Nobody's Darlings

Analysing one of venture capital's premiere debut funds: Mucker Capital Fund 1

“We keep our heads down and obsess over how we can help entrepreneurs build great businesses. We are consumed with generating great returns for our limited partners. We are the blue collar VCs that keep showing up every morning to get after it.”

When Erik Rannala and William Hsu opened their small Santa Monica office in 2011, venture capital’s center of gravity sat squarely in the ten-mile strip between Sand Hill Road and South of Market. The serious money lived in the Bay Area, and the serious founders moved there to get it. Los Angeles, for all its technical talent and cultural influence, was an afterthought.

Rannala and Hsu disagreed, and they named their firm after the people who proved that great things come from unglamorous work. Thomas Edison called his laboratory team “muckers” - collaborative inventors who got their hands dirty. That name became a statement about their firm, and the work they intended to do for entrepreneurs.

Their first institutional fund, a roughly $12 million vehicle raised in 2013, would go on to return more than $280 million from a single investment: Honey, the coupon-finding browser extension that PayPal acquired for $4 billion in 2020. That 23x return on the entire fund from one deal placed Mucker among the most successful micro-funds in venture capital history and validated an idea the establishment had been slow to accept: that world-class companies can be built anywhere, if the investors are willing to do the work.

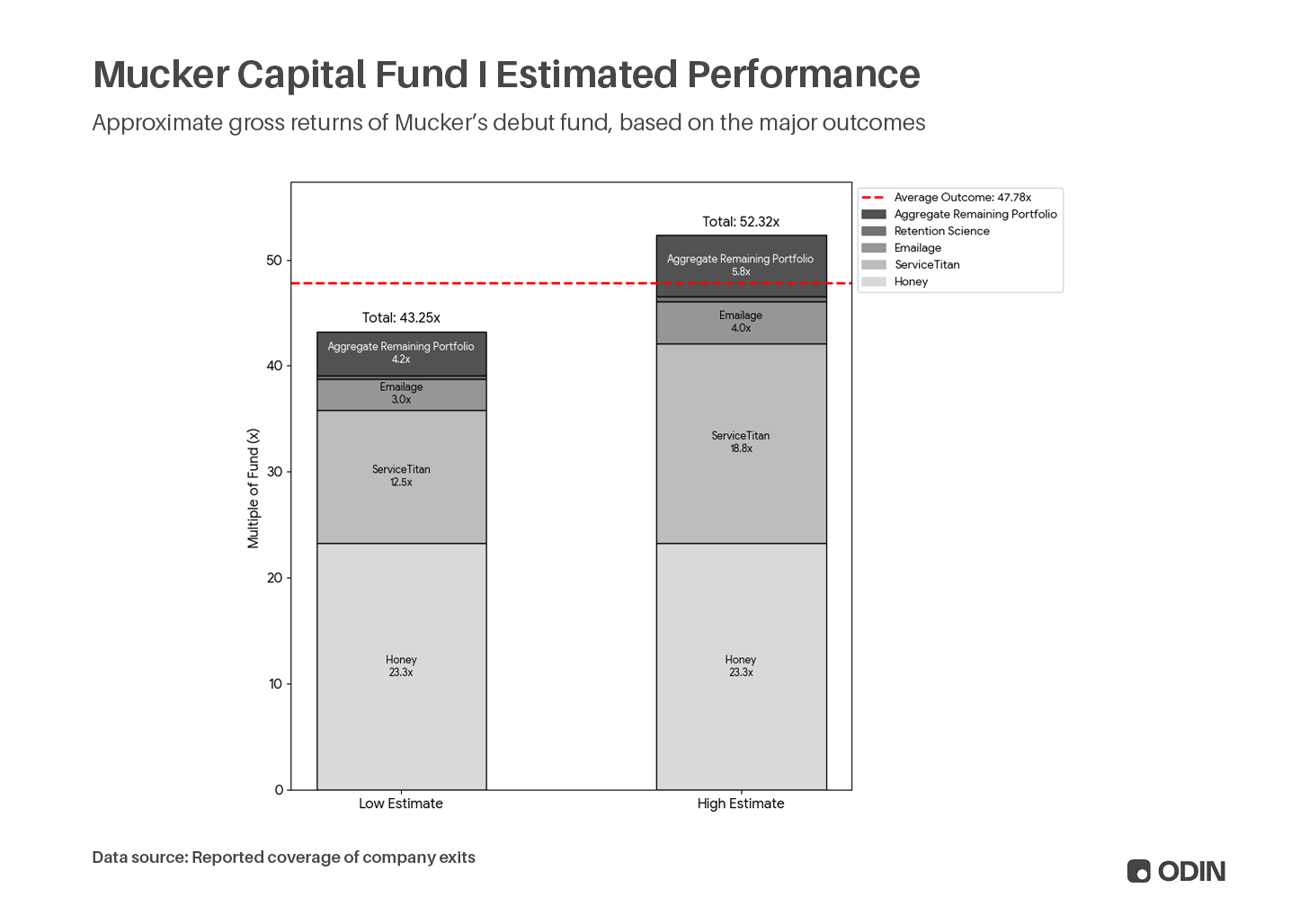

Overall, our napkin math indicates Mucker Fund I returned somewhere between 43 and 53x cash on cash; i.e. at least $3m (net of carry) to an investor from a $100k cheque. This is the rarefied air of the 99.9th percentile.

This is the story of how they built it, and what the results reveal about where alpha actually lives in early-stage venture capital.

The Operators

“When you know that your investors have walked the operating road at a company, and then apply those operating principles of starting a business in their venture fund, it adds a different type of filter. I feel more comfortable taking the advice I get from the team and applying it in real-time.”

William Hsu spent years at eBay and AT&T, building and scaling products inside large organizations where shipping was the only metric that mattered. Erik Rannala worked at TripAdvisor during its high-growth years and later at Harrison Metal, where he studied the mechanics of early-stage investing from the inside. Both had seen how the best companies are actually built: not through decks and term sheets, but through the daily grind of product iteration, customer acquisition, hiring, and firefighting.

They believed a basic asymmetry existed in the market. Southern California had Caltech, UCLA, and USC producing world-class engineers. It had a deep bench of technical talent. And it had a fraction of the venture dollars per capita that the Bay Area commanded. Founders in Los Angeles were building real companies, but the institutional capital wasn’t showing up, or when it did, it demanded they relocate to San Francisco.

Rannala and Hsu saw this as a pricing error. The talent was there, and the ideas were there. What was missing was an investor who would stay local, get involved early, and do the unsexy operational work that helps create strong businesses.

Building the next Mucker Capital? Do it with Odin, your full-stack partner for SPVs and fund administration

The Lab

“In addition to their nose for new opportunities, Erik and Will were capable of being hands-on, operationally oriented investors who could help portfolio companies solve problems, achieve product-market fit, and stimulate growth. This was most apparent in MuckerLab, the firm’s accelerator program for pre-seed opportunities, which it established as a precursor to an institutional fund. In many cases, the companies working with MuckerLab were only a founding team and an idea, relying on Mucker for initial funding, office space, and coaching as the companies worked to build or expand on an early product.”

Before the fund, there was MuckerLab.

Launched in 2011, the accelerator was Mucker’s proof of concept. For $100,000 to $175,000, Mucker took 10 to 15% equity in pre-seed startups and gave them office space in Santa Monica, access to a network of more than 300 mentors and specialists, and something harder to quantify: daily operational coaching from two partners who had actually built products and managed teams. The main objective was to help companies find product-market fit.

There were no pedigree filters, no insistence on Stanford degrees or well-known co-investors. Mucker evaluated founders on the quality of their thinking and the defensibility of their market, not on accolades from the past. In this sense, the accelerator was a deliberate inversion of the Valley model, where pattern-matching on credentials had become a substitute for good judgment.

The accelerator also served as a low-cost laboratory for the partners’ investment thesis. Every cohort generated data on which kinds of founders and markets produced results in Southern California. By the time Rannala and Hsu went out to raise institutional capital, they had something more persuasive than just a pitch deck.

The $12 Million Bet

The first institutional fund began raising in March 2013. It closed at roughly $12 million, with TIFF Investment Management serving as the anchor LP, committing 25% of the total.

At that scale, the economics were not exactly comfortable. The management fee on a $12 million fund does not support a comfortable lifestyle in Los Angeles, let alone two partners. Rannala and Hsu’s livelihoods depended entirely on carry, which meant they depended entirely on returns. For LPs and founders, however, that alignment is a feature rather than a bug.

The strategy was explicit in avoiding exposure to the froth of Silicon Valley. The fund targeted seed and pre-seed companies building defensible internet software and services in undercapitalized ecosystems, Los Angeles first among them. Investments ranged from accelerator checks to Series A rounds. The portfolio would be a few dozen companies, each treated as a long-term partnership, with Mucker providing hands-on support in product development, customer acquisition, business development, recruiting, and fundraising.

It was concentrated, conviction-driven investing in which the partners’ time was the most valuable asset they deployed.

The Sweetest Exit in Venture Capital

“Back in the early days of starting Honey, we needed funding, but what we needed even more was a thought partner to help us really understand and perfect our product-market fit. Mucker provided both the capital and the expertise.”

In December 2015, a company called Honey Science Corporation entered MuckerLab. The product was a browser extension that automatically found and applied coupon codes at online checkout. It was a simple idea in a crowded e-commerce landscape, and it was exactly the kind of opportunity that most funds on Sand Hill Road would have scrolled past.

Mucker became the first institutional investor.

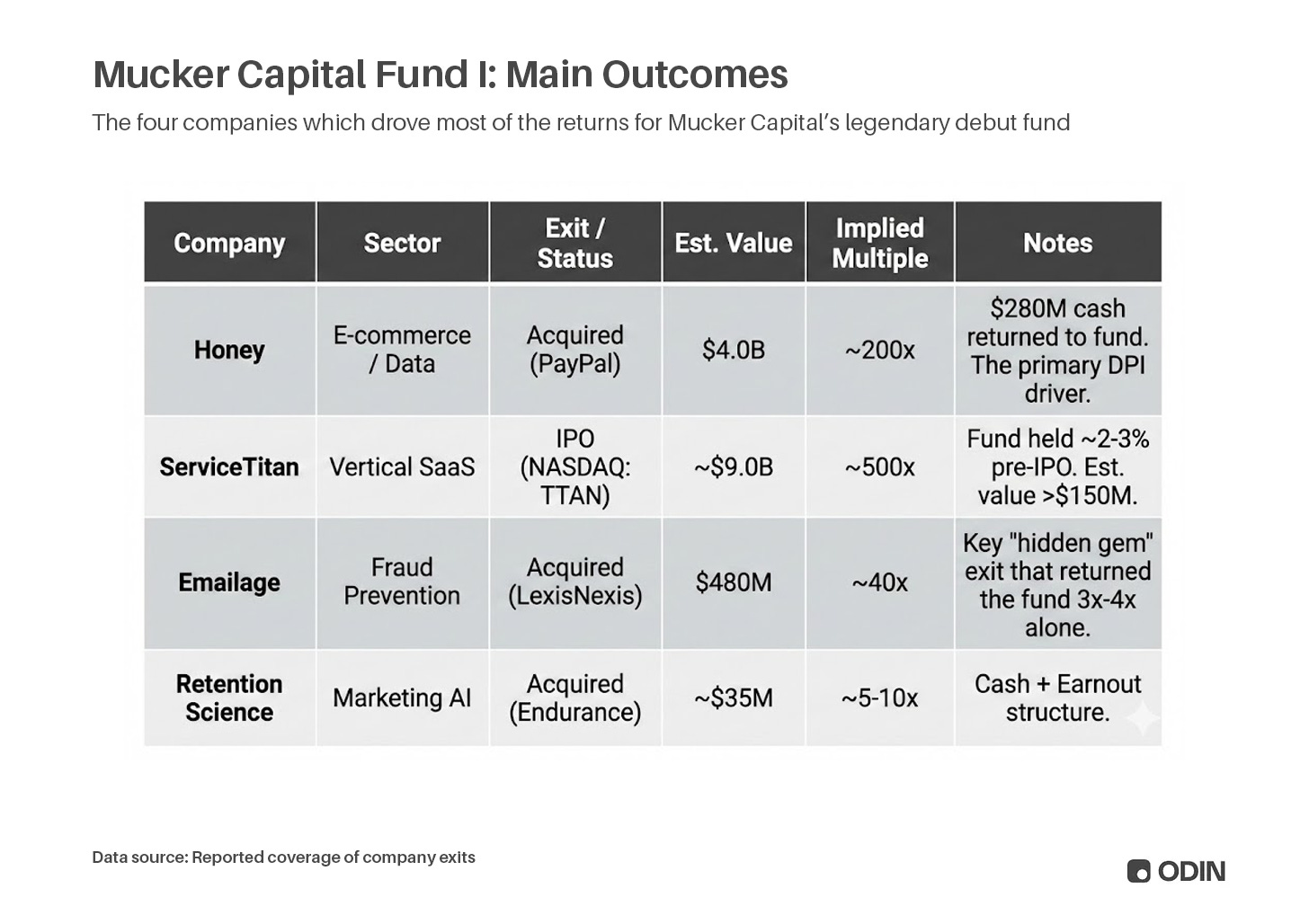

Honey scaled to 17 million monthly active users and roughly $200 million in annual revenue, raising about $49 million in total funding along the way. In January 2020, PayPal acquired the company for $4 billion.

For Mucker Fund I, that single exit returned more than $280 million - 23x the entire fund from one deal. For TIFF, whose look-through exposure to Honey across fund commitments and direct co-investments totalled approximately $1 million, the payout was $60 million; a 60x return on their total investment.

Honey’s outcome did more than generate spectacular numbers. It proved that a two-person firm in Santa Monica, writing small checks into companies the establishment had never heard of, could produce the kind of outlier return that defines a generation of venture capital.

Importantly, it validated the thesis that Rannala and Hsu had been quietly building since 2011: great companies can emerge from non-traditional hubs, and the investors who find them are the ones willing to show up before anyone else does.

Beyond the Headlines

Honey was the blockbuster, but Fund I’s portfolio extended well beyond a single exit. Across Mucker’s early investments, 97% of portfolio companies secured outside follow-on funding, reflecting the accelerator’s ability to turn raw startups into appealing prospects for later-stage investors. The broader roster included consumer, enterprise, and fintech plays that together raised billions in subsequent capital.

ServiceTitan

Founded in 2012, ServiceTitan built business management software for home services companies: plumbers, electricians, HVAC technicians, the trades that keep the physical world running but were still managing their operations on paper and spreadsheets. Mucker invested early. The company achieved unicorn status with a valuation exceeding $9.5 billion and raised billions in funding, becoming one of the defining enterprise SaaS companies to emerge from the Los Angeles ecosystem. In December 2024, ServiceTitan completed its IPO on the NASDAQ under the ticker TTAN, pricing shares at $71 and debuting with a market cap of approximately $8.9 billion.

Emailage

Emailage built fraud prevention technology that used email address metadata and machine learning to assess transactional risk. Mucker was among the early investors. The company raised roughly $55 million before LexisNexis Risk Solutions, a subsidiary of RELX, acquired it for a reported $480 million in early 2020. The deal closed weeks after PayPal’s acquisition of Honey, making the first quarter of 2020 a remarkable period for Mucker’s Fund I.

Retention Science

Retention Science, founded in 2012 in Santa Monica, was an early MuckerLab company that applied machine learning to a problem most e-commerce businesses were ignoring: keeping existing customers rather than spending more to acquire new ones. In April 2020, Retention Science was acquired by Newfold Digital Holdings Group (formerly Endurance International Group), adding it to the roster of Mucker portfolio exits that closed in early 2020 alongside both Honey and Emailage.

Besides the standout successes of Honey, ServiceTitan, Emailage, and Retention Science, Mucker Capital’s Fund I boasted several other notable exits that underscored its early prowess in seed-stage investing. These include Wallaby Financial, acquired by Bankrate in 2015 for its credit card optimization tech; Chromatik, bought by TakeLessons in 2016 to enhance music education platforms; Penango, snapped up by Google in 2014 for secure browsing tools; Blayze, also acquired by Google in 2014 for video coaching software; TaskRabbit, sold to IKEA in 2017 in a deal valued around $100 million; and Surf Air, which went public via SPAC merger in 2023 as Surf Air Mobility, focusing on sustainable aviation.

Taken together, the early funds demonstrated that Mucker’s approach (geographic contrarianism, operational depth, disciplined check sizes) could produce exceptional outcomes across a range of categories.

Compounding the Lesson

Fund I’s performance gave Mucker the credibility to grow without abandoning its model, and their second fund provided further validation. By 2016, the firm raised the $45 million Mucker III, which Hsu considered, with characteristic self-awareness, as similar to a Series A for the firm itself. Later vehicles, including a 2017 vintage, brought total cash raised to more than $150 million by 2023.

“Today, we are inside the tornado. The entrepreneur and venture capital market in LA has hit the hockey stick, and I no longer worry about whether we are going to be around 12 months from now. We’ve shifted our focus to scaling our business, just like a real company.”

The accelerator model has remained the core. The fund size might have grown, but the approach has remained to find founders in undercapitalized markets, get in at the earliest stage, provide real operational support, and let the returns compound over time.

The co-investment structure has also proven durable. Mucker offered LPs preferred terms on follow-on rounds, giving them direct exposure to breakout companies like Honey. This amplified LP returns, mitigated J-curve risk, and built the kind of trust that leads to re-ups in subsequent funds. TIFF’s 60x return on its Honey exposure was a demonstration of how the co-investment model, applied with discipline, can transform a small fund’s economics for everyone involved. It is an actionable solution to the Reserves Paradox.

The Blue-Collar Blueprint

“They returned almost 5x the fund in the form of carry to themselves, which is life changing money for Erik and Will, and yet they are amongst the hardest-working GPs we have”

Michael Kim, founder and Managing Partner of Cendana Capital

Mucker’s story contains a set of lessons for emerging managers that are easy to state, but exceptionally difficult to execute.

An accelerator can serve as a low-cost laboratory for an investment thesis. MuckerLab allowed Rannala and Hsu to build a track record and generate deal flow before raising institutional capital. The accelerator was the proof of concept.

Small fund economics enforce a kind of discipline that larger funds cannot replicate. At $12 million, there is no room for a fee-driven lifestyle. The managers must generate real returns, which concentrates their attention on the only thing that matters: finding alpha.

Geography can be an edge. Mucker’s focus on Los Angeles was contrarian in 2011. It meant less competition for deals, lower entry prices, and access to a founder pool that mainstream VCs were ignoring. The bet has since been vindicated as LA emerged as one of the country’s most productive startup ecosystems.

Operational expertise can be a moat. Rannala and Hsu did not offer portfolio companies vague “value-add.” They sat in the room and helped build products, acquire customers, recruit engineers, and prepare fundraising materials. That hands-on work is why 97% of Mucker’s portfolio companies went on to raise further outside capital.

The relationship between GP and LP is itself an investment. The co-investment structure, the alignment through small fund size, the willingness to let performance speak for itself. These are not incidental features of Mucker’s model.

The Magic of “Mucking In”

Thomas Edison did not invent the light bulb alone. He built a team of muckers, people who worked in the laboratory alongside him, testing filaments and wiring circuits, doing the unglamorous daily work that turned ideas into products.

Erik Rannala and William Hsu chose the name deliberately, because they were not trying to get ahead by being the smartest investors on Sand Hill Road. They were trying to be the most useful investors in a market that the “smart money” had overlooked. They started with an accelerator in Santa Monica, raised $12 million from investors who believed in alignment over scale, and built a portfolio that returned 23x from a single deal while producing unicorns, IPOs, and dozens of successful exits across the rest.

The thesis was never complicated. Find the founders. Do the work. Stay close. Let the returns take care of themselves.

And it worked. Oh boy, did it work.

Build the next Mucker Capital with Odin

Great piece Dan!