Best Served Cold

Why cold inbound is an overlooked source of alpha, and a research-led approach to getting the most value out of it.

“We found that when it came to success, cold deal flow and warm deal flow deals performed relatively similar in terms of likelihood for success or failure, with warm deal flow companies outperforming in this statistic by a little less than 2%.

However, there was an interesting finding when it came to the size of success. The successful cold deal flow companies outperformed in terms of overall exit size.

Cold deal flow companies saw, on average, a 16.2% higher ROI and required almost 18% less capital.”

Success and ROI of cold deal flow companies versus warm deal flow companies, by Anthony W. Richardson

If you ask a group of VCs to rate the primary sources of dealflow (warm intro from other investors, warm intro from founders, cold outbound, cold inbound), it’s safe to assume that cold inbound would come dead last.

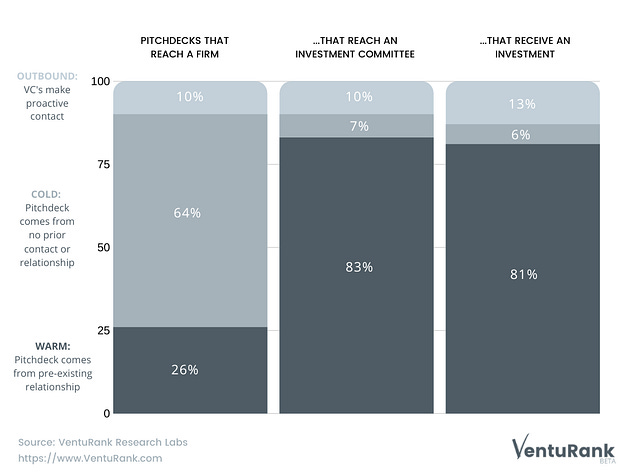

This is reflected in their observed practices; a 2020 survey of VCs in the US found that only around 10% of deals originated from cold inbound, versus 20% referred by other investors and 30% from professional networks and warm intros via founders. Analysis from VentuRank found that cold inbound represented 64% of the opportunities that firms saw, but only 6% of their ultimate investments.

Superficially, it is easy to imagine why. Cold inbound comes with no network signal or peer validation. It is a sign that the founder is not coming from a position of strength, without existing relationships and in-group credibility to lean on. For an industry so heavily influenced by qualitative signals, this feels sub-optimal. The inbox is also just cumbersome to manage, beyond a certain point.

This is precisely why cold inbound is the most potent source of alpha.

Put another way, generating alpha is implicitly difficult. The easier it is to make an investment decision, the less alpha it is likely to generate. Cold inbound has the most friction, takes the most effort, and requires the greatest conviction, thus it yields the strongest outlier returns when it works.

The Unprepared Mind

“In the beginner’s mind there are many possibilities, but in the expert’s mind there are few.”

Shunryu Suzuki, Sōtō Zen monk

It’s certainly effective to build a hypothesis about a particular opportunity and make targeted investments, but most VCs will readily admit that the future is messy. That uncertainty is why the venture strategy exists to begin with.

So, while a “prepared mind” will contribute to great investment decisions, there are limitations. An early-stage investor must be fundamentally open-minded, willing to be surprised, and have a method of origination which exposes them to the totally novel ideas and founders. An unprepared mind, free from bias and full of curiosity, is the optimal lens with which to view these opportunities.

The critical biases in venture capital, mostly related to hindsight and attribution, influence what types of founder and company an investor is likely to look for, as well as what will be referred to them through their network. Cold inbound addresses this with a pipeline of opportunities that are not the product of a selective process, while referred opportunities (including via scout programmes, or junior roles at larger firms) are the product of a black box of third-party biases.

There are two specific vectors for bias in referred opportunities:

The Keynesian Beauty Contest

“We have reached the third degree where we devote our intelligences to anticipating what average opinion expects the average opinion to be. And there are some, I believe, who practise the fourth, fifth and higher degrees.”

The General Theory of Employment, Interest and Money, by John Maynard Keynes

Any investor whose dealflow comes primarily via referrals will face a problem that economist John Maynard Keynes explained with the analogy of a beauty contest.

In his example, the most beautiful contestant was defined as the one who collected the most votes from judges. As a result, each judge is left considering not which is the most beautiful contestant, and not even which contestant other judges will find most beautiful, but which contestant the other judges are likely to think will get the most votes. These layers of abstraction pull focus further away from the central question of beauty, degrading the quality of the judgement.

Through the act of a referral, the view on quality is similarly distorted by the referrer trying to predict how the referral will be received. The desire to be seen to offer high-quality investments leads referrers to prioritise superficial (and often misleading) signals, thus undermining their judgement on quality.

This issue plagues venture investments, generally, as investors become anxious about the enthusiasm of downstream investors. However, the issue is explicit when looking at referred opportunities that introduce another party into selection.

“This suggests that the very act of trying to use the information contained in the decisions made by others makes each person’s decision less responsive to her own information and hence less informative to others.”

Affinity Bias

Everyone has heard venture capital described as a “relationship business”, but relationships are dangerous to any discipline that relies on objective judgement.

This problem is commonly referred to as affinity bias, which reflects our inclination to overweight the opinions of people we feel close to, regardless of their merit. Prioritising the opinions of poorly informed friends over expert strangers.

“The credibility and influence of information will be higher as the relationship between the sender and receiver is close [...] People with whom one has strong ties are regarded as more credible and reliable than people with whom one has weak ties [...] Information derived from strong ties is perceived as more useful and information derived from weak ties is considered less valuable, even questionable.”

Impact of tie strength and experience on the effectiveness of online service recommendations, by Dong-Mo Koo

Affinity bias is reflected in a body of research studying the influence of relationships in venture capital. To summarise the findings, it appears while the breadth of a VC’s network is a positive influence on performance, the depth of those relationships actually degrades performance over time.

“Once we include VC-pair fixed effects into the analysis, we find that higher levels of past coinvestment activity leads to fewer, not more new coinvestments. Moreover, higher levels of past coinvestment lead to lower exit performance, a result that continues to hold after controlling for endogeneity.”

Getting Tired of Your Friends: The Dynamics of Venture Capital Relationships, by Qianqian Du and Thomas F. Hellmann

Essentially, the most beneficial relationships are those that are held at arm’s length, in order to remain objective about any signal that is transferred. Obviously, this is easier said than done given the incestuous nature of venture capital.

Process Alpha

Theoretically, the highest potential venture capitalist is a solo generalist, with no bounds on strategy, stage or category. Like Manfred Macx of Accelerando, they would consume vast amounts of data, distil those insights for opportunity, and identify potential in the most unique and unlikely places.

Unfortunately, that’s not yet possible. Instead, venture investors must build a process that curates their pool of opportunities, rather than trying to boil the ocean. It’s a necessary trade-off, sacrificing an unknown number of outliers in pursuit of a broadly better rate of success.

This gets at the core of the cold inbound challenge. How can investors properly manage the firehose of founders looking for investment?

Logic Gates

“Our job is to find a few intelligent things to do, not to keep up with every damn thing in the world.”

Charlie Munger, former Vice Chairman of Berkshire Hathaway

The first step of this process is for an investor to decide the scope of their inbound.

At the top of the funnel, there’s a question of brand. A firm can position themselves to maximise visibility, becoming a default destination for founders raising capital, or they can target exposure to particular communities and categories. A maximally visible brand will receive a significantly larger volume of applications, most of them poorly fitted, and will need much more active filtration to remain useful. A more targeted brand will see much less, but it will tend to be more relevant.

Then there is the question of explicit filters on stage, sector, geography and ticket size. These are useful, and most firms apply at least two of them, but it is worth being honest about what they cost. Every filter narrows the pool, and an unspecified portion of the most interesting opportunities fall outside of those bounds.

A firm that describes itself as investing in pre-seed rounds for vertical AI will have an easy narrative to pitch LPs, but it will miss many great opportunities that may only be a short step outside that thesis.

On the whole, filters allow a firm to more reliably make good decisions by preserving bandwidth, but they also dampen the upside. The right approach balances these two forces around the competencies of the partners, rather than catering to industry norms or LP expectations.

Judging Books by Their Covers

“The single most powerful pattern I have noticed is that successful people find value in unexpected places, and they do this by thinking about business from first principles instead of formulas.”

The next question is how investors approach screening the opportunities that make it through the filter. The most common shortcut in early-stage investing is pattern-matching on founder credentials (e.g., which schools they attended, which companies they worked at, or past entrepreneurial experience). These data points feel like they should be meaningful, but more often become a vector for dangerous biases rooted in comfortable familiarity or common wisdom.

Venture capital is an outlier business. The returns are produced by a small number of companies that, by definition, cannot be systematically identified. There is no checklist that reliably surfaces a higher-potential founder, and the more an investor leans on that approach, the more they are optimising for the mediocre middle of the distribution.

Markers like a Stanford degree, FAANG pedigree, or simple charisma, are all appealing because they address the insecurity associated with staged capital and the question of downstream investor interest. They help build confidence, pushing up prices without actually being predictive of future success. A Keynesian beauty contest emerges, with the seductive promise of easier markups.

A more literal version of this superficiality is seen in investor’s preference for founders with facial features that match their own. “Mirrored matching” is responsible for a 7% drop in the rate of successful exits, according to one study.

Productive Constraints

“James Montier pointed out in a recent piece that when athletes were asked what went through their minds just before competing in the Beijing Olympics, the response again and again was that the competitor was focused on the process, not on the outcome. The way to maximize outcome is to concentrate on process.”

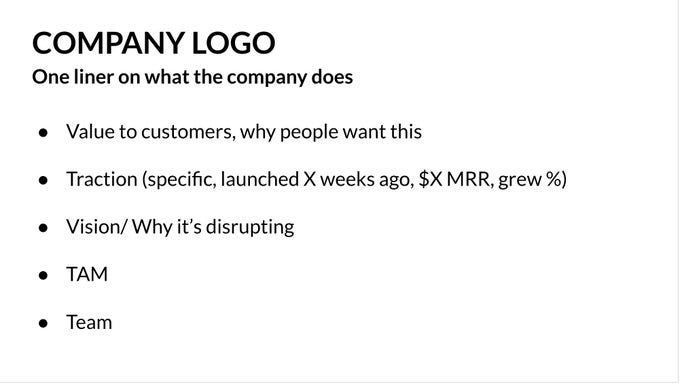

The most instructive precedent is the way that Y Combinator presents batch companies to investors, through their platform. This single-slide format allows investors to efficiently browse through around 250 companies per batch.

Alongside the obvious efficiency gain, this format strips out a great deal of the surface area for biases. The first point of contact isn’t a resume or a discovery call. Investors are focused on the critical elements of what is being built, and are therefore less vulnerable to over-weighting irrelevant similarities. As a result, Y Combinator’s approach has been determined to reduce credentialism and the associated drag on investment performance.

Essentially, the applications that stand out at this stage are those that effectively demonstrate that the founders are designers of a problem worth solving.

This is an example of thoughtful process design, and a great example for any firm that takes the research on biases in venture capital seriously. The objective is to maximise the probability of catching outliers by compressing a pitch down to the critical idiosyncrasies, thus magnifying an investor’s analytical ability.

Staging Information

The practical application of this theory is a staged process that prioritises the most valuable (high signal, low risk of bias) information at each step.

The goal is to present the partner with the most meaningful inputs, ordered by importance, to enable the highest ROI use of time. A maximally efficient and high-fidelity interface between founder and investor.

For an early-stage venture capital firm, the implementation could be as simple as a form, laying out the questions below:

A reasonable first stage asks for the basic information and a hook for ambition.

What is the problem you are working on? This screens for ideas that are obviously bad or in conflict with what the firm has already backed. It also surfaces, in the choice of words, how the founder thinks about scope.

Why do you believe it matters? This is partly a check against the founder’s personal conviction, and partly a chance for the investor to discover something fundamental about the problem itself.

A second stage, for those that pass the first, presses on the qualitative signal in the founder’s relationship to the problem.

What do you believe about it that nobody else does? This is the test for novel insight, and for the kind of problem design described by Bianchi and Verganti. A founder without a compelling position is more likely to be an opportunist, chasing capital.

What is your relationship to the problem? This surfaces the founder’s personal stake in the concept. This is not a hard requirement, but it is one of the better predictors of the persistence, and a more explicit lens on domain expertise.

A third stage, finally, looks at trajectory.

What have you achieved so far? Traction and milestones, articulated honestly. Founders who oversell at this stage are offering useful information of a different kind.

What is the next milestone? Velocity matters as much as the current position, and a founder who can describe concrete near-term goals is providing useful signal on how they think about execution.

The total length of all six answers should be modest, with each subject to a character limit. The goal is to deliver something a partner can read in two or three minutes, with enough signal to know whether to keep going but nothing that introduces material bias. As an added bonus, this structure discriminates against the overly-long AI slop which plagues cold inbound today.

Finally, a firm may choose to take the lesson from Y Combinator a step further, and ask founders to record a short video talking about their company. This would be the final step in the process before a meeting, to get a sense of whether the founder can credibly and fluently articulate their ideas. It also adds a degree of friction to the process which will filter out a large volume of spam submissions.

Undoubtedly, the process will need refinement over time.

Some firms will find they remain swamped, and choose to add more friction.

Others may adjust character limits to make answers more easily digestible, or simply recalibrate their personal hurdle for accepting a meeting.

This ability to learn and iterate is a core strength of a well-designed process, which offers a measurable input and output with dials to adjust.

The Atomic Question

The objective of all of this is to reduce a noisy inbox to a single binary question that a partner can hold in their head while rapidly reviewing potential investments.

Has this team managed to design a problem worth solving?

It’s a simple question, though it encompasses a holistic view of the opportunity.

Submission should be compressed into a form that allows that question to be most easily answered, whereafter the partner may easily move forward with a meeting or swipe it onto the discard pile. Each subsequent stage is a deeper investment of time which should be made on the basis that it has been earned by the previous stages.

This is what process alpha looks like in practice. It’s not about being smarter than the market in some absolute sense, but gaining an edge through exposure to a wider field of potential, stripping out the inputs that distort judgement, and focusing attention on the single most important question.

Cold inbound is no poor man’s deal flow. It is a structurally underpriced source of alpha which rewards the few investors who are willing to take it seriously.

“VC funds must further experiment on the product of VC, building new, more open processes that leverage our industry’s considerable resources to unlock the potential of outsiders and gain access to new markets and new ways of thinking. Funds can start this journey by eliminating warm introduction requirements.”

Launch and run your VC firm from your phone, with Odin

Love this article. Thoughts on cold OUTbound? To me, the best plan is to play offense. Waiting for inbound seems more like defense. If you build a CRM of your investable universe, triage it based thesis fit, investability, etc. and start reaching out to the highest scoring companies, that seems like it would beat both approaches. Would love any thoughts, can reach out to ar@generalinnovation.com if interested in having a conversation.