime objective is to establish a liquid market for their shares, as a means of maximizing the market value of their wealth. The owners attempt to accomplish this objective by optimally manipulating critical variables including and especially share retention, underpricing, and a lockup restriction.”

Pursuing Value Through Liquidity: Share Retention, Lockup, and Underpricing in IPOs (2003), by Steven Xiaofan Zheng, Joseph P. Ogden and Frank C. Jen

In recent years the pressure to reach a liquid endgame has diminished slightly, as secondary transactions have become more common. In the first three quarters of 2025, the total secondaries volume hit $94.9B, compared to $104.7B from IPOs and $107.1B from acquisitions, according to data from Pitchbook.

However, questions remain:

How many of these transactions are at steep discounts to the last marked price of the companies or portfolios involved?

How much of the total value is concentrated in employee-secondaries for the most obvious companies, like Stripe, SpaceX, Anthropic, OpenAI etc?

How much of the demand is for companies with an imminent IPO, as is true for 8 out of the top 10 on Setter’s ranking of secondary market demand?

Generally, do current volumes persist in a recovered market where great companies may begin exiting sooner, and GPs have fewer bad assets to offload?

Indeed, the rise of secondaries (particularly PE activity) is often connected to troubled times in venture capital, with patterns repeating across historical cycles.

“Of course, economic turbulence is not positive and investments could suffer in this environment. However, the performance of PE during these past recessionary periods demonstrates the opportunity that fund managers have to capitalise on declining valuations and distressed opportunities that often emerge during downturns.”

The secret behind private equity’s strength during the dot-com crash and the great recession, by Blazej Kupec and Jason Feder

Want to back the next Mag-7 companies? Try Odin, your full-stack partner for SPVs and fund administration

When Do Companies Go Public?

In a basic sense, the timing of an IPO is typically the point on a spectrum at which the risk is no longer appropriately priced by private markets. Where the business is sufficiently and obviously strong enough that it would see a net benefit from the transparency imposed by public markets.

However, there are two other influences on when a company might decide to go public, one internal and one external.

Productivity Shocks

“In our model, two firms, with differing productivity levels, compete in an industry with a significant probability of a positive productivity shock. Going public, though costly, not only allows a firm to raise external capital cheaply, but also enables it to grab market share from its private competitors.”

IPO Waves, Product Market Competition, and the Going Public Decision: Theory and Evidence (2012), by Thomas J. Chemmanur and Jie He

A “productivity shock” can be considered as a major step-up in capability in a particular technology, unlocking real economic value. It significantly improves the offering of the company, with meaningful consequences for revenue and profitability, providing a springboard into public markets.

For example, OpenAI’s release of GPT-3.5 in 2022 was a major turning point for technology, but it did not constitute a productivity shock. At that point, LLM chatbots were a fun toy with obvious future potential but little immediate utility.

Since then, we’ve seen a number of AI-related productivity shocks.

Arguably, DeepSeek’s R1 model, released in January 2025, was the first hint at a productivity shock, by significantly driving down the cost of inference with fairly sophisticated models.

The next (minor) productivity shock was the release of “Nano Banana” by Google, in August 2025. For the first time, image models were accessible and accurate, creeping into the domain of professional photography (e.g. product photos, fashion catalogue images, headshots).

With coding agents it’s harder to pick a specific moment; the ability to write code with an LLM has been improving steadily since day one. Recent releases like Claude 4.6 Opus and GPT-5.3 Codex may be looked back on as the tipping point at which much artisanal programming (particularly for front-end) became obsolete.

Today, both Anthropic and OpenAI are both rapidly tapping new veins of potential productivity, with Excel agents, financial agents, legal agents, and more. As both companies reportedly aim to go public within the year, it’s clear they are both looking for (and likely on the verge of) some new productivity shock.

IPO Windows

You will often hear private market investors discuss the need for an “IPO window”, but it’s never entirely clear what that means.

Under the interpretation that an IPO window is a period during which public markets seem healthy, that describes most of the last three years, and yet IPO activity has been relatively subdued. A more honest interpretation is that an IPO window is simply a time in which there are many IPOs, which isn’t really helpful; a private market investor calling for more IPOs is like a baker calling for more bread.

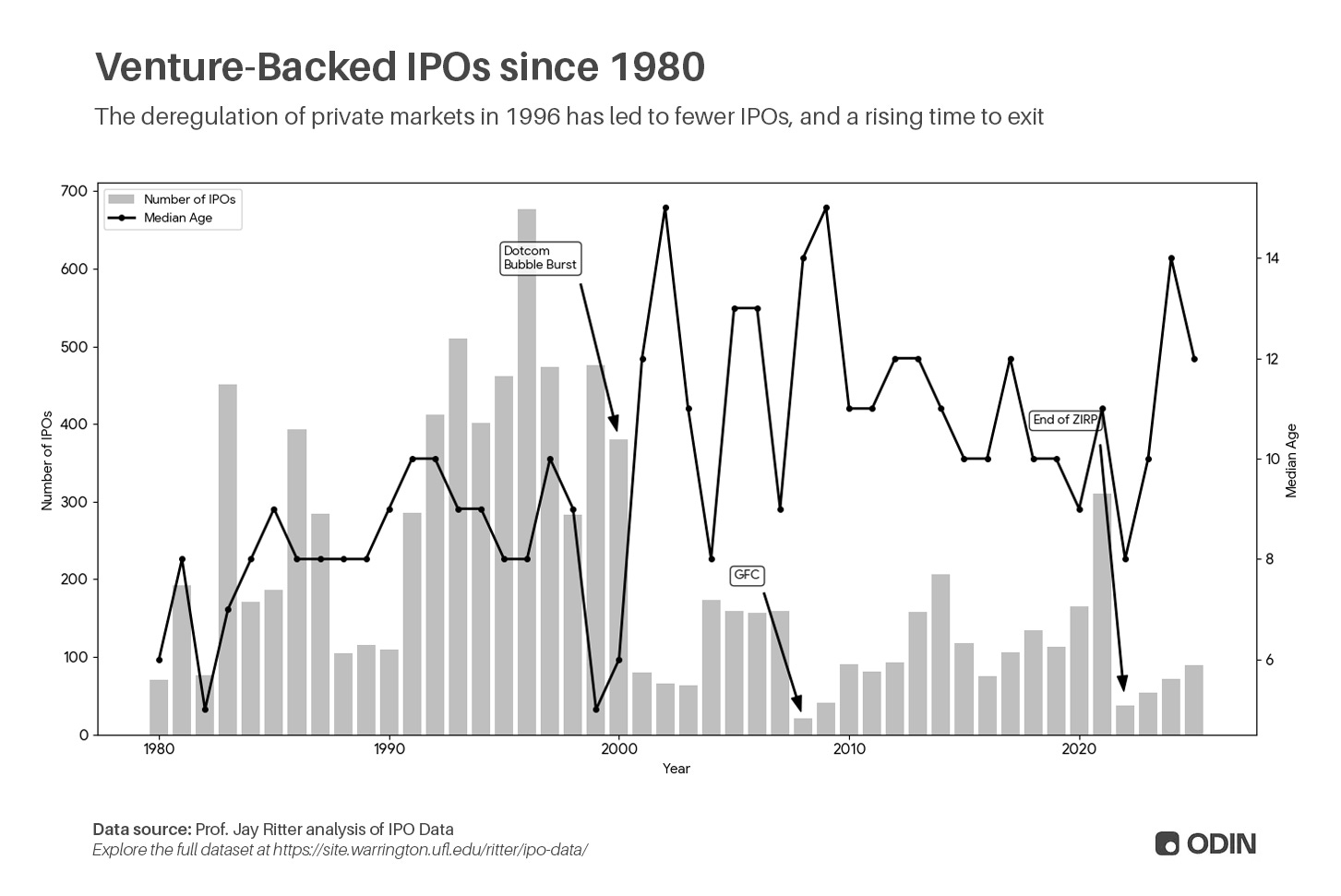

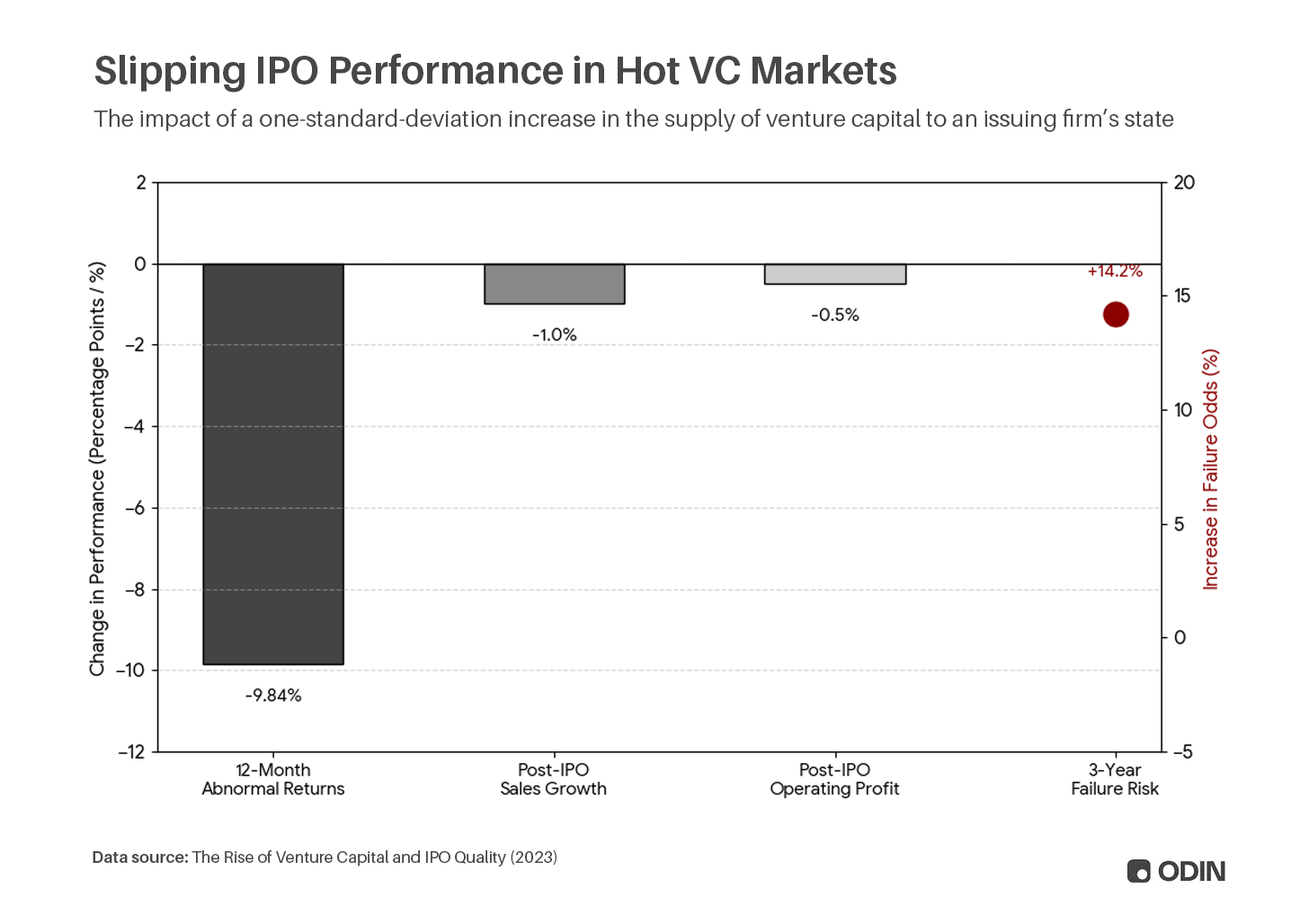

Here’s the slightly uglier truth: an IPO window is appealing because it’s easier for lower quality companies to go out with a herd. Few want to be the first out, but plenty will pile into a broad surge (like the ~1000 companies that exited in Q4 1999–Q1 2000 and Q2–Q3 2021) where going public becomes easier.

“The IPO market has significant time variations over time and IPOs issued during the high-volume period are more likely to have worse performance on average than those issued during other periods.”

Essays On Ipo Cycles And Windows Of Opportunity (2021), by Meng Chen

If you’re the CEO of an outstanding company, in great financial health, you can IPO virtually whenever you like and the market will reward you with less competition for attention. However, if you’re not actually doing that well, and your timeline may be accelerated with pressure to create liquidity, you can squeeze out in a crowd if you play into the right narrative. A greater number of recent IPOs lowers the information cost of going public as there’s much more to benchmark against. You’re less likely to attract detailed scrutiny, as investors simply have too much volume to carefully analyse every opportunity in what is likely a less rational market already. .

Indeed, hot IPO markets (IPO windows) are often triggered by a few excellent companies going public, followed by a swelling stream of exits of decreasing quality. As this becomes obvious over the following months, with more time to absorb the actual performance of these companies, the market will freeze and liquidity will diminish.

What Stops Companies Going Public?

Extreme Idiosyncracy

As described above, private markets price-in large amounts of risk, because of the intrinsic opacity and information asymmetry. Early in a startup’s life, that’s a reasonable cost of doing business. Later on, as the company matures and produces more predictable financial performance, it becomes the burden which makes private capital feel expensive.

However, some companies remain intrinsically risky for a long time, by the very nature of their activity. A good example is SpaceX. Up until recently, with the proving of Starship and the growing profitability of Starlink, SpaceX seemed like an extremely risky company and so required private investors to keep the business going.

However, examples of sustained idiosyncratic risk more than 10 years into the life of a company are extremely rare. Today’s frontier companies, Anthropic, OpenAI and Cohere, are considering IPOs on much shorter timeframes as their idiosyncratic risk is much lower (it’s broadly accepted that AI is a huge opportunity), even if their systematic risk (exposure to a speculative bubble) is much higher.

Financial Health

“The roles have reversed. In the dotcom bubble there wasn’t much VC money, and companies went public to get the stupid money at crazy prices. Now you get the crazy prices privately, and if you go to the public market you have a reality check.”

Once upon a time, venture-backed companies would go public somewhere between 5 and 8 years. The central question of venture capital was whether or not a startup could scale into a large, mature business with positive cash flow and sustainable competitive advantages to offer an attractive proposition to public markets.

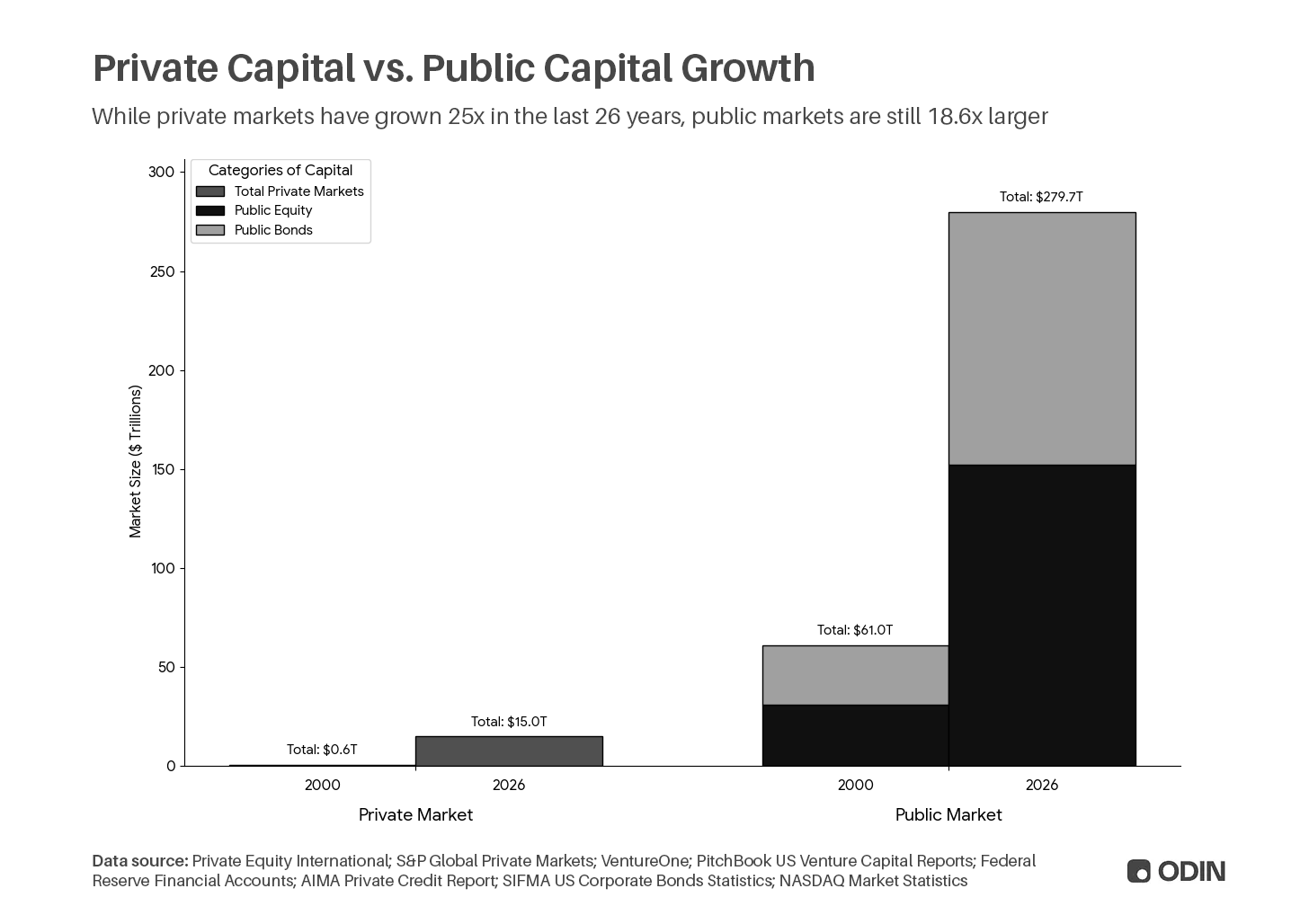

As private markets have seen greater deregulation over the last 50 years (most notably via NSMIA, in 1996), venture capital has become bloated with the growing capital inflows. On one hand, this is a huge positive for entrepreneurship (more money!), but on the other hand it has warped incentives and outcomes significantly.

Today, venture-backed companies go public somewhere between 12 and 14 years, in large part because large growth rounds give VCs somewhere to put all of this capital. See, for example, the Series L of Databricks in December 2025. Generally speaking, private market investors want growth regardless of risk, and with less concern for economics. Exposure to these incentives over long periods of time risks creating brittle businesses with high growth and lofty valuations and an unusual amount of risk.

Indeed, the brand of “founder friendliness” that has developed alongside this new funding environment has explicitly encouraged founders to embrace more risk in order to drive growth.

“The VCs get the founders to pursue high-risk strategies like blitzscaling, underwater expansion, regulatory entrepreneurship, and venture predation. In compensation for the risk they bear, the founders receive private benefits. They can cash out in secondary sales, indulge in a little self-dealing, avoid public criticism and lawsuits, and benefit from a soft landing.”

Risk-Seeking Governance (2023), by Brian J. Broughman and Matthew Wansley

The outcome is essentially that valuation growth is held-back in private markets, under much looser conditions, producing businesses which are much more valuable on paper but perhaps don’t really have the fundamental strength that a public market investor would expect. Thus, the IPO process can feel like an incredible hurdle, and many supposedly “IPO ready” unicorns from the last decade will simply never make it.

For those that make it out, they might do so at a lower price than their last private round, or they may see returns slip fairly quickly. Or both.

Preference Stacks

Finally, the other main issue which discourages IPOs is the ubiquitous use of preferred stock in venture capital transactions.

Over the lifetime of a company, each institutional funding round is likely to have at least a 1x preference, meaning that those investors are entitled to at least a 1x return on their capital in the event of a liquidity event. This downside protection doesn’t move the needle with successful exits, where there’s enough for everyone, but it becomes crucial if the value of a company slips.

In an IPO, it’s typical for all share classes to be converted to common stock. All preferences are wiped out, and thus downside protection evaporates. For growth investors who contributed huge sums of capital to an IPO, this becomes a major headache if the company slips significantly from the marked price.

In some cases, investors will include terms which provide downside protection in the event of an IPO, such as guaranteed return or IPO veto provisions. Similar to preferred stock, these clauses structurally shift value towards protected investors, away from common stock holders. Here, it is the founders and employees who may feel discouraged to go public until the company is in better shape, as their shares are effectively underwater.

“The postmoney valuation metric overvalues all unicorns in our sample, but the degree of overvaluation varies dramatically. The average unicorn in our sample is overvalued by 50%. There is a large variation in the degree of overvaluation: while the 10 least overvalued companies are overvalued on average only by 13%, the ten most overvalued companies are on average overvalued by 170%.”

Squaring Venture Capital Valuations with Reality (2017), by Will Gornall and Ilya A. Strebulaev

The Scale Factor

It’s certainly true that going public became more expensive in the post-dotcom era, as regulation drove up compliance costs. The most significant update to requirements, Sarbanes-Oxley, was designed to mitigate the risk of fraud by companies like Enron, and many other bad apples that snuck out in the dotcom IPO window.

However, while the increased cost has raised the minimum threshhold (companies must be able to afford the process), it does not make the case that bigger is necessarily better. The shift to fewer, larger IPOs has largely been attributed to the expansion of private markets, artifically and cyclically suppressing the cost of capital.

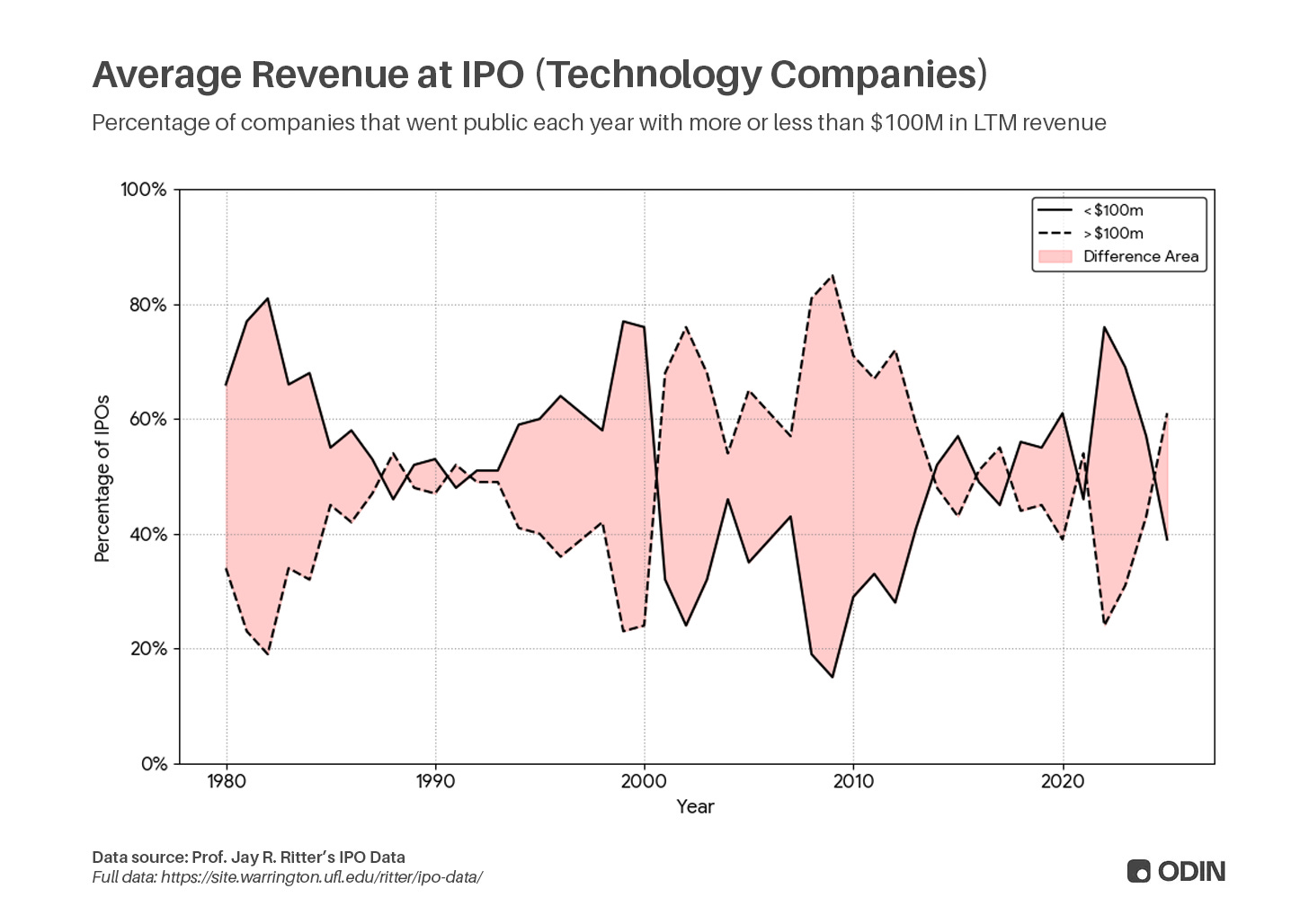

It’s easy to look at post-IPO performance data and draw the conclusion that IPOs of companies with more revenue will have deliver stronger returns.

As a result, many VCs talk about the challenge of delayed exits in terms of the volume of revenue a company must achieve in order to go public. This is an unfortunate misread, rooted in venture capital’s obsession with revenue as a proxy for success.

Public markets want quality businesses, which means solid growth, healthy margins, large markets and strong competitive positioning. Scale of revenue has a loose correlation with “quality” but it is far from causal. Bigger is not necessarily better.

“According to this analysis, the larger you are, the better your metrics on essentially every dimension. This is not a surprise for one simple reason: selection bias.

Companies with billions of dollars of ARR implicitly have leadership positions in large markets supported by durable growth and strong unit economics that have allowed them to ‘grow out of’ the smaller buckets (and quite quickly). Smaller companies are less valuable due to business quality, not due to scale. If you’re a smaller company and not growing fast, you might get ‘stuck’ in the lower buckets.

Based on the chart above, it might be reasonable to assume that there is a ‘size premium’ for larger SaaS companies. Is that really the case? The short answer is no, not really. The chart below is a regression of revenue multiple vs. ARR scale. There is little correlation between scale and valuation multiple in the public markets: R-squared = 0.11. We’ve removed Adobe and Salesforce from the chart for the sake of visibility, but even when including those, the correlation is still only R-squared = 0.02. That said, the trend line is up and to the right – a symptom of the selection bias mentioned in the prior paragraph.”2024: When to IPO in the Age of Uncertainty, by Alex Clayton and Cathy Choi

Unfortunately, with scale as their only measure of success, many venture capitalists believe that companies must simply be larger to be more attractive. Thus, they end up compounding the problem by focusing even more aggressively on that one dimension, to the detriment of others.

This hints at the truth of venture capital’s exit problem, which is not that the bar to go public has risen, but rather that venture-backed companies are fundamentally weaker.

Projecting this “growth at all costs” revenue obsession onto public markets has had a number of toxic consequences:

Delayed exits

Public market stagnation

Indeed, the final point is probably the most concerning.

In overemphasising the importance of scale, venture capital has prioritised business models and technologies that are rapidly scalable — most obviously characterised by the 2010s era of SaaS. In a decade where the cost of capital was remarkably low, due to low interest rates, there was remarkably little technological progress.

This has obvious connections with the problem of financialsiation.

“The VC business model favors innovations that promise large returns in a medium time frame with minimal risk. Such criteria necessarily deprioritize large swaths of socially valuable innovations with longer, riskier development timelines.”

Enhancing the Innovative Capacity of Venture Capital, by Peter Lee

IPOs Are the North Star for Venture Capital

Ultimately, venture capitalists need to remember that their fundamental goal is to generate returns, not to generate faster markups on larger pools of capital, even if their own LPs might appear confused by that at times. In this context, more companies heading for public markets sooner, and in better health, is the best outcome for everyone. Particularly for investors that may hold onto (some of) the public stock to enjoy the growth enabled by public market capital.

Similarly, we need to shift the debate away from exits as an end to the story for innovation, which clearly isn’t true. Many of the most obviously innovative companies (Amazon, NVIDIA, Meta, Apple) had early IPOs and obviously built incredible success stories in public markets.

"I’ve been very outspoken about staying private as long as possible. I don’t think it’s that necessary to do that. [Going public] is actually a valuable process. Having gone through a terrible first year as it made our company a lot stronger. You have to know everything about your company. It took us to the next level and we run our company much better now."

Today’s anxiety about market dips seems fairly trivial compared to the post-dotcom crashes experienced by companies like NVIDIA and Amazon, which likely played a part in the incredible discipline that those companies operate with today.

If there is a moral goal to venture capital, beyond generating returns, it is to support the growth of innovation and economic prosperity. A huge amount of that happens in public markets, and the desire to claw that growth back into private markets is short-sighted. It’s not an environment that is conducive to long-term company health.

All great companies go public, and it is venture capital’s responsibility to provide a fertile environment for great companies at the earliest stages.

Investing in the next big public company? Try Odin, your full-stack partner for private markets SPVs and fund administration.