The Venture Capitalist's World Model

Venture capital has roots in financing exploration, and in many ways that's what the industry still does today — the horizons are just less literal.

This week we released a directory of research covering venture capital and adjacent fields. Today, the directory features 135 papers that span from the 1980s to 2026, covering market cycles, regulatory changes and systemic shifts in the industry.

Regular readers of The Odin Times will recognise many of these papers from past articles. The directory is part of our goal to take this further, encouraging individuals to examine the literature and use it to feed their own unique and objective model of the world.

There’s a vast and criminally underutilised body of academic research looking at venture capital and the associated disciplines.

This research is valuable, because academics are unlikely to have vested interests and their reasoning and methodologies are transparent. The work is observational, but it is also objective and anchored in reality.

It’s a profound contrast with the output and consumption of private industry, where almost everything is an anecdote built around a narrative. This is the overriding state, whether that’s a result of calculated behaviour or simple self-conditioning.

This preference for short-form insight is mostly the result of processing fluency, where simple ideas travel faster, but two other factors amplify the problem:

Opacity - It’s hard to make a complex argument when the facts are thin.

Insecurity - The desperation for confidence creates an aversion to complexity.

If you were to draw these two factors out as a venn diagram, venture capital would be in the dead centre.

This is why, as an industry, venture capital is uniquely vulnerable to the seductive coherence of simple ideas, rather than complex truths. That’s unfortunate, because venture capital is also uniquely dependent on intellectual diversity, as evident in the damage done by group-think versus the extreme profitability of contrarianism.

This stacks on existing research which illustrates how social media creates echo chambers that amplify consensus ideas while filtering out unconventional or contrarian views — which in turn builds on existing theory that describes how individuals self-censor opinions when they suspect they are in the minority.

“To the individual, not isolating himself is more important than his own judgement. […] This is the point where the individual is vulnerable; this is where social groups can punish him for failing to toe the line.”

Elisabeth Noelle-Neumann, Spiral of Silence (1974)

As the world has become louder and more connected, the outsized power of ideas that can cut through the noise, regardless of their merit, has become more obvious. This wielding of memetic influence is now a field of study that crops up in everything from marketing playbooks to industrial strategy and geopolitics.

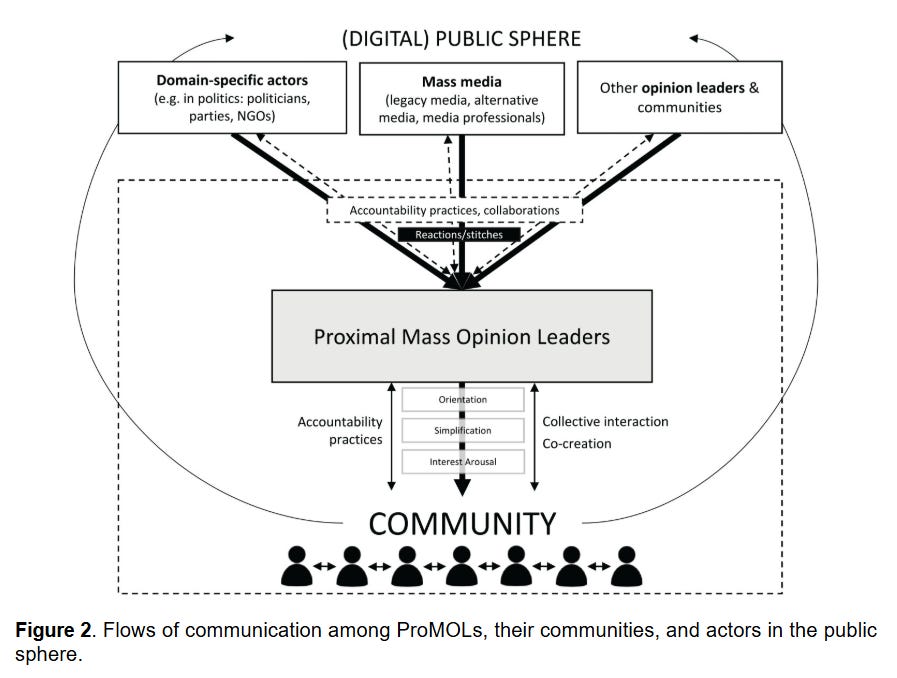

It’s no coincidence that venture capital’s propaganda era began around the same time as a paper discussing the concept of “proximal mass opinion leaders” which essentially sets out the theory behind programmes like a16z’s New Media Fellowship.

More than ever, people are keen to tell you how they see the world; to tell the bigger story. To share their model of the world with you, as if it were a map that you could also follow to success. And, thanks to social media, it’s getting harder to resist.

This is an existential problem for venture capital, which relies on people having the courage and curiosity to build their own uniquely idiosyncratic models of the world. And the courage to hold onto those models in the most difficult conditions.

The Stars Can’t Lie

“Last of all he will be able to see the sun, and not mere reflections of him in the water, but he will see him in his own proper place, and not in another; and he will contemplate him as he is.”

Plato, “Allegory of the Cave” The Republic (380 to 375 BC)

Consider the lesson of early maritime explorers, who are often cited as an allegory for venture capital with many obvious parallels.

Like venture capitalists, they searched for unclaimed territory. The unbounded opportunity of new frontiers. They used maps that approximated the known world and stars as the source of truth which allowed them to navigate beyond it.

These explorers, who made their own maps by necessity, offered a significant advantage for their patrons. For example, from 1488 to 1499, only the Portuguese knew how easy it was to navigate around the Cape of Good Hope. The more widely available maps tended to exaggerate the difficulty of the journey, which deterred others.

The same is true for Russia’s deception about the Siberian longitude in the 1760s, designed to discourage European merchants from using the Northeast Passage. Or Captain Cook’s maps of New Zealand in the 1770s that obscured harbours and safe passage around the islands. Or the Dutch East India Company guarding their knowledge about passage through the Le Maire Strait.

So, maps were also used to deter or mislead, increasing the risk of voyages or discouraging exploration entirely. A precursor to today’s information warfare; the goal was to be seen as an authoritative source while preserving some asymmetric advantage — the ability to exploit a frontier before it became competitive.

So, either you embrace the risk of exploration, following the stars into uncharted waters, or you just go where a map tells you to go — knowing that whoever produced it was, for one reason or another, happy for you to do so.

Simulacra and Simulation

“Today abstraction is no longer that of the map, the double, the mirror, or the concept. Simulation is no longer that of a territory, a referential being, or a substance. It is the generation by models of a real without origin or reality: a hyperreal.”

Jean Baudrillard, Simulacra and Simulation (1981)

Maps, therefore, have power over humanity, by dictating reality to those who don’t know better. In fact, when maps are sufficiently influential, they become our reality.

This is the perspective of French philosopher, Jean Baudrillard.

Imagine a map that showed a canal traversing a peninsula. An arriving ship would be so convinced that the canal must exist, because their course runs through it, that they might end up digging it out themselves. The determination would essentially be that, of the two possibilities, reality was the incorrect party.

The same is true for less literal maps, whether they relate to the hierarchy of ecosystems, the flow of capital, or the focus of attention. A sufficiently authoritative map can organise the world around whatever reality it asserts. And wherever reality is uncomfortably complex or uncertain, people are keen to embrace simple abstractions that offer confidence.

Consider, for example, the fundamental truth of venture capital; there is no formula for success. The biggest winners are rarely the expected winners. There are literally no easy answers in the pursuit of alpha. The industry’s response to this is to manifest an abstract reality of categories, heuristics, and hierarchies around which people and capital can organise themselves. To pretend that there are such things as “obvious winners”, when the term is an oxymoron in the context of investing.

Inside this hyperreality, concepts emerge and embed on the merit of how well they match up with expectations and preferences, rather than any connection to reality. This is fertile ground for memes; simple narrative devices that shape expectations and preferences more easily than a person might alter reality. If you want a boom of enterprise software, sometimes it helps to say there is a boom of enterprise software.

This is evident in the many ideological artifacts of venture capital, most of which have no empirical basis, or are even contrary to empirical findings. These nuggets of common wisdom are not a distillation of reality, but a means by which reality is replaced with something more convenient. Bite-sized and reassuring.

While this was initially the natural response of human psychology, it is increasingly wielded with purpose to shape behaviour and modify outcomes.

It is, effectively, a narrative wargame within a hyperreality of capital allocation.

World Models

“If the organism carries a ‘small-scale model’ of external reality and of its own possible actions within its head, it is able to try out various alternatives, conclude which is the best of them, react to future situations before they arise, utilise the knowledge of past events in dealing with the present and future, and in every way to react in a much fuller, safer, and more competent manner to the emergencies which face it.”

Kenneth Craik, The Nature of Explanation (1943)

The final evolution of the map is the world model; an all-encompassing reflection of reality in which ideas are tested, simulations are run, and complexity is erased. Everyone has a world model, as a reflection of their life experiences and the information they have consumed. But, again, there is danger.

It’s difficult and uncomfortable to try fitting the whole world in your head. To travel widely, to debate, to scrutinise facts and consume data. So, inevitably, our world models are streamlined simulations. Like a video game that lowers the quality of assets when they’re too far in the distance, or around a corner.

Where we lack confidence, we borrow from the models of others. We accept the CNN model of politics, or the Fox News model, whichever fits our priors. We don’t know what to make of AI, so we assimilate Ed Zitron’s scepticism or Brad Gerstner’s optimism. Like a celebrity endorsement of an otherwise lazy world view.

A consequence of this is that building and selling world models becomes a seriously appealing proposition. It is effectively the commercial playbook for 5th Generation Warfare, applied to corporate interests rather than national interests. And, thanks to our base human nature, we are inclined toward the simplest and most affirming option; the GPT-4o of world models. Tell us we’re the good guys, that we’re correct, and that the people we’re secretly jealous of are evil.

For anyone seeking power, learning to pull these levers is obviously attractive. So, like the explorers and their patrons, they create authoritative-seeming world models that serve a hidden agenda, and market them as morally correct, financially lucrative, or more prestigious. These models promise all the benefits of intellectualism, with none of the hard work required, so their users are not inclined to test their validity.

For the venture capitalist, this is death, as characterised by the generation of prestige-seekers that joined the industry during ZIRP. They all adopted variations of the same world model, chased the same opportunities, and experienced the same disbelief and confusion when there was no pot of gold at the end of that rainbow. They did not even have the instinct to reflect on why their approach was doomed from the start.

But venture capital is also where this proposition is most tempting. The long horizons of uncertainty, battling peer pressure and market volatility, are uniquely conducive to insecurity. And what better way to reduce insecurity than to absorb a world model of seemingly successful peers through endless podcasts and posts. The comfort of the herd, and the complete annihilation of alpha.

Ultimately, this may be why emerging managers and outsiders demonstrate aggregate outperformance. They are far enough from the herd to preserve a unique and idiosyncratic model of the world. The kind of model which allows them to recognise the unique and idiosyncratic opportunities which produce outsized returns.

Anchoring in Reality

“What important truth do very few people agree with you on?”

Peter Thiel, Zero to One (2014)

All value that an investor can hope to capture will be a consequence of how they model the world. The ability to recognise potential in a company, which may be little more than a few slides at the present moment, is dependent on their ability to simulate the outcome in their mind.

Like all models, volume of data is one component, but the quality of that data is far more important. And even when you have a large amount of quality data, if it’s not proprietary and differentiated it will leave you stuck on par with everyone else. And par in venture capital is a seriously mediocre place.

So, success requires two things:

First, it requires being in the world, interfacing with reality, literally or figuratively. Collecting data that feeds a world model that is uniquely your own. Absorbing information, whether that’s from visiting a factory, analysing a paper, or reading science fiction to understand the infinite possibilities of the future.

But it’s not the simple act of visiting or reading that produces the benefit. What matters is what is recognised in it, plucked out and mentally filed away, and for each person that will be slightly different. Experiences are not fungible.

Second, it requires epistemic hygiene. In a world where everyone is promoting their own world model, you must carefully protect your own. Like the recursive nightmare of training an LLM on the output of other LLMs, quality will be continually degraded as an investor absorbs the opinions of their peers into their model.

Which is not to say that venture capitalists should avoid interacting with each other, but, as the data shows, the best networks are broad, diverse, and arms-length. Productive collaboration that broadens horizons, not incestuous commingling.

“Remember, your goal in investing isn’t to earn average returns; you want to do better than average. Thus, your thinking has to be better than that of others — both more powerful and at a higher level... You must be more right than others… which by definition means your thinking has to be different.”

Howard Marks, The Most Important Thing (2011)

Indeed, returning to the question posed by Thiel; to hold an important truth which few others agree with, you implicitly have a different view on the world — which will have emerged from a unique body of facts and experiences.

This is why research repeatedly shows that venture capital benefits from greater intellectual diversity, even as the forces within the market drive concentration which pulls more capital behind generic, myopic, corporatised models of the world.

It’s why the ceiling on effective allocation, and therefore human progress, has always been the number of good investors, not the volume of capital; the variety of world models that are being applied to seed opportunity in the most unlikely places.

Against common belief, which favours dull uniformity and credentialism, looking for powerful idiosyncrasy in world models may be how the best venture capitalists operate, and how the most effective allocators identify their potential.

"Worldly wisdom teaches that it is better for reputation to fail conventionally than to succeed unconventionally."

John Maynard Keynes, General Theory (1936)

Watch the latest episode of Going Solo, with Sarah Drinkwater of Common Magic

Run your investment firm from your phone, with Odin