No Crying in the Casino

How financialisation taps into our gambling gene

“Speculators may do no harm as bubbles on a steady stream of enterprise. But the position is serious when enterprise becomes the bubble on a whirlpool of speculation. When the capital development of a country becomes a by-product of the activities of a casino, the job is likely to be ill-done.”

John Maynard Keynes, The General Theory of Employment, Interest, and Money (1936)

Meme stocks. Crypto. Leveraged bets. Prediction markets. VCs white-knuckling $2B Seed rounds.

Savings at an all-time low, debt at an all-time high.

More than ever, capital feels impatient. Creating wealth has become a game of taking big shots with long odds, hoping to get lucky.

Gambling has infiltrated every part of the economy, top to bottom; institutional and individual. It has shaped how younger generations behave, and the direction of technology investment.

Welcome to Casino Culture.

The Roots of Financialisation

To understand Casino Culture, you must first understand how we arrived here. That’s primarily via a process known as “financialisation”, which describes the gradual dislocation of capitalism from productive activities within the economy.

In practice, financialisation means economic rewards shift to capital owners, away from those responsible for production. It is the opposite of industrialisation, during which investments in manufacturing and infrastructure increase, shifting economic rewards from capital owners to production.

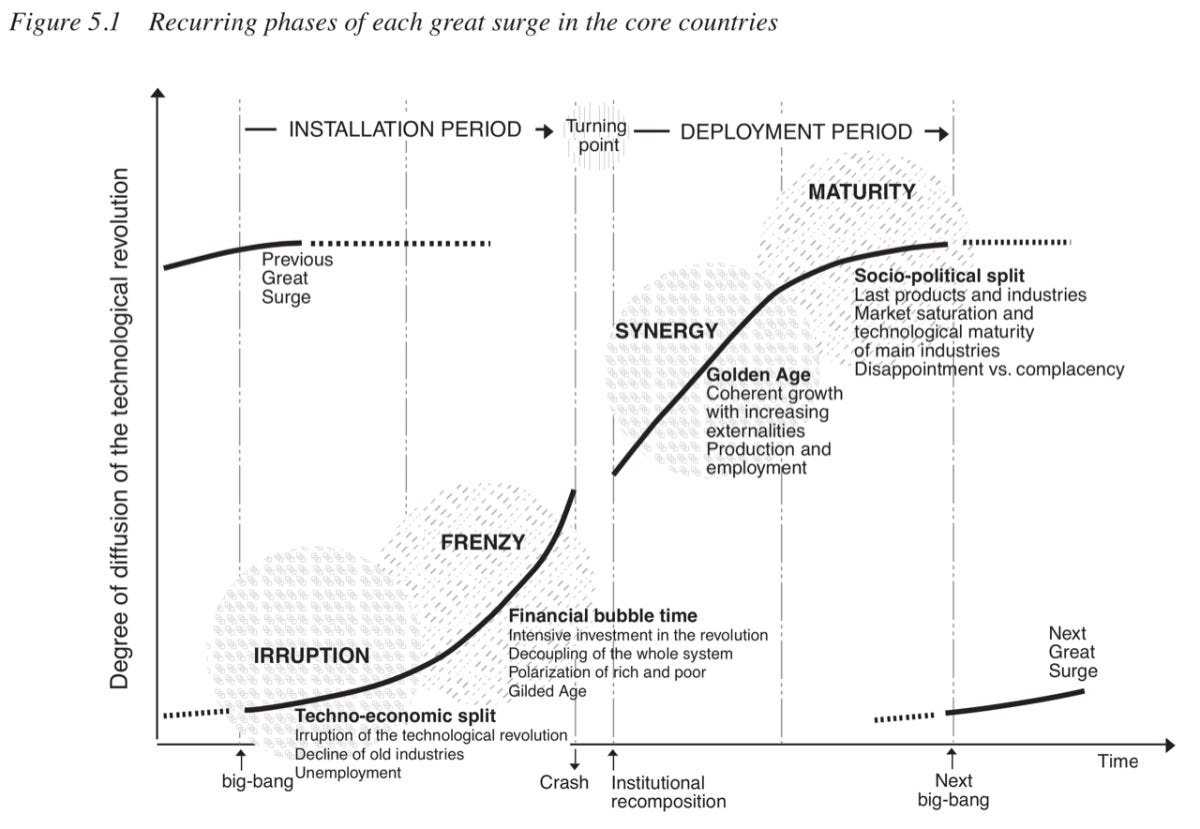

The cycling between these two forces, in response to major technological revolutions, is a central topic of Technological Revolutions and Financial Capital by Carlota Perez. In the early stages of a market boom (the “installation period”) there is a heavy focus on financing capital requirements along with a layer of raw speculation. At some point, the market corrects (the bubble bursting) and the market enters a new productive phase (the “deployment period”) where the new technology is rolled out across the economy, broadly driving prosperity.

In a healthy economy, a full cycle seems to occur every 40–60 years or so, and these are broadly positive for driving human progress. However, the West is at around 50 years of unmitigated growth in financial services and industrial stagnation.

From a policy perspective, financialisation has been enabled by deregulation of the financial markets (e.g. The Nixon Shock, GLBA and NSMIA in the US), and money printing disguised as smart fiscal policy (“quantitative easing”). As a result, companies have been incentivised to seek success through financial engineering. Shareholders focus on metrics that proxy performance in the financial market, rather than economically productive activities.

Consider the recent decade of low interest rates, a period that could have seen unprecedented growth in manufacturing and infrastructure. Instead, financialisation manifested a generation of “asset-light” businesses, built to efficiently convert the abundant capital into inflated valuations and shareholder returns. Capital collected in pools, rather than flowing out to productive activities.

Going back to its roots, financialisation began with mercantilism and bullionism between the 16th and 18th centuries. At a time when international trade was usually paid for in precious metals, politics ended up favouring the gross accumulation of precious metals as the indicator of success, rather than a more active and productive trade economy. This shift, and the associated “zero-sum” thinking, underpin many of today’s economic woes.

“The great affair, we always find, is to get money... It would be too ridiculous to go about seriously to prove that wealth does not consist in money, or in gold and silver; but in what money purchases, and is valuable only for purchasing.”

Adam Smith, The Wealth of Nations (1776)

Profits Without Prosperity

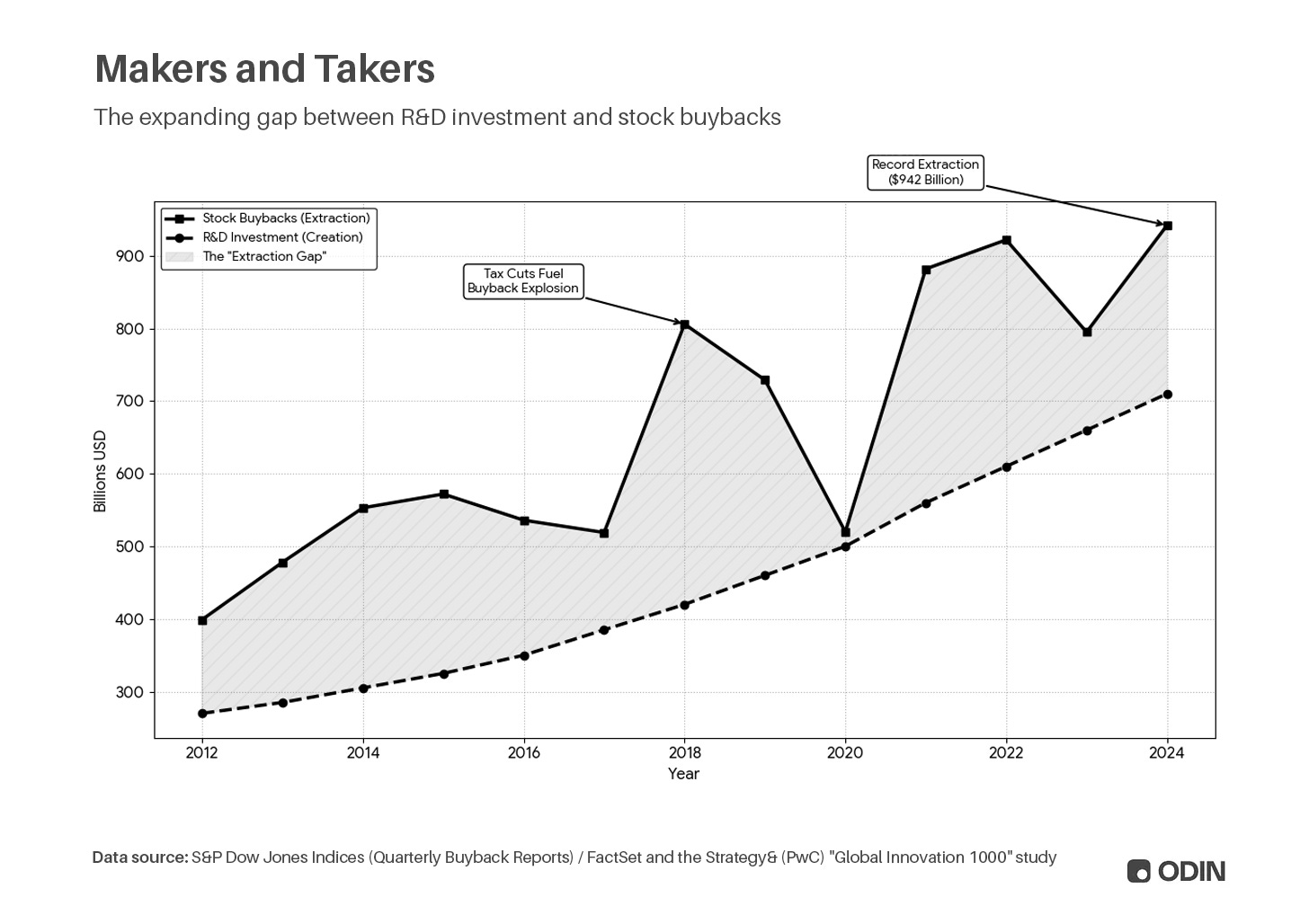

The preference for accumulation is reflected in how public companies pursue market capitalisation as the metric of success. For example, the growing trend of distributing earnings via dividends, or spending cash on stock buybacks (repurchasing shares to reduce supply, inflating earnings per share (EPS) and stock price), rather than investing capital in productive activities like R&D or capital expenditure. Essentially, rather than engage in productive activities that generate more value, companies will manipulate reality via metrics and ratios to inflate their market cap.

While this activity makes sense to a certain extent, driving value for shareholders, it risks producing “hollow” companies with inflated valuations that ultimately erode the productivity of the wider economy.

“For U.S. manufacturers, the ratio of dividends paid to the amount invested in capital equipment increased from the low 20 percent range in the late 1970s and early 1980s, to around 40 percent to 50 percent in the early 1990s, to above 60 percent in the 2000s In other words, rather than reinvesting in capital, market pressures have forced companies to keep share prices high by paying greater dividends (or by undertaking share buybacks).”

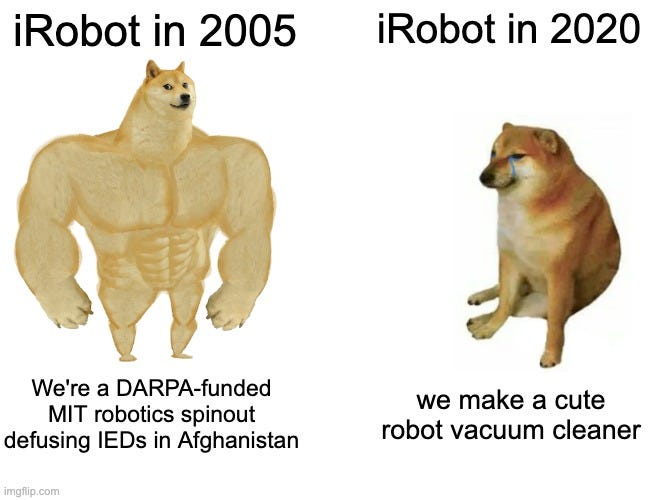

We Had Robots, Once

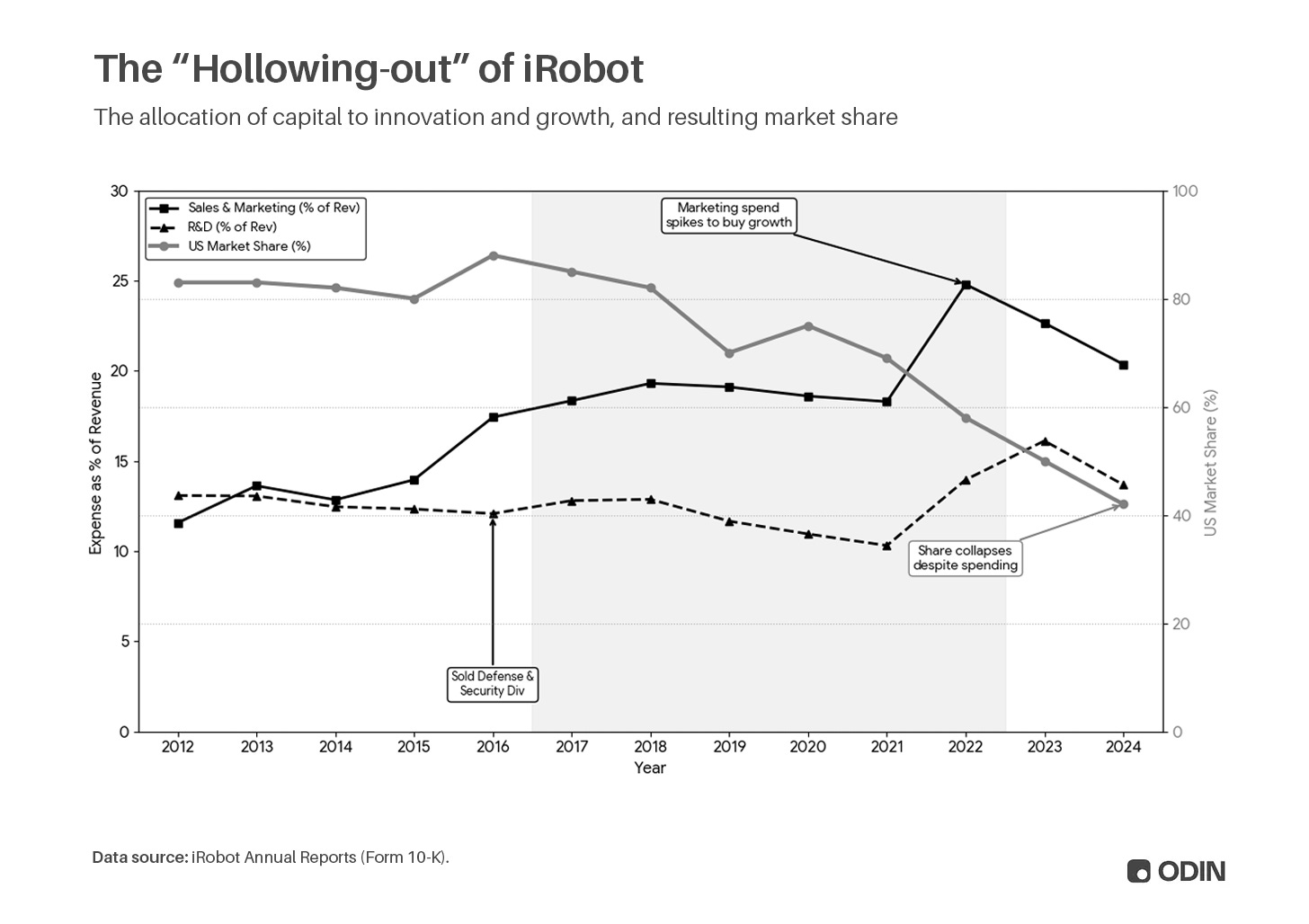

Across the 2010s, outsourcing production allowed iRobot to shed fixed assets (factories) and inventory risk from its balance sheet, boosting return on net assets (RONA) and return on equity (ROE) by reducing the capital denominator. At the same time, cutting R&D expenses increased free cash flow, which was redirected into share buybacks rather than new product innovation. This inflated the company’s earnings per share (EPS), creating a feedback loop that drove up the stock price and shareholder compensation.

In the process, iRobot was repositioning itself as a “smart home” technology company with more attractive valuation multiples (P/E, P/B ratio, etc), rather than a less exciting “appliance” company. This led to hiring large numbers of software developers, while selling off the defence and security arm of the company along with its US manufacturing base. In the years that followed, staying ahead of the competition relied increasingly on sales and marketing spend, rather than sustaining technical moats.

This is the story of a cutting-edge DARPA-funded MIT robotics spinout (responsible for everything from defusing IEDs in Afghanistan to search and rescue efforts after 9/11) being transformed into a distributor of commodity robotic vacuum cleaners, manufactured overseas. Ultimately, and inevitably, the business faltered when the company lost control of its own product, allowing its monopoly to be eroded by more innovative alternatives.

iRobot offers one example of the wider systemic problem associated with financialisation. As such, much of the apparent economic growth of the last few decades has looked good on paper, despite a feeble reality marked by long periods of stagnation. The benefit has been overstated in financial reporting (see Goodhart’s Law), without having a proportional impact on general prosperity and opportunity for individuals.

Debt to the Centre

“When one has too much student debt or if housing is too unaffordable, then one will have negative capital for a long time and/or find it very hard to start accumulating capital in the form of real estate; and if one has no stake in the capitalist system, then one may well turn against it.”

From the individual’s perspective, financialisation limits opportunity to participate in wealth creation, as the economic upside is concentrated in the hands of capital owners. If companies are pushed to reduce R&D, capital expenditures and domestic workforce to optimise financial metrics, they become top-heavy. As this spreads through the economy, it suppresses wages and deepens inequalities.

In an industrial economy, money is simply the liquid unit of value which makes the system more efficient. It’s a tool with which you may do important things, not important itself. Money has value because it allows you to have a nice house, a good car, and a pleasant lifestyle. Your primarily economic role is the production and consumption of goods or services, driving (and benefiting from) the “invisible hand” of prosperity.

“Money has the same relationship to real wealth, that is to actual goods and services, that words have to the physical world. And as words are not the physical world, money is not wealth; it’s only an accounting of available economic energy.”

Alan Watts, Writer and Philosopher (1968)

In a financialised economy, the unequal distribution of opportunity is subsidised with financial products. You’ll take a mortgage to buy a house you can’t really afford. You’ll lease a car and put vacations on your credit card. Day-trading stocks or buying crypto makes it feel manageable; there’s a chance you’ll earn your way out of the permanent underclass. Your primary economic role is debt to the centre, and the system is designed to hold you there.

“Banks are using increasingly sophisticated models to predict which customers will borrow more if their limit is raised. For many, that means an automatic increase they never asked for and may not fully understand. These decisions are shaping household debt across the country in ways most borrowers don’t see.”

Dr Agnes Kovacs, Senior Lecturer in Economic at King’s Business School

The Gambling Gene

“Buying a lottery ticket is the only time in our lives we can hold a tangible dream of getting the good stuff that you already have and take for granted.”

Morgan Housel, The Psychology of Money (2020)

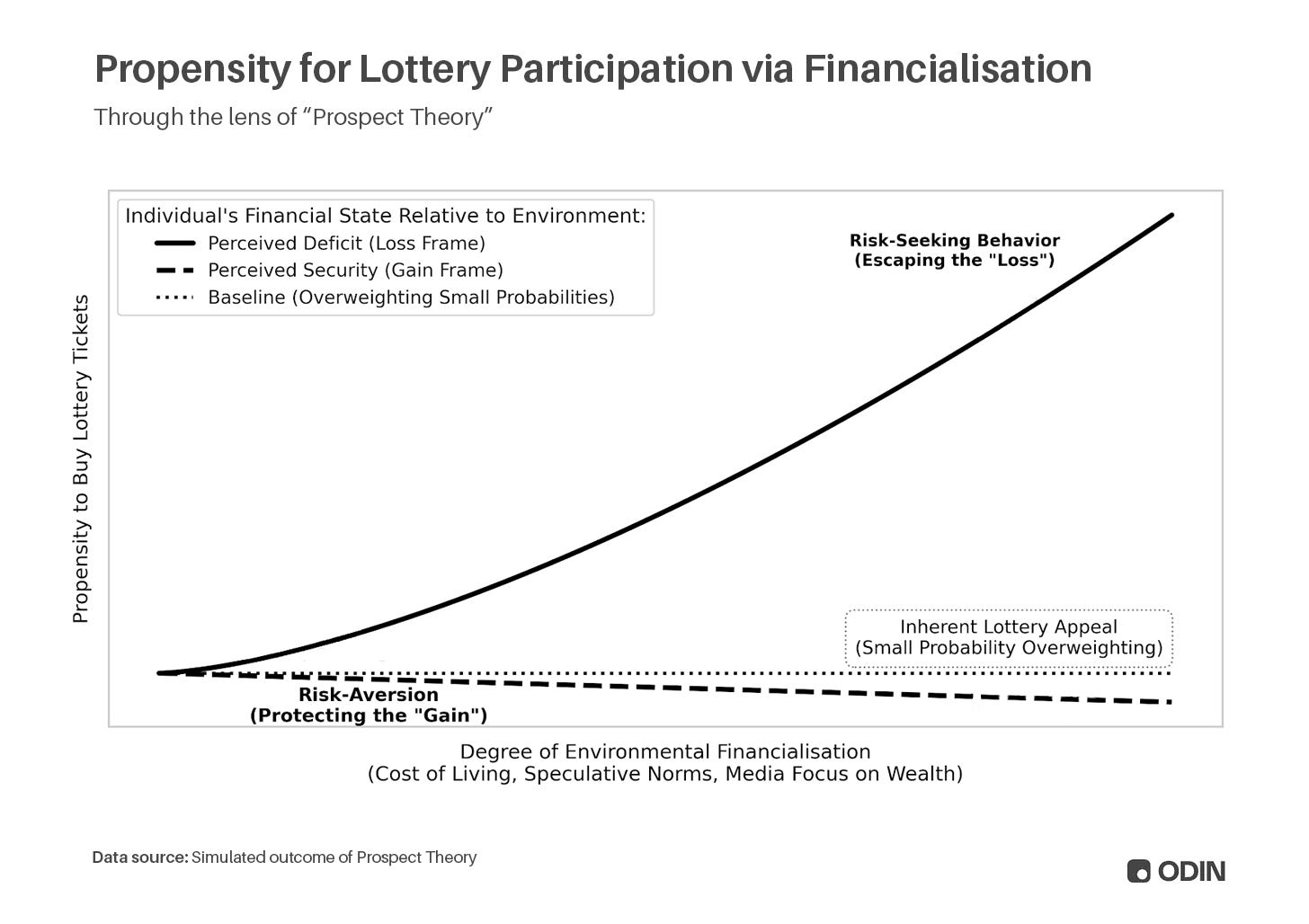

In periods of economic stress, financialisation has evolved to exploit our tendency to overweight long odds of extreme rewards, which economists Daniel Kahneman and Amos Tversky described as Prospect Theory:

“People underweight outcomes that are merely probable in comparison with outcomes that are obtained with certainty. This tendency, called the certainty effect, contributes to risk aversion in choices involving sure gains and to risk seeking in choices involving sure losses.”

For example, if you are chasing wealth, you’re more likely to use debt to buy lottery tickets, because we are cognitively wired to prioritise the extreme (and unlikely) reward more than the small (and certain) cost. On the other hand, a person who is already wealthy will prioritise avoiding loss, and is therefore less likely to buy lottery tickets they can easily afford.

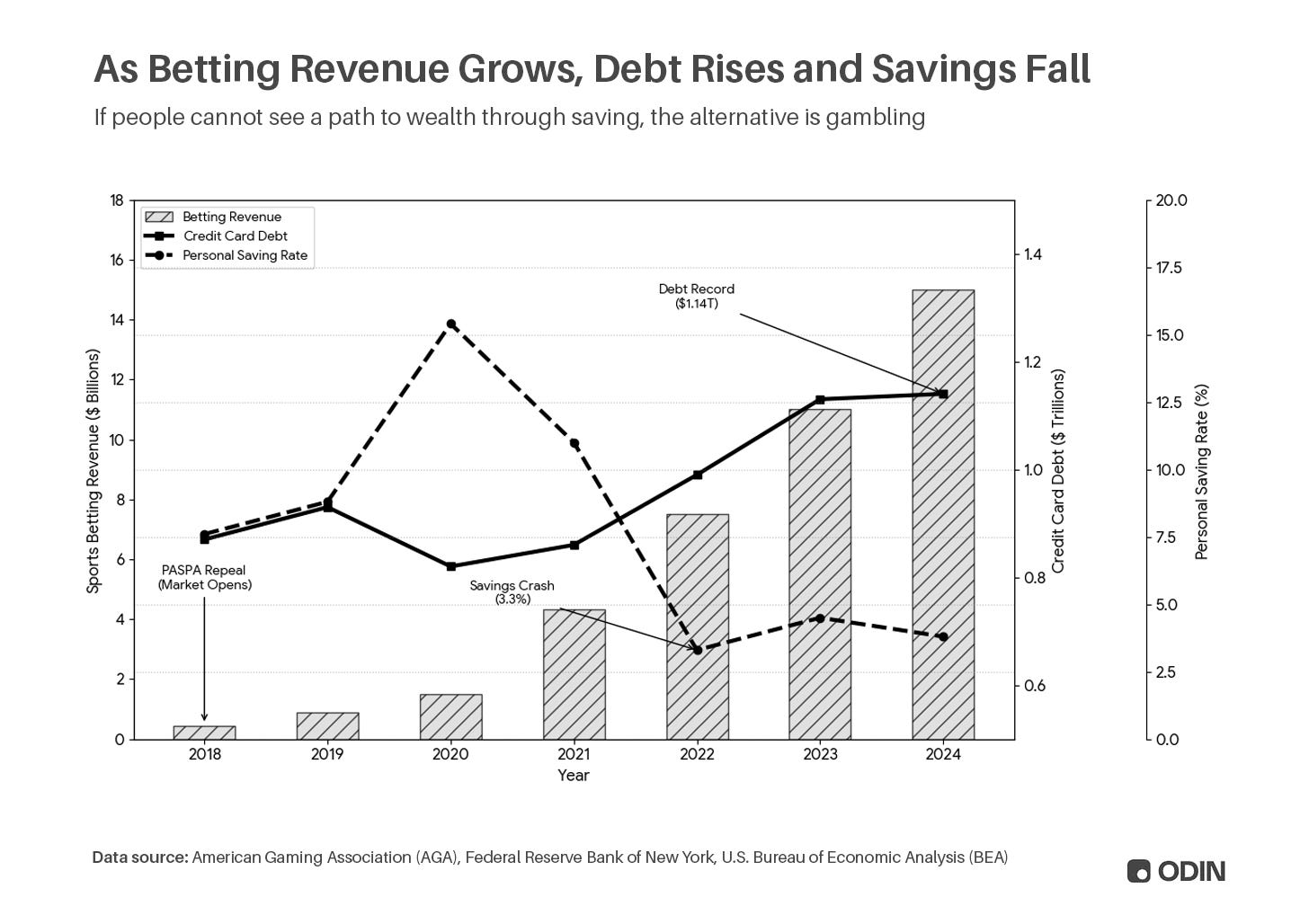

The result, as financialisation deepened over the last fifteen years, has been a significant shift in behavior from saving into debt and gambling. US Sports betting revenue rose from $0.4 billion in 2018 to $13.8 billion in 2024, while credit card debt rose from $870 billion to $1.14 trillion across the same period.

This behavior masks much of the poor health of the economy, as purchases made with debt still appear as consumption of a good, and gambling as the consumption of a service.

As this attitude spreads across the economy, there’s an increase in the rate of gamblification. Whether it’s sports betting, meme stocks, altcoins, gamified brokerages, or ripping through video game loot boxes and Pokemon packs, social media is full of people desperately pursuing wealth by rolling the dice.

Perhaps even more worrying is the scale of audience this activity generates, reaching another level of abstraction from real wealth where viewers live vicariously through the performer. This content is bringing a new generation of young adults into an environment where gambling is entirely normalised, if not celebrated.

“Although loot box related activities significantly predicted frequency of participation in monetary gambling activities (opening free loot boxes, paying for loot boxes, and selling items from loot boxes) and perceived normative pressure (selling items from loot boxes), other activities are of greater importance. More specifically, all tested monetary gambling outcomes could be significantly predicted by the viewing of gambling streams - or videos that include gambling behavior.”

Of course, the house always wins. Whether it’s harvesting order flow data, collecting fees, or just the negative expected value of gambling, existing capital owners come out ahead of individuals who have to meet liquidity demands on less predictable, shorter-term horizons.

Finance Eats Innovation

Since 2011, Silicon Valley’s thesis has been “software eats the world”. Perhaps more accurately it should have been “finance eats the world”. Despite a reputation for contrarianism and independence, venture capital unfortunately exhibits all of the flaws associated with financialisation with the associated preference for accumulation.

In the era of low interest rates, software offered VCs a vehicle to convert venture dollars into inflated asset values and fee income. Negative-margin businesses were scaled at a huge loss, only to be marked-up on multiples to justify further investment. Capital chased capital in an inflationary cycle, as the “best” deals became those that were the most likely to attract more investment. Similar to share buybacks, this created brittle market leaders with inflated valuations.

This particular era of financial engineering died out with the low-interest-rate environment in 2022, and the subsequent correction washed out much of the “paper” accumulation. The market remains in the tail-end of the hangover, with the collapse of liquidity felt in weaker fundraising across all subsequent vintages (albeit primarily by peripheral hubs and “outsider” managers).

Still, the problem persists. Managers aren’t immune to Prospect Theory, and the parallel with “buying lottery tickets” and today’s investment activity is clear: as incumbents capture the centre via accumulation, the general response is to greatly overpay for any deal that might produce an extreme outcome. “Power law” now shapes entry more than it explains exits, as investors rush toward the endgame.

Worse still are the investments which exploit the behaviors entrenched by such a long period of financialisation. You can gamble on your bills, you can bet against insiders on prediction markets, or try your hand in the poorly-regulated crypto casinos. Thus, the desperation of late-stage financialisation brings us financialisation squared; investors seeking scalable models that print markups based on exploiting the economic stagnation created by financialisation.

Ultimately, this is a choice which investors will be held accountable for. Investors can coast on the tail-end of financialisation, and the products which enable it, all the way to the bitter end. Or, they can be part of the correction, backing the companies that help to deliver long-term prosperity through industrialisation.

The Obstacle is the Way

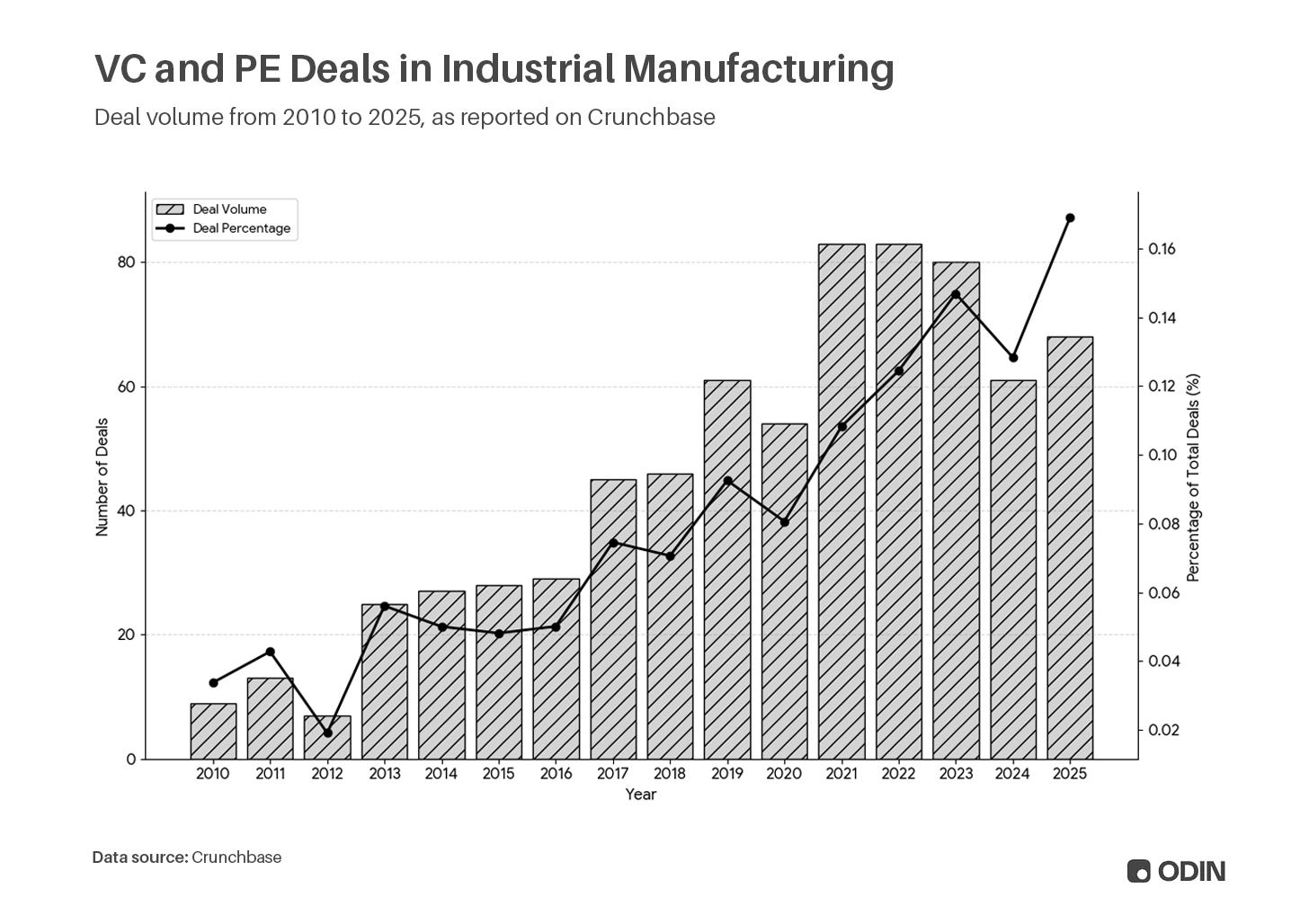

Despite adverse incentives (slower growth, lower multiples) and subscale activity, sectors like industrial manufacturing are on a steady march upward.

It’s not clear whether this signals a cycle back to industrialisation, or whether there’s just a growing recognition that the status-quo is not sustainable. Indeed, as more capital concentrates into fewer investors, flowing through to fewer companies, there is implicitly a growing number of investors and builders who do not feel like they have a stake in the current system.

Something, eventually, will break.

“This time however, things are different. With the current ICT revolution, we seem to be stuck in the installation period or in what I call the ‘turning point’, which is the mid-way time of recessions and uncertainty, revolts and populism that reveals the pain inflicted on society by the initial ‘creative destruction’ process. It is precisely when the system is in danger and is being questioned and attacked that politicians finally understand they must set up a win-win game between business and society.”

A long delayed golden age: Or why has the ICT ‘installation period’ lasted so long? by Carlota Perez

As Perez describes, the turning point has typically been spurred by government action. While the current US administration has made some progress with industrial policy, there has been a continued drift toward deregulation. As a result, this could be the first time an industrial economy has quietly emerged in parallel to a financial economy, with the two in competition for capital and talent.

Make no mistake, industrialisation is the harder path, as managers face skepticism from their LP base and less immediately lucrative markups. Long-term, however, these “hard tech” and “deep tech” companies offer enduring moats and compounding value that can outperform the hotter sectors. More importantly, they do so by solving real problems with a direct and positive impact on prosperity.

“Reindustrialisation” is the call of technologists who recognise the tragedy of a lost future.

It’s a new uranium enrichment plant amidst a nuclear renaissance, a marine robotics startup solving critical food supply chain issues, or a specialist AI lab focused on the blue ocean opportunity of drug discovery in a world with AlphaFold.

None of these ideas benefit from financialisation. They do not easily fit around the metrics and ratios that have enabled money printing in private markets. Instead, they will make the economy genuinely productive again.

The Age of Industrialists

“The relationship between the creation of money and credit and the creation of wealth (actual goods and services) is often confused yet it is the biggest driver of economic cycles.”

Financialisation became the lazy default in a post-prosperity era of stability; a mechanism for extraction and driver of stagnation. Ultimately, it’s self-serving, zero-sum, and increasingly vulnerable to systemic shocks that wash away accumulation and all hope of recovery.

Hopefully, capital is ready to embrace “hard problems” once again. This part of the cycle is characterised by great industrialists, particularly those who operate out on the frontier. Critically, they are idealists with a vision that supersedes the shallow incentives of finance. They’ll put enduring competitive strength ahead of fragile capital moats, and legacy over short-term status games. Finance will bend to their needs, rather than vice-versa.

Meanwhile, the return of Adam Smith’s “invisible hand” will not be kind to those who keep trying to juice the metrics of investor-friendly slop.

(Thanks to those that provided feedback on the early drafts, including Yifat Aran, Alex LaBossiere, Laurel Kilgour and Aaron Slodov.)

Build and invest in the Age of Industrialists with Odin

Enjoyed the article! I think one angle you may have missed is that for the past few decades the American economy has trended towards a rentier economy in many sectors, but specifically the businesses that VC funds. SaaS as an industry extracts rents, as does all of our endless subscriptions and cloud services. Rent extraction, as described long ago by Ricardo, is probably the main target to eviscerate when transitioning to industrial capitalism. In the early days of industrial capitalism rents weee minimized and the cost of doing business dramatically fell.

Great piece. The Perez framing is spot on.

I'd push one thing further though — Gen Z gambling isn't just Prospect Theory. It's rational. When every promise you grew up on collapses, rolling the dice makes more sense than playing by rules that stopped working. That's not irresponsibility. That's adaptation.

And reindustrialisation is the right call but I think it's incomplete without a goal that's bigger than shareholder value. Otherwise you just rebuild the same loop.

The meaning gap underneath casino culture feels like the real story here.