The Disappearance of the Ten-Year Fund

Breaking down recent research on venture capital fund horizons, and the implications for small and emerging managers.

The standard venture capital fund, as taught in business schools and outlined in thousands of LPAs, runs for ten years. Capital is called over the first three to five, deployed into a portfolio of young companies, and harvested through the back half of the decade as those companies are sold or taken public. Limited partners receive their money back, with whatever returns the general partner has managed to engineer, and the fund is wound down.

That is the textbook version of venture capital, but it doesn’t really exist today.

In April 2026, Robert Bartlett and Paolo Ramella of Stanford Law School, released a paper examining the influence of extended liquidity horizons in venture capital. “The Disappearance of the Ten-Year Fund” draws on linked quarterly cash flow, NAV, and portfolio company data from PitchBook covering funds formed between 1995 and 2014.

Their finding is that the ten-year horizon (which supposedly anchors fund accounting, performance reporting, fundraising cycles, and LP expectations) no longer corresponds to anything in the underlying economics of venture market.

“Unrealized NAV late in fund life has risen sharply across vintages, especially in venture capital, and many funds continue distributing capital for more than twenty years.”

The Disappearance of the Ten-Year Fund, by Robert Bartlett and Paolo Ramella

For the 2010 to 2014 vintage, the median venture capital fund still reports year-ten NAV that exceeds total committed capital. Such a significant share of fund value sits unrealised when, in theory, the vehicle should be winding down.

Bartlett and Ramella observe that fund lengthening is not because modern funds are converting NAV into cash more slowly than their predecessors; the speed of distributions after a liquidity event hasn’t changed significantly. Portfolio companies are simply staying private longer, and getting much larger.

“Elevated late-life NAV primarily reflects greater value creation: these funds hold portfolio companies that reach substantially larger valuations by year ten and exhibit more extreme right-tail outcomes.”

The influence of extended liquidity horizons on venture capital performance is obviously negative, from a time-value perspective. If a sizeable amount of value remains unrealised in year ten, interim IRR must blend actual distributions with estimated valuations. Those metrics drift downward as the liquidity horizon stretches further, unless the unrealised portion appreciates exceptionally quickly.

This downward drift is systematic, larger in venture capital than private equity, and increasingly pronounced in the most recent vintages where late-life NAV is the most inflated.

“Investors evaluating managers, especially in VC, should expect greater IRR-unwinding when a large share of value remains in NAV, even when interim IRRs appear strong […] These findings challenge the use of ten-year fund structures and interim performance metrics as reliable guides to the timing, risk, and performance of private fund investments.”

So, if the ten-year structure is functionally dead, why does the industry keep using it?

Parkinson’s Law

Industry practitioners have been quietly aware of the lengthening for years. In some ways it is a parallel to Parkinson’s Law:

“Work expands so as to fill the time available for its completion.”

In a venture capital context, that might be reframed as:

“Funds expand so as to absorb the capital available for management.”

This is a reflection of the goal shifting from the fiduciary relationship of delivering the best possible performance, to a service relationship of managing capital at scale for a larger community of LPs who needed a place to park it that was labelled “venture capital”.

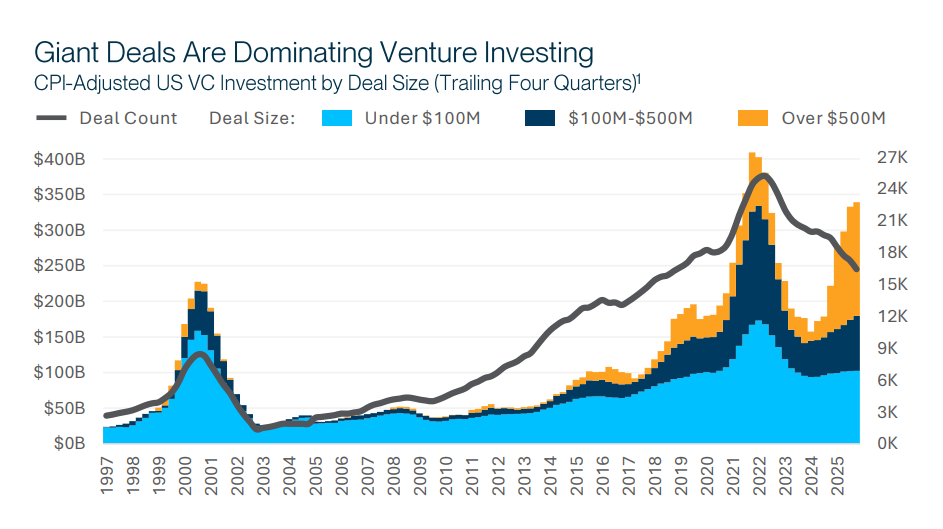

As a result, SVB’s State of the Markets H1 2026 report describes a venture market that has split into two largely separate industries, operating out of one allocation bucket. At one end are the massive growth rounds dominated by mega-funds; at the other, a shrinking cohort of disciplined early-stage investors. In 2025, 33% of all US venture dollars flowed to the top 1% of companies by valuation, up from 12% in 2022. The mega-fund segment, with deals over $500 million, captured a far larger share of total investment than at the 2021 peak.

Inside this distorted market, fund extensions are just a fact of life for LPs. Top-quartile funds routinely take sixteen to twenty years to fully return capital. A growing share of 2010 to 2015 vintage funds remain active, with material NAV still on their books.

The traditional harvest phase has been replaced by an extended growth phase, creating space for larger pools of downstream capital from larger funds. Companies in modern portfolios continue to scale, often dramatically, well after the ten-year mark.

So the argument is not that capital is stuck and entirely unproductive, but that it has enabled investing across timelines that aren’t exactly what LPs signed up for, and that there is a large question mark about the resulting performance.

Paper Tigers

If the ten-year structure has lost its connection to the reality of venture capital, why has it not been replaced? The answer is that it serves several functions that have nothing to do with actual fund outcomes.

LPs compare funds by vintage year and use these reference points to make portfolio construction decisions. Cash-flow models for pensions, endowments, and sovereign wealth funds are built around predictable distribution schedules. So, even when the underlying funds routinely blow through those schedules, the schedules provide an illusion of standardisation that enables comparison.

A ten-year fund is intelligible to a board, to a trustee, to anyone who must explain the asset class to people who aren’t familiar with it. An indefinite-horizon vehicle feels much less certain and therefore is harder to defend, even if it is closer to the truth. The industry has continued to write ten-year LPAs partly because change is uncomfortable, and invites too many other difficult questions.

Successor funds are typically raised three to four years after a predecessor closes, on the implicit understanding that the predecessor will be approaching early distributions by the time the new vehicle is investing. However, when predecessor funds carry large unrealised NAV positions for years past their stated end date, there’s an awkward overlap. The GP is asking LPs to evaluate them based on interim performance metrics that, as Bartlett and Ramella demonstrate, are mechanically inflated by exactly these unrealised positions.

Normalisation of Deviance

“Normalization of deviance is a term first coined by sociologist Diane Vaughan when reviewing the Challenger disaster. Vaughan noted that the root cause of the Challenger disaster was related to the repeated choice of NASA officials to fly the space shuttle despite a dangerous design flaw with the O-rings. Vaughan describes this phenomenon as occurring when people within an organization become so insensitive to deviant practice that it no longer feels wrong. Insensitivity occurs insidiously and sometimes over years because disaster does not happen until other critical factors line up.”

When Doing Wrong Feels So Right: Normalization of Deviance, by Mary R Price and Teresa C Williams

For all that maintaining this comfortable status quo suits the managers who profit most from it, there are costs involved.

For a start, it probably doesn’t set a good precedent that the GP:LP relationship begin with a lie. If neither side expects a ten-year fund, yet both sign a contract explicitly acknowledging that structure, it raises questions about whether other contractual obligations are also perceived as rough guidelines.

The large unrealised positions that persist alongside successor fundraising put strain on the LP model. The GP is simultaneously stewarding old assets and marketing new vehicles, drawing on overlapping resources, reporting on overlapping metrics and benefitting from overlapping fee streams.

Another concern is what could be referred to as the re-risking trap. Mega-funds with billions of dollars in dry powder push companies into ever-larger rounds at ever-higher valuations, betting on power-law outcomes that justify their scale. This pattern keeps risk elevated far longer than the traditional venture curve. A company that might once have reached an early profitable exit at $200 million is now urged toward a Series E round implying a multibillion-dollar outcome, because anything smaller does not move the needle in a $5 billion fund. Smaller managers, who could profitably exit at the lower threshold, get caught in the same long-horizon game even though their fund economics, ownership levels, and investor expectations are entirely different.

Permanent Capital

“Ironically, innovations in venture capital haven’t kept pace with the companies we serve. Our industry is still beholden to a rigid 10-year fund cycle pioneered in the 1970s. As chips shrank and software flew to the cloud, venture capital kept operating on the business equivalent of floppy disks. Once upon a time the 10-year fund cycle made sense. But the assumptions it’s based on no longer hold true, curtailing meaningful relationships prematurely and misaligning companies and their investment partners.”

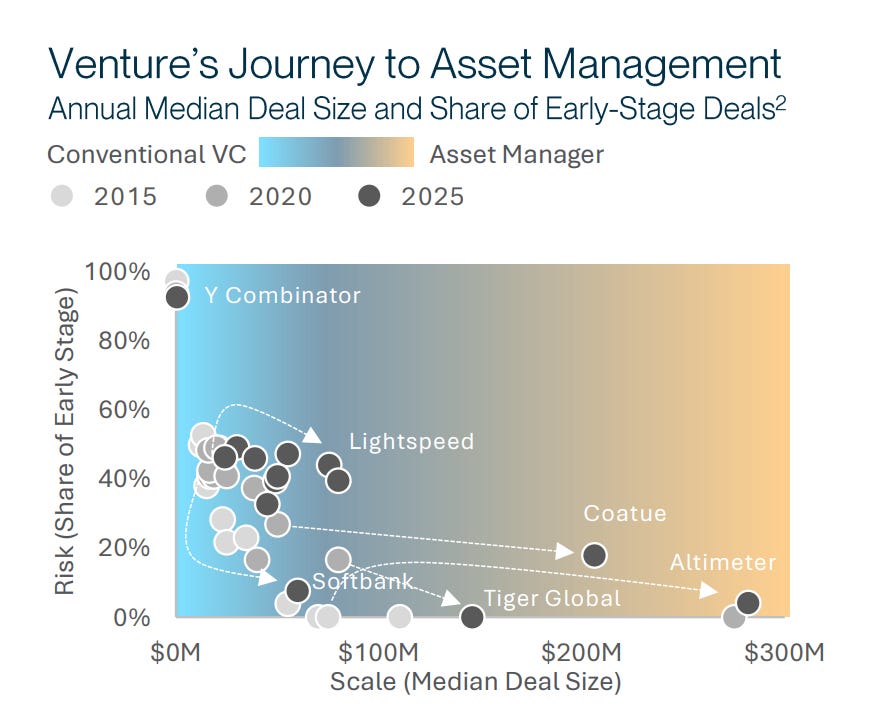

Sequoia’s 2021 restructuring was the most visible acknowledgement that the ten-year fund had become a liability for a firm operating at the top of the market. By moving to an open-ended structure, Sequoia could hold post-IPO positions indefinitely, fund new investments through internal recycling rather than periodic LP commitments, and offer LPs semi-annual redemption rights instead of fixed distributions. The model, which resembles a hedge fund grafted onto a venture franchise, was made possible because Sequoia’s track record allowed the firm to do something novel without spooking LPs.

Other large firms have moved in similar directions. Andreessen Horowitz and General Catalyst registered as investment advisers, expanding their flexibility to hold public securities and pursue non-traditional asset classes. The architecture of the mega-firm has, in practical terms, abandoned the ten-year horizon. What remains in the LPAs is a vestigial structure, preserved out of convention and regulatory familiarity.

The largest investors that entered the venture asset class in size during the 2015 to 2022 boom were sovereign wealth funds, pension allocations, family office platforms, and crossover funds that operate on indefinite or very long horizons. That capital has flowed into mega-funds, which deploy it into very large rounds at very high valuations. Companies that receive that capital have less reason to go public and more capacity to scale privately. The ten-year framework, designed for an era of smaller funds and faster exits, was left supporting a market that had outgrown it.

The logical response for firms operating at this scale is Sequoia’s; permanent capital, open-ended structures, and indefinite horizons match the underlying economics of holding the top of the power law for as long as it continues compounding.

Nimble Capital

The same logic does not apply for small funds, where the analysis breaks in the opposite direction and the disciplined ten-year fund may be favourable.

This is partly a story about the law of large numbers and partly a story about ownership. A small fund concentrating its capital in early rounds at modest valuations can convert a single outsized exit into a fund-returning event where a large fund cannot. To move the needle on a $1 billion fund, a manager needs $3 billion or more in realised value, which requires either many large outcomes or one truly enormous one. The mathematics push large funds toward the re-risking trap and small funds toward the discipline that has historically produced the best venture returns.

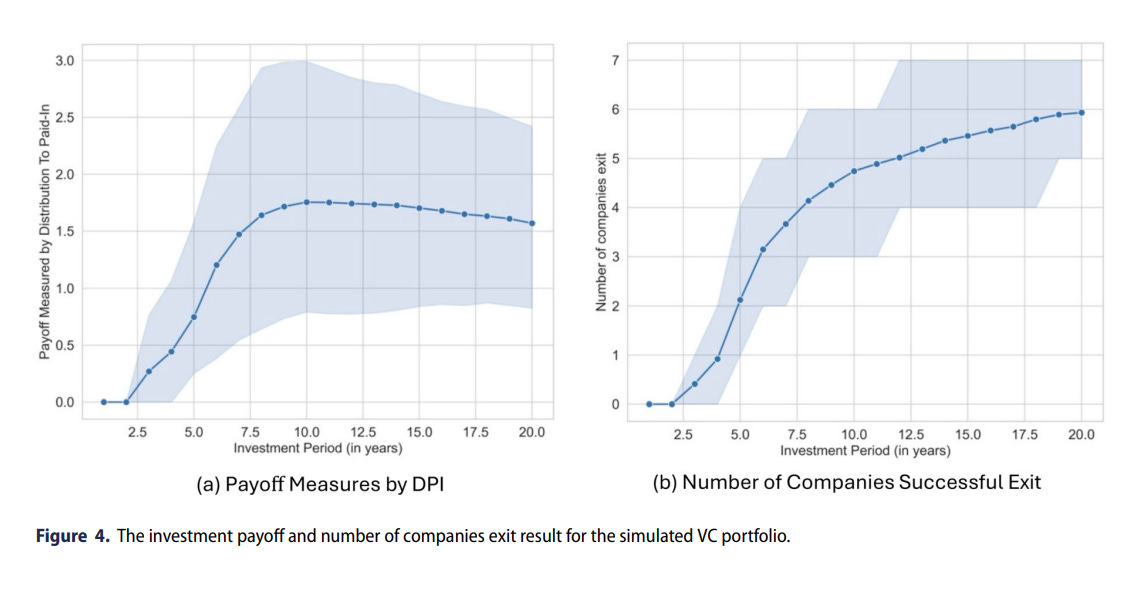

A 2025 paper by Guanrou Deng and colleagues, published in The European Journal of Finance, helps to illustrate this point. Using a sequential investment allocation model calibrated to PitchBook data on US later-stage venture rounds, the authors derive the relationship between portfolio payoff and investment period length. The result is an S-shaped curve.

“The optimal payoff is achieved when the VC fund is terminated around the 10-year period […] Beyond year 10, the curve flattens, and payoffs may even decline, suggesting diminishing returns from holding investments for too long […] Our conclusion that a 10-year investment horizon is optimal for general VC funds remains valid.”

Optimizing investment period length and strategies for later stage venture capital staged financing portfolio, by Guanrou Deng et al.

In their model, years one to four are flat, with portfolios in their early build phase. Years four to ten produce the bulk of payoff growth, as companies mature and successful exits compound. After year ten, the curve flattens and may decline. Holding for longer does not reliably produce additional return, but does mechanically reduce IRR through the time-value drag that Bartlett and Ramella also document.

The peak falls between years eight and ten, which matches the average exit duration for successful venture-backed companies in the PitchBook sample and pre-dotcom IPO trends. For a small fund operating with disciplined portfolio construction and a clear view of when individual positions should be sold, the ten-year horizon appears to be an optimal target.

The Handoff

If small funds are to deliver liquidity within the ten-year window, then the question becomes how to convert paper gains into cash within that time.

One answer to this, in the longer term, is for smaller funds to proactively align companies toward IPO more quickly. This means trading top-line growth of portfolio companies (and spurious markups) for stronger economics, producing companies that are capital efficient and rationally valued, ready for public market scrutiny.

In the shorter term, the answer is the secondary market. Darian Ibrahim’s 2012 paper, in the Vanderbilt Law Review, made the foundational case more than a decade before the current liquidity crunch.

“Secondary markets offer initial investors a new path to liquidity, offer buyers access to a previously untapped class of assets, and produce governance benefits for traded firms. The realization of these benefits in venture capital should lead to a net increase in the total amount of entrepreneurial activity. Given the surplus that entrepreneurial activity produces for society, VC secondary markets should be studied by academics and encouraged by policymakers.”

The New Exit in Venture Capital, by Darian M. Ibrahim

Ibrahim’s observation, drawn from interviews with secondary market participants, was that the direct market for stock in private start-ups was already functioning as a release valve well before the current cycle. Late-stage VCs frequently bought preferred shares from early-stage VCs as part of larger financing rounds. One of his interviewees estimated that 60–70% of late-stage VC financing rounds have a secondary component to them. Early investors could obtain partial liquidity, the company could remain private, and late-stage capital could enter without being constrained by the early-stage fund’s expiry clock.

The elegance of this relationship is that it aligns each participant’s natural horizon with the segment of the company’s life cycle they are best positioned to underwrite. Early-stage funds bring an appetite for idiosyncrasy, qualitative expertise and pricing discipline at the seed and Series A stages. Late-stage funds bring scale capital, quantitative expertise, and the patience to hold through the long pre-IPO window. The secondary transaction at Series C or D is the point where these two parties naturally meet, and both would appear to benefit.

For a small fund operating on a ten-year horizon, the implications are straightforward. Concentrate on early-stage where the pricing edge is real, consider whether or not to reserve capital for companies through Series B, and treat Series C or D as a default decision point for partial or full secondary sales to multi-stage and crossover investors.

Secondaries are no longer the peripheral market that Ibrahim was describing in 2012. Wellington estimates the venture secondary market reached approximately $160 billion in 2025 and is on track to become a mainstream liquidity tool. The conditions Ibrahim anticipated have arrived, although important questions remain about transparency and efficiency.

Collective Conservatism

“We conjecture that venture capitalists and their investors often fall prey to what is known as ‘collective conservatism.’ We investigate this conjecture by analyzing boilerplate provisions in limited partnership agreements. When investors accept suboptimal boilerplate provisions it is not because they believe that the standardized terms and conditions sufficiently align the interests of investors and fund managers, but merely because they think their peers, including their competitors, prefer to include them in the limited partnership agreement.”

Conservatism and Innovation in Venture Capital Contracting, by Joseph A. McCahery and Erik P. M. Vermeulen

The strangest feature of the current venture market is how obviously it has bifurcated while continuing to offer a single standard fund product. Capital has stratified, strategies have stratified, exits have stratified, and the underlying companies have stratified. Fund structures, through sheer inertia, have remained the same on paper despite clearly divergent market realities.

Mostly, this can be explained by the reluctance amongst venture capital firms to present their LPs with novel concepts and risk rejection. Indeed, the way in which venture capital models structures and strategies around LP expectations has clear parallels to “catering” in the GP:founder relationship, likely with the same negative consequences for performance. However, as LPs become increasingly uncomfortable with the market reality, there’s an obvious opportunity for change.

The case made by Bartlett and Ramella is thorough, drawing on data that allows them to trace fund-level outcomes back to individual portfolio company exits. However, their conclusion doesn’t call for the ten-year structure to be abandoned. Instead, they highlight it’s no longer a reliable description of industry practices, and that performance evaluation, fund design, and LP expectations need to be reconsidered accordingly.

Embracing Divergence

What the industry now needs is a divergence in fund products that matches the divergent market reality and LP requirements.

Mega-funds and platform managers with the scale, brand, and track record to demand permanent capital should pursue the path that Sequoia has outlined. The companies they back stay private longer, grow larger, and justify the holding period. Here, the ten-year structure has become a fiction, and the honest response is to move on to more rational arrangements.

Small funds should head in the opposite direction. They should use the ten-year horizon to enforce discipline as a competitive feature that will be appreciated by their community of LPs. A fund that explicitly targets full or majority realisation by year ten, focuses on early stages where it has structural ownership advantages, and uses Series C or D secondary transactions as the default hand-off to larger investors.

The rationale for the small fund’s ten-year revival is the same that Bartlett and Ramella identify for the structural breakdown; modern private markets create more value, more slowly, in fewer companies. That logic supports very long horizons at the top, where the power-law winners are held. It also supports disciplined short horizons in early-stage, where capital efficiency and risk management are most critical.

LPs also face their own pressure to choose a deliberate strategy. Endowments and pensions whose annual payout obligations are growing have begun to question whether the indefinite horizon embedded in mega-fund holdings serves their cash flow needs. A small-fund product designed around genuine liquidity within a decade is an increasingly attractive proposition.

In summary, the ten-year fund disappeared in a period where the venture market was struggling with capital indigestion. Now that is resolved, through the divergence of strategies with clearly differing objectives, there’s an opportunity to bring it back.

Essentially, the opportunity for small and emerging managers may be to finally make good on a promise that venture capital has neglected for well over a decade.

SPVs & Fund Administration purpose-built for global venture capital

Excellent read. Thanks!

the 10-year fund is dead but everyone keeps signing the LPA, classic normalization of deviance