The Frontiersmen

Adam Draper and Brayton Williams have made their mark by backing ideas from science fiction. Their debut fund was one of the most remarkable of its generation.

“I’ve always had an affinity for the fringe. I go with what I feel is the most important problem being solved by the most impressive people who are being neglected for one reason or another. I try to find that blank space.”

Adam Draper, Managing Partner and Co-Founder, Boost VC

Sometime around 2011, Adam Draper and Brayton Williams found themselves at a P.F. Chang’s in the Stanford Shopping Center, becoming friends over a topic of conversation that has always animated Silicon Valley, “What if we tried something new?”

The two initially worked together on a startup attempting to solve private company liquidity through a secondary exchange. While that idea never quite took off, they formed a strong partnership which, over the next nine years, evolved into one of the most impactful, contrarian, and ultimately successful pre-seed firms of this generation.

Boost VC’s Fund I, a $38 million vehicle raised in 2016, has already returned 4.61x to their LPs. In an era where most funds struggle to return more than 2x on horizons that stretch out to 16 years, that’s a remarkable achievement.

The firms success is rooted in a particular combination of people, philosophy, and sheer audacity. As many of the largest institutions in venture capital were straying down the path of herd behavior, Draper and Williams saw an open season on outliers.

An Insider and an Outsider

Central to the Boost VC lore is Adam Draper’s relationship with the industry. His great-grandfather, William Henry Draper Jr., co-founded Draper, Gaither and Anderson in 1959, one of the first venture capital firms on the West Coast and the originator of the limited partnership structure that the industry uses to this day. His grandfather institutionalised venture capital through Sutter Hill Ventures before helping launch the first international fund in India. His father, Tim Draper, globalised it through Draper Fisher Jurvetson, seeding nearly 700 funds across the world.

Adam Draper dropped out of UCLA and co-founded a company that he eventually sold for parts. He spent years in the wilderness of Silicon Valley trying to figure out whether his real gift was building or backing. By his own account, the answer only became clear when he started making angel investments in companies nobody else would touch. These early investments included Coinbase, when most people had barely heard of Bitcoin; Benchling, which became a $6 billion life science platform; and Amplitude, the analytics tool that went public in 2021.

“While most investors start out by making terrible investments because we don’t know anything, five of Adam’s first twenty-five pre-seed bets are unicorns already.”

But Draper’s pedigree is only half the story. Brayton Williams arrived at their partnership with almost the opposite background. A relative outsider, a Cal Poly graduate in finance and econ, Williams had no real notion of how venture capital operated, or the industry’s history. This turned out to be a superpower, as he dodged decades of accumulated bias and dogma that many career investors naturally absorb.

The partnership between Draper and Williams works because of this contrast. Draper brings the fourth-generation instinct for greatness, and a risk appetite to match. Williams brings a blank slate; a vision for how things should be done, rather than how they have always been done. Their take on venture capital is a revival of the industry’s historical contrarianism combined with a more contemporary portfolio strategy, and they’re exactly the people to execute on it.

An Appetite for Risk

Boost VC’s investment model runs contrary to much of the common wisdom about ownership targets. Where most firms concentrate capital into 20–30 companies, Boost VC disperses their investments across a large portfolio of around 120.

The thesis is that at the earliest stages, the portfolio maths of venture capital demands breadth. If 2–3% of pre-seed investments eventually become unicorns, a fund of twenty companies might miss completely, while a fund of 125 companies could hit two to four. The strategy recognises that most venture capitalists are undone by their focus on “picking”, through overconfidence in their ability or by letting insecurity push them toward consensus. Diversification solves this problem.

This is a perspective supported by research. Larger portfolios enable a greater appetite for idiosyncratic risk, as investors are more willing to make investments that may fail completely. This enlarged risk appetite captures a wider range of outcomes and generally leads to outperformance.

Essentially, by making more investments, Boost VC is able to lean further into moonshots, rather than safer feeling iterative ideas.

“Because fund diversification also affects fund risk, risk-averse fund managers are tempted to invest in companies with higher idiosyncratic (i.e., company-specific) risk when pursuing a strong diversification strategy. Doing so eventually leads to higher realized fund performance on average, since investments in riskier ventures only make sense if they come with better prospects of high returns.”

Diversification, Risk, and Returns in Venture Capital, by Axel Buchner, Abdulkadir Mohamed and Armin Schwienbacher

This approach also requires that Boost VC is able to move quickly on investments. Williams has spoken candidly about the firm’s investment approach, which allows them to reach conviction with a minimal amount of time wasted.

“You’re still typically taking three calls per founder, but we always generally believe more diligence does not get you to a better decision. You’re basically just judging, can this person do what they say they’re going to do, and are they committed for the next 20 years to do that thing?”

They recognise that the signal in a pre-seed investment is human. Nine out of ten of Boost VC’s deals come via referrals from trusted sources, and by the time a founder sits across from Draper or Williams, the firm has already run a parallel diligence process through that network. The goal of the meeting is to ascertain character, conviction and the magnitude of the idea.

Their diversified strategy also helps the firm manage systematic risk. As Boost VC spans sectors including cryptocurrency, virtual reality, artificial intelligence, space, biotech, and nuclear energy, a collapse in any one corner of the market is unlikely to harm the overall fund. A downturn in crypto doesn’t touch a space company. A regulatory crisis in biotech has no bearing on a VR startup.

Another benefit of their strategy is a price advantage. Being the first money into extremely idiosyncratic ideas means they are typically investing at valuations between $3 million and $7 million, well below the median for pre-seed. While other investors complain about prices creeping upward due to increasing concentration and consensus, Boost VC’s average ownership for $500,000 has gradually increased.

Early Crypto Returns

The companies in Boost VC’s first fund cover a spectrum of technological imagination from the mid-2010s, some of which has become reality and some of which remains aspirationally strange. It certainly isn’t the more typical dull cocktail of enterprise SaaS solutions of that era.

Their most consequential relationship, with crypto, began with Adam Draper’s investment into Coinbase in 2012 and was followed by the Fund I investment in 2016. When Coinbase went public via direct listing in 2021, the company reached a market cap of over $85 billion. That track record helped establish a reputation for truly understanding crypto before any other institutional investor. In fact, Boost VC was among the first funds to hold Bitcoin as a portfolio investment.

“Boost VC was one of the first funds, if not the first, to buy bitcoins as portfolio investments. That enabled them to return 1.5x the fund during Venture Capital’s worst year.”

Within Fund I’s direct portfolio, the returns have been driven by a cluster of winners that demonstrate the significance of their early crypto conviction:

Polychain Capital, the crypto hedge fund founded by Coinbase’s first employee Olaf Carlson-Wee, returned more than 90x to Boost VC’s limited partners despite the fact that many investors had passed because its structure was not a conventional Delaware C-corp.

Etherscan, the Ethereum blockchain explorer that became the default transparency layer for the entire ecosystem, turned into one of the most important blockchain infrastructure plays in the portfolio.

Decentraland, the blockchain-based virtual world that anticipated the metaverse wave years before the term entered the mainstream, and another example of a category that the rest of the market would later pile into.

Polkadot, the blockchain interoperability protocol developed by Ethereum co-founder Gavin Wood, another major infrastructure project in the crypto ecosystem.

21Shares, the Swiss crypto exchange-traded product issuer, was acquired in a deal that pushed it past a $1 billion valuation in 2025.

Then there is the recent phenomenon of Moltbook. The story of Matt Schlicht, the founder Boost VC backed through his earlier company Octane AI and who later pivoted to build an AI agent social network.

Schlicht grew up at a Waldorf school where he never touched a computer. When he eventually got a laptop as a teenager he became so obsessed with building products that his school expelled him for it. He hacked the school’s systems that summer, helped them fix the vulnerabilities, and they let him back to graduate. He skipped college, moved to Silicon Valley at nineteen, and by 2016 was building crypto social products and chatbot platforms.

In March 2026, his company Moltbook was acquired by Meta, with Schlicht and his team joining Meta’s Superintelligence Labs. This decade-long story of overnight success pushed Fund I’s DPI over 4.61x.

“I love the Boost VC team. The support they have given me, no matter the situation, is so strong and rare. They were the first check in my companies. I will work with them until I die.”

Schlicht’s arc is not unusual for Boost VC’s portfolio; Williams’s instinct has always been to look for people who are constitutionally incapable of doing anything other than building, regardless of whether the world is ready for what they are building.

The portfolio also carries a substantial set of positions that have not yet reached their exit, but where the trajectory suggests the fund’s total value to paid-in capital of 7.04x still has plenty of room to run.

Ledger, the French hardware cryptocurrency wallet company, has reached valuations of $1.5 billion with IPO discussions mooted at significantly higher figures.

Unstoppable Domains, the blockchain domain name provider, has grown into one of the most recognisable brands in the Web3 identity space.

Volley, the voice game platform, has built a substantial audience across smart speaker devices and represents an early bet on ambient computing as a distinct category.

FitXR, the virtual reality fitness company, has raised over $18 million in follow-on capital and continues to grow as VR hardware becomes more mainstream.

Ripio, the Latin American crypto platform, has expanded across Argentina, Brazil, and beyond, serving a region where the use case for digital currencies has always been more urgent than the Silicon Valley imagination of it.

VennBio and Shake Labs represent the fund’s deeper investments in life science and fintech infrastructure respectively, both still in the compounding phase that Boost, by its own design, is built to be patient about.

Frontier Science

The companies that attract the most attention are not always the ones that generated the largest financial returns. Over the last decade, Boost VC has backed companies working on problems that more conservative venture firms would not put in a slide deck. De-extinction. Telekinesis-adjacent brain-computer interface research. Personal flight. Space observation networks designed not to watch Earth from orbit but to watch the cosmos from a fixed platform. VR platforms, hardware wallets, and AI voice tools when all three categories were considered too early, too strange, or too difficult to commercialise.

This is a consequence of the strategy and incentives that Draper and Williams have designed. Because they make small investments at very low valuations, they are free from the tyranny of consensus. A $500,000 investment in a company working on something that might take fifteen years to mature does not break a fund. If the technology proves out, the returns will be transformative. If it doesn’t, the fund absorbs the loss and the other 120 companies carry on. Their strategy allows them to back the ideas that other funds cannot justify to their limited partners.

Colossal Biosciences, the de-extinction company whose recent news includes the revival of the dire wolf and a $10 billion valuation, is perhaps the most vivid illustration of what happens when that philosophy catches a tailwind. When Boost VC first backed the company, the idea of bringing an extinct species back from the dead using CRISPR and ancient DNA was the kind of thing that appeared in science fiction. The company’s scientific claims have attracted significant scrutiny. But the point is not whether every bet pays off. The point is that the firm was in the room, with conviction, before anyone else was willing to be.

“Boost VC makes bold bets on the frontier. Make science fiction real.”

If you include investments made prior to Fund I, Boost VC’s core thesis has now been tested across thirteen years, four funds, and more than 500 companies.

The thesis holds that transformative technologies are systematically underpriced at inception because most investors cannot evaluate what they do not yet understand. Bitcoin in 2013. Small modular nuclear reactors in 2020, when every investor wanted SaaS and remote-first businesses. Voice AI in 2015, when speech recognition was considered a solved problem that belonged to the large technology companies. The founders who front-run the market in these categories might look like eccentrics to the average venture capitalist. To an investor like Boost VC, that eccentricity is a strong positive signal.

Run your investment firm from your phone with Odin.

Entrepreneurial Idealism

Boost VC’s success is built on a specific and unusual relationship with a certain kind of founder.

Most venture capital is designed, whether its practitioners acknowledge it or not, to select for founders who already speak the lingua franca of the industry. The pitch deck structure, the ritual dance for setting terms, the ability to turn an irrational ambition into a straight-laced investment memo. These conventions tend to advantage founders with existing access to networks and institutions, who have seen how the game is played and know the rules.

Draper and Williams are less interested in founders that cater to the venture capital industry, and more interested in how they can cater to founders.

Matt Gould, the CEO of Unstoppable Domains, a Boost VC portfolio company, described the firm in terms that capture something real about its character:

“Boost VC is one of those rare VCs with as strong a conviction in technology’s ability to shape the future as the founders of the companies in their portfolio. Brayton and Adam are both dedicated to changing the world and that passion comes through in their support and advice. Founding a company is hard. Having great investors makes it easier. You can’t get any better than Boost.”

The dynamic at Boost VC is unusual because they arrive already disposed to believe that hard, strange, long-timeline ideas are worth pursuing. The founder’s job is not to overcome scepticism but to demonstrate that they are the right person to pursue this specific version of the impossible. This is a stark contrast to the typical interaction with venture capitalists, and it turns out that matters enormously to the most ambitious founders.

The ability to identify people with the combination of technical capability, commercial instinct, and the psychological resilience required to build something new cannot be taught with a checklist of attributes or credentials. It comes from volume, attention, and a genuine openness to being surprised. Recognising the absolute idiosyncrasy of greatness.

Draper describes his investment process in terms of looking for evidence that someone is “confident in themselves enough to build a business,” able to be uncomfortable every day, and capable of learning the skills they do not yet have.

Drivers of Performance

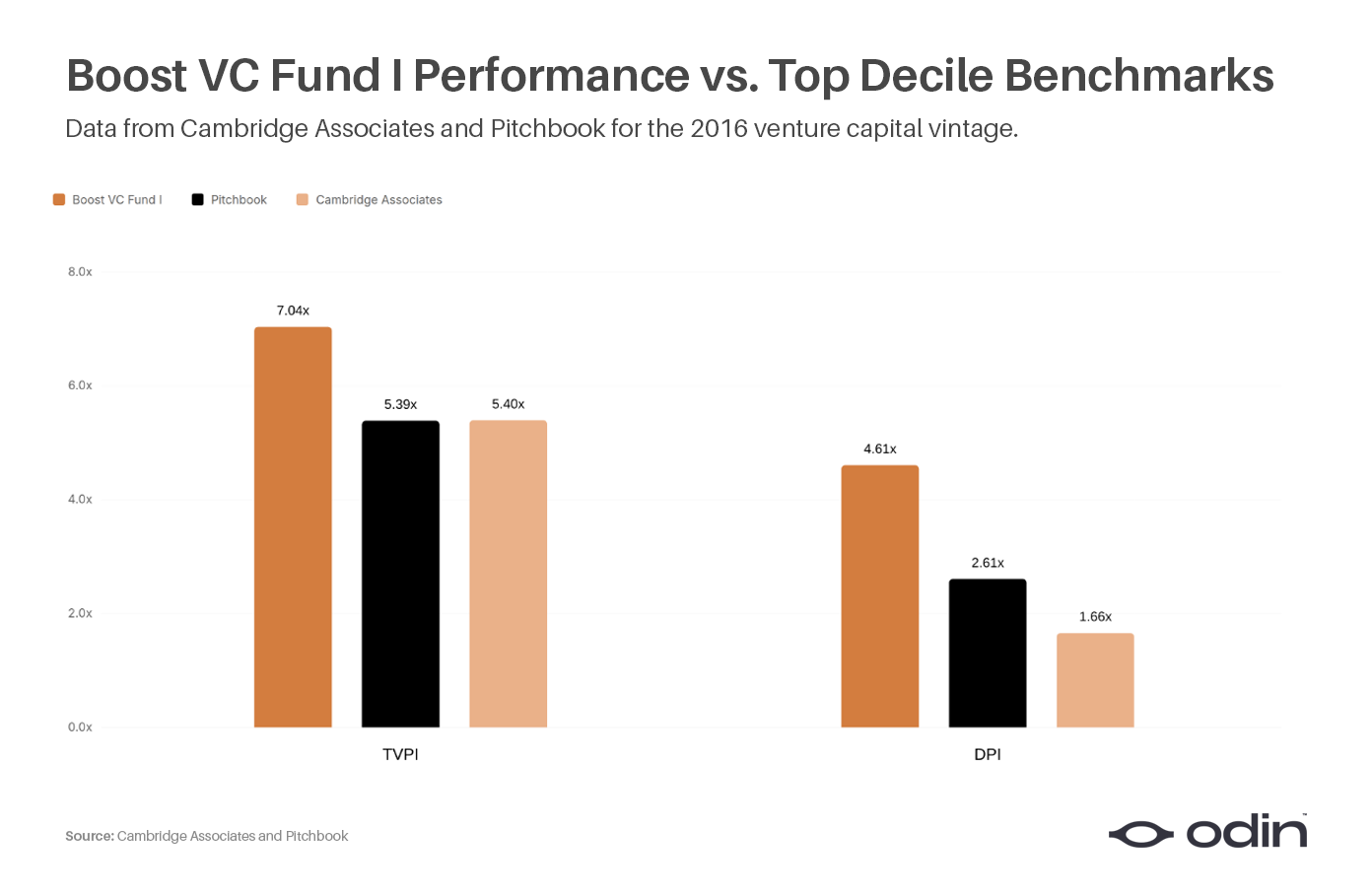

Boost VC’s Fund I will mainly be measured by its performance, which (so far) is 4.61x DPI and 7.04x TVPI, on the original $38 million. That result places the fund among the best of its vintage. For context, the top decile performance for venture capital funds in the 2016 vintage stood at 1.66x DPI and 5.4x TVPI, according to 2025 Cambridge Associates benchmarks.

In 2025 alone, the firm returned $42 million to limited partners, predominantly from Fund I, while four portfolio companies across all funds reached billion-dollar valuations, including 21Shares (acquired), K2Space, Radiant Nuclear, and one other undisclosed company.

The Radiant Nuclear offers another great example of Boost VC’s strategy at work. When a SpaceX engineer named Doug Bernauer came to them in 2020 with a plan to build small modular nuclear reactors, Boost VC made the investment in a single twenty-minute meeting. Nuclear energy was, at that moment, considered a dead category by most of the technology investment community. Capital was flowing into software, remote work tools, and anything that did not require physical infrastructure, long regulatory timelines, and the specific stigma that has surrounded nuclear since the accidents at Three Mile Island, Chernobyl, and Fukushima. Radiant is now valued at over $1.8 billion, having recently closed a $300 million Series D with Boost VC co-leading the round.

Adam Draper reflected on that in a note that captures the spirit of the whole enterprise:

“If we believe something that the rest of the investment world doesn’t, that is a scarce resource and we must act.”

Boost VC’s performance is driven by their willingness to sit in a category alone, potentially for many years, waiting for the rest of the market to catch up with them.

The Next Generation

Boost VC’s Fund IV, a $87 million vehicle that they began investing out of in November 2024, is an extension of everything described above. The thesis has not changed, and neither has their investment strategy. What has changed is the breadth and ambition of the technologies being built as dynamism grips the market. Suddenly, “hard problems” are back in vogue and Draper and Williams are in a great position to capitalise on that.

The fund is only partially deployed, and most of its companies are operating in stealth or at a stage of development where they have little public profile. The handful that have begun to emerge say a lot about how years of frontier investing have sharpened the firm’s instincts.

Icarus is perhaps the most immediately legible of the Fund IV investments. The company, which emerged from Y Combinator’s 2025 cohort, is building solar-powered stratospheric drones designed to operate at roughly 60,000 feet for weeks or months at a time. The pitch is that these platforms could serve as persistent, high-altitude infrastructure for communications, imagery, and data relay: effectively cell towers floating at the edge of the atmosphere.

FeltSense occupies a different register of ambition entirely. The San Francisco company, founded in January 2025, is building AI agents designed to function as autonomous founders; systems that can ideate, build products, launch them, and scale companies without human direction. It claims to be capable of running the equivalent of a Y Combinator batch entirely within AI, at speed and at volume. The company raised a $5.1 million seed round in February 2026, led by Draper Associates, with Boost co-investing alongside Precursor Ventures and Liquid 2 Ventures.

Then there is American Housing Corporation. Based in Austin, Texas, the company is building factory-produced modular homes shipped in standard containers and assembled on-site in days, with the explicit goal of industrialising the solution to the United States housing shortage. The company built and publicly showcased its first home within just over a year of founding. When venture capitalists had largely abandoned the physical world for software, a company trying to re-engineer how homes are manufactured and delivered is precisely the kind of heterodox idea that Boost is drawn to.

Serova Bio sits at the opposite extreme of legibility. The company is developing personalised cancer vaccines powered by machine learning, designed not merely to target the mutations currently visible in a tumour but to anticipate what those mutations will become as the cancer evolves. It describes itself as “building the future quietly,” and has almost no public footprint beyond its website.

Finally, there is Capable, who are working on what might be described as Ozempic for sleep, a therapeutic targeting sleep disorders through mechanisms related to the GLP-1 pathway that underpins the current generation of weight-loss drugs.

The Fund IV portfolio helps to illustrate a deep truth that might be lost in the survivor bias of looking back on Fund I outcomes; these companies are not obviously going to work. Several are operating in categories where the scientific or commercial case is not yet clear. Some of them will fail. The ones that succeed may well create entirely new categories and markets. This is exactly what should be expected in an early-stage venture capital portfolio at the outset, and if an investor feels like they need more certainty then they may well be in the wrong business.

“This is a game of endurance and optimism.”

Manifest Destiny

The success of Boost VC is evidence that the technologies which will shape the future rarely look obvious at their inception. The most transformative ideas are sitting in a conference room somewhere, being pitched by someone who is being told no by almost everyone they meet, until they find their first believer.

Boost VC built a fund to be that first believer, at scale, across sectors, over time. Their strategy was designed to fill a gap that institutionalised venture capital had abandoned. It turns out the gap was enormous, and that the founders waiting on the other side of it were building some of the most important companies of their time.

The world will produce more founders like Matt Schlicht, who builds obsessively without permission, and more companies like Deepgram and Radiant Nuclear, which seemed too early and too strange until suddenly they were not.

Fund I demonstrated that being the first believer in those founders, unconditionally and at volume, might be the most rational investment strategy in the venture business.

Run your investment firm from your phone with Odin.