The Individual Versus the Firm

Venture capitalists tend to understand success through the lens of scale, but the pursuit of scale is the undoing of many ventures.

Great companies are usually the product of great individuals. And great companies typically become large companies. But large companies often become ungovernable by the individual.

Too often, and particularly in venture capital, scale treated as a proxy for success. This encourages organisational entropy that erodes leadership and agility.

The counterintuitive conclusion is that deliberate restraint on scale may be necessary to preserve what makes companies great in the first place.

“The transfer of a transaction out of the market into the firm is regularly attended by an impairment of incentives. It is especially severe in circumstances where innovation (and rewards for innovation) are important.”

Oliver Williamson, The Economic Institutions of Capitalism (1985)

Why do people organise themselves into firms?

Economic literature describes the nature of the firm as a compromise; firms are formed to manage external market frictions which prohibit the individual. Marketing costs, trust and reputation, economies of scale, etc.

However, growing firms introduce internal market frictions which limit effective scale.

For example, no individual could have gotten mankind to the moon in 1969; it took an organisation to make that happen. However, the scale of that organisation ultimately led to risk aversion, procedural inertia and rising costs which ground progress to a halt.

Essentially, as organisations expand, their goals and responsibilities become abstracted from the core mission until they are paralysed by hesitant incrementalism.

The optimal configuration, therefore, is where the organisation is always just large enough to remain viable, minimising the dilution of the individual and the mission.

Depending on the goal, that optimal size might be 25,000 people, or it might be one.

“Control loss is cumulative over the levels at which information is sent and the loss eventually imposes a limitation on firm growth.”

Oliver Williamson, Hierarchical Control and Optimum Firm Size (1967)

Uncompromising Vision

“I must create a system, or be enslaved by another man’s. I will not reason & compare: my business is to create.”

William Blake, Jerusalem. The Emanation of the Giant Albion (c. 1804–1820)

The principle of optimal scale can be observed at SpaceX, which has been managed with ruthless focus and efficiency. It has remained a lean organisation, sometimes by necessity but often by choice, prohibiting distractions and eliminating bloat.

That discipline is the result of adhering to the mission of making human life multiplanetary. As a result, Musk knows precisely what to measure; what is important, and what is not. Pursuing that goal has other outputs, like increased cash flows and financial value, but those outputs are never confused with actual progress.

Unfortunately, organisations that lack such clear leadership are inclined to entropy. To scale for the sake of scale; to hire more people, to raise more capital, to acquire more assets. The larger they get, the more distributed responsibility becomes, the more they optimise for easily measurable short-term outputs rather than less tangible long-term goals. Those outputs becomes a crude proxy for progress, until the organisation collapses in on itself.

“A firm will tend to expand until the costs of organizing an extra transaction within the firm are equal to the costs involved in carrying out the transaction in the open market.”

In many cases, scale is the result of financial incentives. Management fees are a topical example, where linear scaling of fees results in inflated funds, which in turn promote mindless scale in the underlying companies. This is a direct conflict with the vision of the founder; accelerating the entropy that threatens to consume their work.

Indeed, it is unfortunately common for financiers to believe that scale itself is the goal, as scale can conveniently be brute-forced with capital in the short-term. These people are responsible for huge value destruction, and should be kept far away from important companies.

The unintuitive truth here is that scale for the sake of scale is something that every leader should resist, even when it appears similar to actual success.

In addition, depending on cyclical market conditions, speed and endurance are often more beneficial than size. Overscaling is easy in ZIRP-like environments where capital is everywhere, and there’s no real punishment for it. Until, suddenly, there is.

In fact, extreme success lowers external market frictions (reduced marketing costs, enhancing reputation) so the optimal size of the organisation actually falls. And a smaller organisation offers efficiency that further strengthens the business.

Great success enables smaller companies, relative to their mission.

Consider a SpaceX hypothetical. If the company was slower, less innovative, with a weaker reputation, they would face greater scepticism from the market. As a result, they would be forced to raise more capital, build larger commercial teams and maybe diversify into other streams of business. This would bloat the organisation, eroding efficiency and the clarity of leadership.

Implicitly, a company cannot just scale into strength. Strength is a product of constraining scale with efficiency; picking an important mission and focusing on it obsessively, scaling only where it enables or accelerates progress.

Undiluted Idiosyncrasy

“The individual has always had to struggle to keep from being overwhelmed by the tribe. If you try it, you will be lonely often, and sometimes frightened. But no price is too high to pay for the privilege of owning yourself.”

Rudyard Kipling, Arthur Gordon interview (1935)

Some professions do not suffer so much from market friction, and so do not benefit from forming larger organisations.

Artists, carpenters, writers, and financial advisors are examples that fall into this camp. The quality of output is obvious or measurable, work is project based, and the relationships are one-on-one which makes monitoring easy. So, the market for these skills operates smoothly and the cost of those transactions is low. There is little upside to scaling the organisation, and the downsides are perhaps even more painful.

This brings us to the question of venture capital, and what value a firm offers to the individual partners.

When it’s working as intended, venture capital is more Philippe Dufour than Hublot. It is artisanal, rather than industrial. The venture capitalist’s role is to apply thoughtful methodology to finding outliers, rather than competing for attention and chasing trends. Consequently, there is little market friction on the demand side.

This would imply that venture investing is best pursued by individual investors or small partnerships. Rather than putting firms on a pedestal for the scale of their operation, more time should be spent celebrating the achievement of individuals. Investors like Cyan Banister, Ron Conway, Oren Zeev, Charlie Songhurst or Elad Gil, who have had an outsized impact on the world. Indeed, these individuals are often the quiet heroes of venture’s success stories, which the larger, later firms usually take credit for.

Why “tier 1” rankings often reward the largest, not the best performing.

However, market frictions remain on the supply side, with fundraising through the notoriously poor GP-LP interface. Research indicates that compensating for this friction is the primary role of the firm in venture capital.

“The results suggest that venture capital partners are often significantly different from each other, but high-quality firms are those with a group of better partners. What then is a VC firm? We suspect that the benefits of joining together may relate to fundraising.”

Is a VC Partnership Greater than the Sum of Its Partners? (2013)

In fact, the paper is specific in finding that there is very little “organisational capital” in venture capital firms. The firm itself basically represents the combined human capital of the partners, including intangible factors like brand and reputation.

So, the desire to raise (more) capital is essentially what drives an otherwise artisanal and unscalable industry to form scaled organisations.

In an ideal world, this would enable fundraising for the best investors without the firm altering their incentives. However, complications emerge in the form of internal market frictions. The partners have joined together into a firm, so they each now must worry about their relative contribution. Or, more accurately, how that contribution is perceived by their peers.

Consider how, as a solo GP, it’s easy to reject a pitch if something turns you off, even if it’s in a hot category. At a large firm, the reputational cost of missing a category winner is high, versus investing in a loser, so you are always inclined to invest.

Similarly, juniors earn their right to make investments by presenting good deals to the other partners. Implicitly, they are trained to recognise what those partners think good looks like, and why, rather than developing any skill of their own.

These internal market frictions encourage consensus seeking, principal-agent conflict, and more bureaucracy and process. The mechanism that makes it easier to raise capital ultimately ends up eroding performance.

Downstream of these internal frictions, larger consensus-seeking firms also incentivise overscaling in portfolio companies, with the harm that causes.

So, in venture capital, the whole is often less than the sum of its parts. Beyond a certain size, the firm is likely to be a significant net negative to the partner.

This probably explains why the rise of the megafund in 2021 has been so quickly followed by an increase in the number of spin-out GPs.

“Talk to a number of solo GPs who left large funds and one reason comes up consistently: they got tired of watching their highest conviction deals die in investment committee because the partnership couldn't get comfortable.

Consensus is good at protecting against obvious mistakes, but really good at killing non-obvious winners. That's a problem.”

Capital Convexity

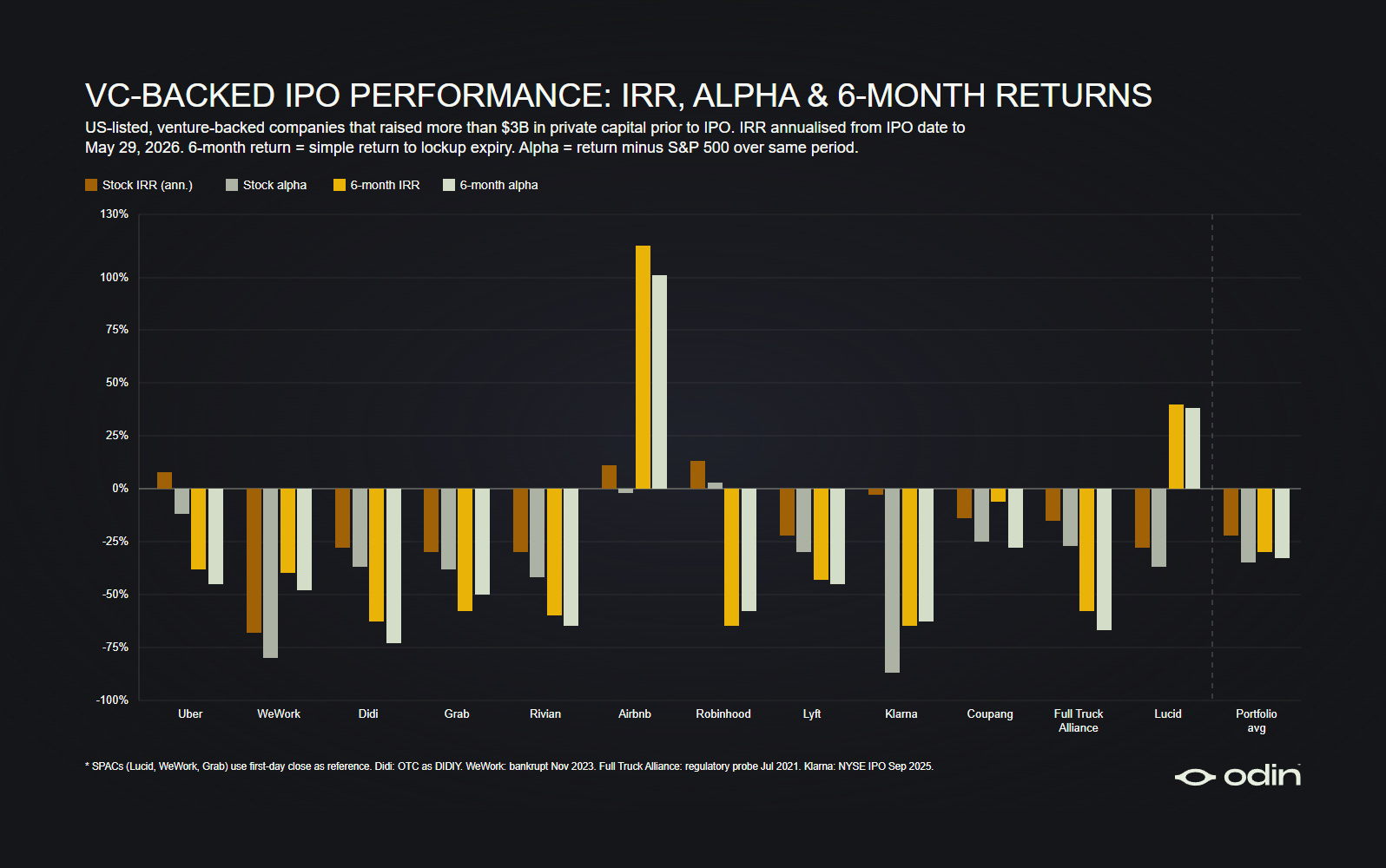

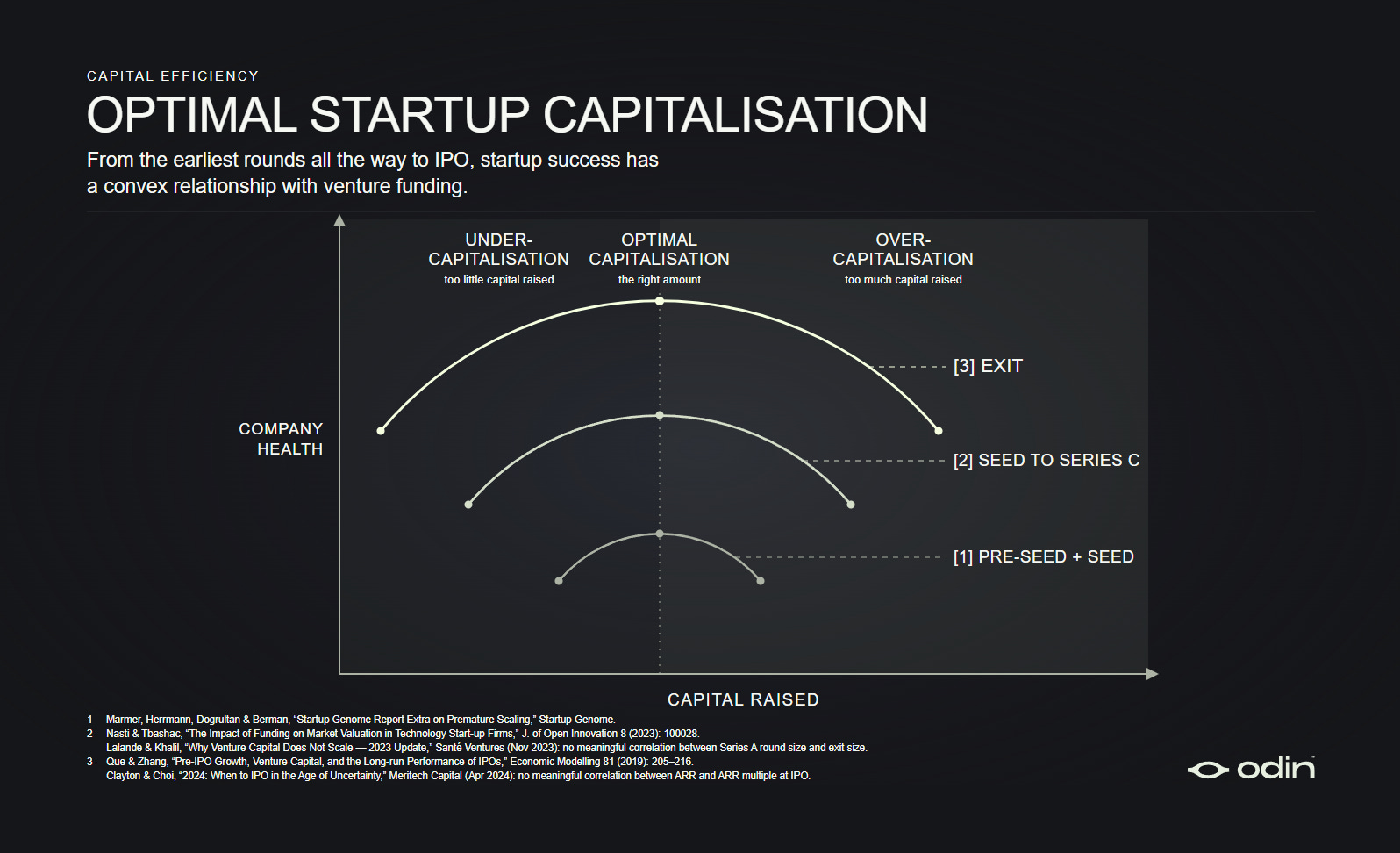

Venture-backed startups exhibit a well-documented convexity in the relationship between capital raised and success. That is, an undercapitalised company will more likely fail, and also so will an overcapitalised company. This is exhibited in data looking at stages from pre-seed up to exit.

The best investments, broadly speaking, are those that are optimally capitalised.

“Premature scaling is a result of firms focusing on one dimension in their operation and advancing it out of sync with the rest of their operation. Our data indicates that inconsistent firms tend to overspend early on customer acquisition, hire too many employees, designate executive management too early, and focus too much on engineering at the expense of customer development.”

Access to capital enables rapid scaling of the organisation, which reduces the external market frictions for small firms, which initially feels good. However, there is the commensurate and stickier increase in internal market frictions which can end up crippling the company at a time when speed and clarity are most critical.

Essentially, raising capital allows companies to defer having to earn their place in the market. Initially this is a worthwhile trade-off, but it quickly becomes dangerous.

This same principle of optimal scale is true for venture capital firms.

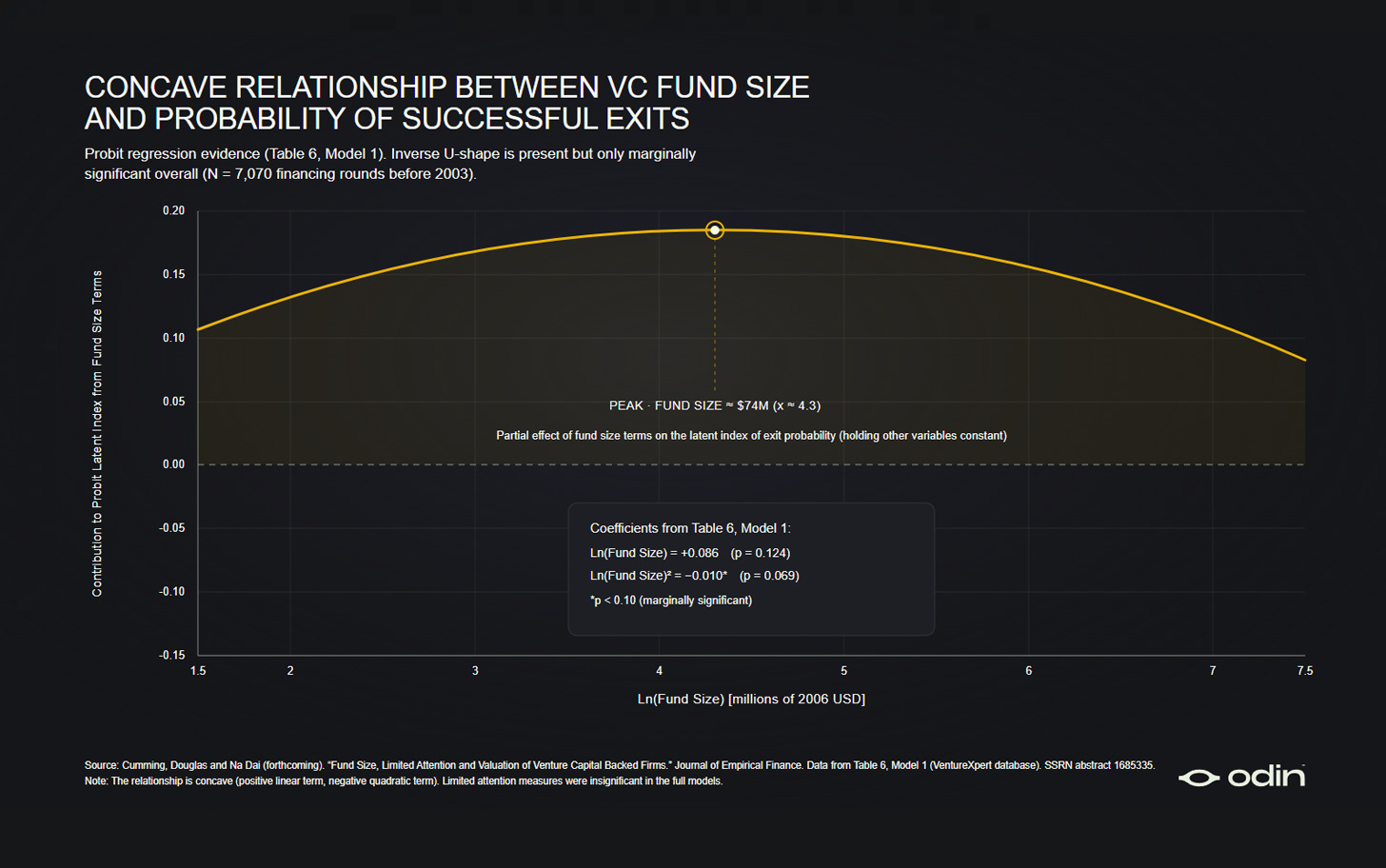

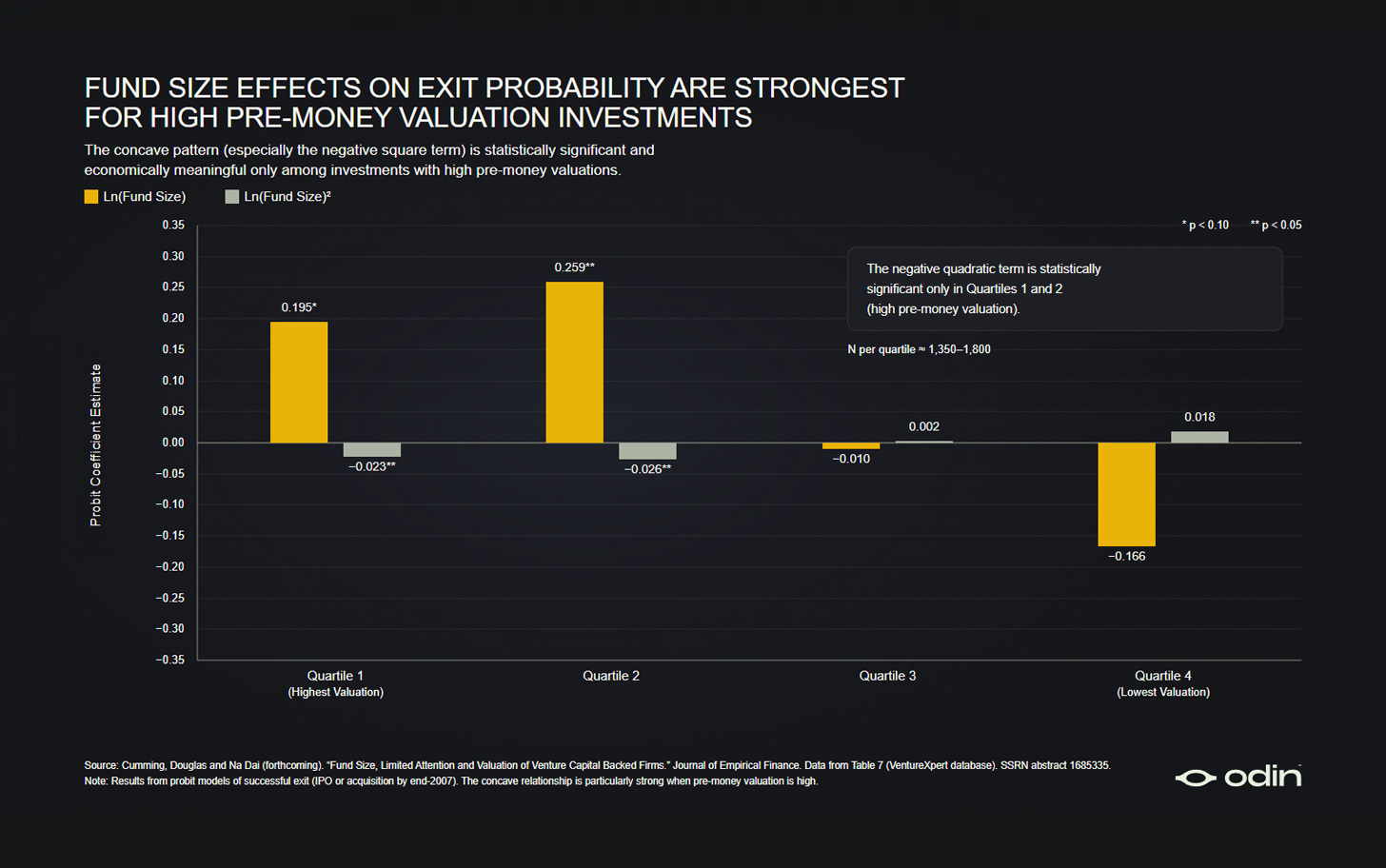

“We show a convex (U-shape) relationship between fund size and firm valuations… we show a concave (inverse U-shape) relationship between fund size and venture’s performance measured as the probability of successful exits… Our findings support the notion that there is diseconomy of scale in the venture capital industry, which is partially due to the constraints from the quality and quantity of human capital when fund size grows.”

Fund Size, Limited Attention, and Valuation of Venture Capital Backed Firms (2010)

Of course, it’s the smallest funds that deliver outlier performance, based on the nature of power law returns. These firms achieve DPI efficiency that is essentially impossible for larger funds, though with a wider spread of potential outcomes.

This potential declines as funds get larger, where returning multiples of the capital is just mathematically more challenging, though outright failure is also less likely.

However, the inverse correlation between performance and fund size isn’t linear, because staged capital creates external market friction across downstream investors. External market friction that, as elsewhere, can be reduced through scale.

However, beyond a certain point, the internal market frictions will outweigh the external market frictions and performance will once again begin to fall.

This reflects the same tension as any other organisation, where if you are focused on the mission (maximising returns for LPs), you should resist the temptation to confuse scale (fund size) with success, as that ultimately degrades your performance.

In theory, a stronger track record will allow the optimal size for the firm and fund size to fall, by reducing the friction around fundraising. This is yet another argument against linear fees that reward scale and structurally erode performance.

“We further show that the negative correlation between fund size square term and the probability of successful exits are particularly strong and significant when the pre-money valuation is high.”

Fund Size, Limited Attention, and Valuation of Venture Capital Backed Firms (2010)

Diseconomies of Growth

“The ‘optimum size’ of the firm is the lowest point of the average cost curve for its given product… [But] if we become interested in other aspects of the firm we ask questions that the ‘theory of the firm’ is not designed to answer.”

Whether it’s venture capital, a startup, or some grand private enterprise, it’s important to emphasise that there is no single optimum size for any organisation. This relates to the writings of Edith Penrose, and the concept of Diseconomies of Growth.

The scale of an organisation should not be interpreted as strength, nor should it be interpreted as weakness. Scale is not inherently good or bad, although mindless pursuit of scale is likely to end badly. The question is always and only whether scale is contributing to the mission, or distracting from it.

A streamlined version of this is the Founder Mode argument, from Paul Graham.

“The theme of Brian's talk was that the conventional wisdom about how to run larger companies is mistaken. As Airbnb grew, well-meaning people advised him that he had to run the company in a certain way for it to scale. Their advice could be optimistically summarized as "hire good people and give them room to do their jobs." He followed this advice and the results were disastrous.”

Paul Graham, Founder Mode (2024)

What Graham overlooks, perhaps for the sake of telling a tighter story, is that the path followed by Chesky wasn’t merely the result of conventional wisdom. It is the predictable entropy faced by any organisation that has scaled beyond its purpose. The result of internal frictions growing beyond their equilibrium with external frictions.

Thus, the Founder Mode principle provides a control for diseconomies of growth, by stating the company should not grow at a rate beyond the founder’s ability to keep a handle on the whole operation. The founder is used as a proxy for mission adherence.

Returning to SpaceX, individuals like Gwynne Shotwell demonstrate it is possible to scale operations beyond the founder’s line of sight, as long as delegates don’t introduce any internal friction. The challenge for any organisation is to design those roles and find those individuals, which itself is a process that cannot easily be scaled.

However, when you extend this logic to venture capital, which is less structured and hierarchical, it’s far more challenging.

Having multiple individuals managing investment decisions across a firm greatly amplifies internal frictions. There are examples of firms like Precursor, First Round, BoxGroup and Benchmark who put remarkable thought and effort into managing this problem, and these are still relatively small firms.

It’s unclear if it’s manageable at all for the largest firms, which may contain dozens of partners. It is more likely that they’re simply pursuing an entirely different objective, where the quality of returns is not their north star. Instead, their goal is to provide a highly-elastic bucket for venture allocation which produces reliable IRR. If this is the case, many of the typical internal market frictions simply no longer apply.

Although it’s worth considering what else venture capital loses with this product; the appetite for outliers and investing in the weird ideas that shape the future.

Run your investment firm from your phone, with Odin