The Magical Money Tree of Management Fees

The mismatch of an unscalable strategy and an incentive to scale.

As the venture market expands, the linear scaling of management fees outpaces the sub-linear scaling of returns from larger and later investments.

As a result, a growing share of the expansion is siphoned out as management fees.

But market expansion also pushes startup exits further into the future. Increasingly delayed exits drive venture capital’s appetite for capital to support larger, later rounds.

So, exits continue to slow, the venture market snowballs, and the fees keep growing.

To begin, consider the hypothetical journey of a successful venture-backed company from a pre-ZIRP era:

In this scenario, a startup is formed around some novel proposition that disrupts a market and promises outsized returns if it works. There’s obviously extreme uncertainty, so raising capital is challenging and dilutive.

After bootstrapping for as long as possible, perhaps raising from angels or friends and family, the founders approach a venture capital firm to lead their Seed round. A syndicate of other investors is assembled, and over the next few years the company is carried through subsequent Series A and B rounds as it continues shedding risk.

For their larger Series C, the company brings in a venture growth firm. This capital helps the company expand into a couple of new markets and build out the required compliance functions to go through an IPO. Their new capital partner understands public market dynamics, and acts as a steward in that journey.

In year 8, the company goes public at a valuation of $1.2B. It’s comfortably a fund-returning outcome for the early investors, and a solid multiple on an excellent timescale for growth equity. All within a decade, as designed.

Most importantly, the company has healthy economics and will be well received by public market investors. Access to deeper capital markets helps to fund compounding growth and innovation. Over time, the company may earn access to the major index funds and become a truly generational outcome, especially for those who held onto their shares through the IPO. There is no ceiling on future growth.

However, this scenario only justifies around $10M in total management fees, across all funding rounds and the various firms involved.

In 2010, as the interest-rate crash settled into the market, venture capitalists got a taste of a bright new future. The growth of capital inflows would change the industry forever.

Over the next decade, a new form of venture capital emerged which can be referred to as “selling allocation at scale”.

A common trajectory for successful venture-backed companies in the modern era:

A startup is formed around an innovative proposition that fits some current theme of opportunity, maximising investor appeal. The founders are well credentialled, centrally located in SF, and quickly scouted by a large venture platform.

Rather than the modest Seed round the founders target, the price-insensitive investor cranks it up by a multiple to signal their conviction and discourage competition; they are a “kingmaker”. In return for this generosity, the company promises future growth at an incredible pace.

To hit the required metrics, the substantial balance sheet is used to heavily subsidise unit economics and accelerate growth. Advertising budgets climb, burn rate surges, but all that matters is that revenue keeps accelerating.

Underpinning this is the modern VC’s valuation tool of choice; the revenue multiple. If a fast growing tech startup is valued at 20x revenue, it can spend $1 on winning 50c of revenue and still print $10 of incremental value for every $1 invested.

Downstream of this, startups will fail more often as they prioritise subsidised growth over building stronger economics or creating more value. Failure is compressed into the early years, allowing capital to concentrate faster. The survivors will be those that hit the growth metrics to attract further investment, filtering for companies that are quick to revenue, easy to scale and “legible to capital”, rather than any deeper quality.

As a result, venture platforms have developed a huge appetite for inexpensive early stage “call options”, although they are explicitly looking for scalability and obvious investment appeal over the typical outlier profile of frontier technologies and ideas.

This dynamic solves one problem, while creating another:

On the one hand, it allows the venture platform to show strong incremental metrics to their own investors. Short-term IRR becomes more predictable, and they’ll be known for their investments in the fastest growing companies. This checks all of the boxes for allocators at the largest LPs who optimise for short-term career objectives.

On the other hand, the resulting companies are cash-incinerators and fundamentally incapable of reaching an exit. Their economics are so deeply negative that acquirers won’t want to pick them up (except perhaps a “reverse-acquihire” talent raid), and the transparency required by public markets will only expose their weakness.

However, even here there is opportunity. If you have a fast-growing company that could continue absorbing allocation and printing paper growth, why exit?

If you can raise a $400M fund and earn $8M in fees each year investing in Series A companies, why not raise a $2B fund and earn $40M a year by scaling private companies further and investing in Series E, F and G+ rounds?

So, in subsequent years, the investor makes further investments in the company, putting more capital to work at terms set within that original syndicate. First tens of millions, and then hundreds of millions, at spurious valuations.

While these investments initially come from smaller early-stage funds, later they’ll come from larger growth vehicles. This allows the venture platform to keep allocating to the company from new funds that are within the 10(+2) year fee window. It even allows early investments to be cashed out at a premium in later rounds, if desired.

This behaviour exploits the opacity of private markets, where capital provides the most obvious signal. When it’s difficult to see how well a company is actually doing, investors will look to the behaviour of their peers. This gravitational effect encourages accumulation while destroying alpha and beginning to resemble a Ponzi scheme.

In this modern scenario, a hypothetical company that gets held for 14 years in private markets could easily absorb $1B from venture capitalists across subsequent rounds. This is capital that previously would have been pulled from deeper public markets, where the average fee is closer to 0.5%, rather than 2%.

Horowitz’ Law: “Capital flows to wherever the fees are highest.”

Now, in this scenario this one company provides the basis for an impressive $250M of fee income, rather than $10M from the previous scenario.

So, what about exits?

To the limited extent that exits still matter to the scaled venture platforms, they are somewhat achievable. Take an “exciting” company with hype and revenue at a huge scale and ship it like a meme stock when the market feels amenable. Most of the time, it will sink like a stone at lock-up expiry, but everyone will have celebrated the day-one pop and will lose interest in subsequent months anyway.

The later-stage funds that catch more downside from this behavior may be stapled to the more appealing early-stage funds, so LPs don’t necessarily have a choice but to participate in both. One offers the inflated metrics and occasional liquidity, the other solves for the allocation at scale. It’s a reasonable solution for careerist allocators who don’t plan to stick around to see the rotten fruits of their labour anyway.

It seems intuitive that the companies which experienced the greatest enthusiasm in private markets would continue to be strong performers later in their lives. Unfortunately, this isn’t the case. After all, they are selected on their ability to scale rapidly, not on any deeper quality or sustainable competitive advantage.

Indeed, of the 12 companies that raised more than $3B in private markets, only Robinhood has a (slight) positive return versus the S&P 500 today. Only Lucid and Airbnb were positive at lock-up expiry, though neither are today.

Overall, the returns from this group of venture capital’s giants are miserable. A portfolio based on the theory that raising more $3B+ from venture capital was a positive signal would be sitting at –117% today relative to the index.

This outcome is aligned with a large body of research on the interface between venture capital and public markets. Venture-funded growth, beyond a certain point, becomes a major negative indicator for post-IPO prospects. This finding is well grounded in data and financial theory, but the simple explanation is that public markets want strong companies while private markets want big ones.

Despite that, the venture industry keeps growing larger, and pumping more capital into the hottest companies.

In the end, the driver of all of this is that generating fee income is a much better business than generating carry. Scaling allocation is a better business than shaping good exits. Firing money into consensus is a better business than finding outliers.

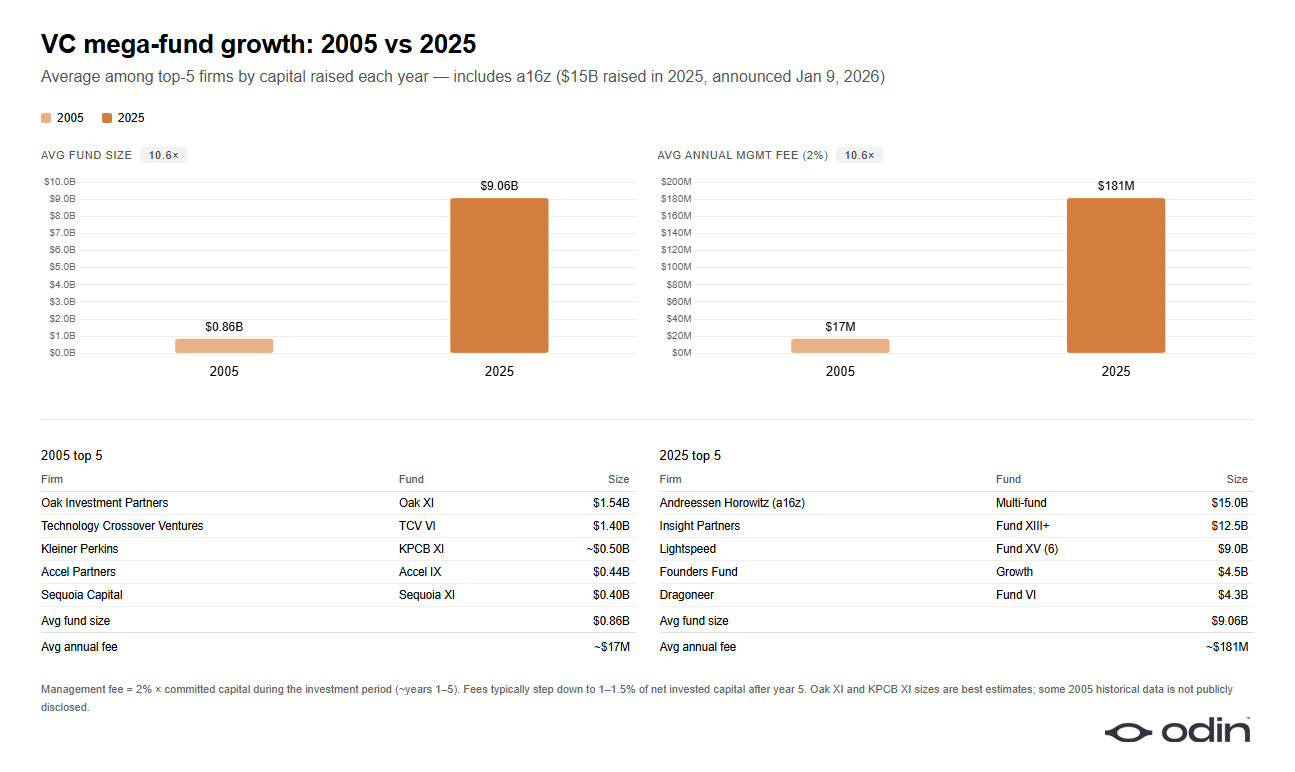

In 2005, the five venture firms that raised the most money in that year each generated around $150M in subsequent fee income. For 2025, it’s closer to $1.6B. Which would you prefer?

A company-level case study of this phenomenon can be found in the example of Rivian versus Tesla. Both consumer EV startups from similar eras, who emerged in different fundraising environments, with investors that had fundamentally different motivations.

Tesla might have had some brief headwinds from the cleantech wave in the early 2000s, but on the whole the company faced a challenging time raising capital. As a result, it raised minimally, found great efficiency, went public relatively quickly, and has gone on to incredible success in the years since.

Rivian was a beneficiary of the low rates environment, and absorbed huge amounts of private capital prior to its IPO in 2021. It never felt the same capital constraint as Tesla, and had no need to develop the same capital efficiency. This has contributed to Rivian’s struggle and a share price that is now down by more than 80%.

Indeed, Rivian raised $10.5B in private capital prior to IPO, compared to Tesla’s $200M. As a vessel for allocation, it supported a far greater volume of fee payments, despite a clearly weaker outcome.

The development of venture capital as a business of selling allocation, scaling the 2% rather than the 20%, is responsible for a number of unintuitive or seemingly contradictory phenomena in the venture market:

The way in which venture investors have increasingly embraced “consensus” in recent years, seeking to lower fundraising friction instead of generating alpha.

The institutional hostility toward antitrust regulation, despite evidence that antitrust is beneficial for nascent startups, innovation and early-stage returns.

The shift of the venture capitalists’ role from one of monitoring and stewardship, to one of choosing to overlook or even incentivise questionable behaviour.

The invention of functions like platform teams or media arms, designed to support the idea that venture firms have advantages that accrue to scale, which is not reflected in returns.

And the greatest paradox of all, that while the venture capital market has scaled, it has increasingly failed on the two fronts where it should be leading; generating returns for limited partners and driving technological innovation. The era of the greatest abundance, from 2016 to 2021, produced a bonfire of capital in the name of a glut of enterprise software and crypto slop.

Ultimately, this is a failure of LPs who have allowed capital to be assigned to something labelled “venture capital” that is actually just the beta of private market hype cycles. This product is designed to serve the myopic career goals of mercenary capital allocators and the continued bloat of venture platforms.

It has been a radical failure for everybody else. The result is a market with weaker returns that is less tolerant of original ideas. A deadzone for alpha.

A Handful of Companies

The common refrain is that today’s winners are bigger, and the rewards more concentrated into fewer firms, but the evidence is clear that these giant outcomes are not positive in the long run.

The most capacious vessels for venture allocation generally do not continue to grow at a healthy rate after they exit, nor do they continue producing meaningful innovation or other positive externalities.

The screening process which selects for these rapidly scalable companies is crude and unidimensional. It is not well designed for catching the typical outliers which drive attractive venture returns.

The Magnificent 7, which remain the most important companies in the world today, were almost all reared in capital-constrained environments that required relatively early IPOs (a median of 5.9 years). Clearly, this did not limit their future growth. In fact, those constraints helped forge truly durable, powerful businesses.

Where would AI be today without foundational work done by Google, the hardware provided by NVIDIA, and the cloud infrastructure from Google, Amazon and Microsoft?

Indeed, private markets are feasting on the gains of investments made decades ago, while failing to consider what the next crop ought to look like.

What future progress is being sacrificed to the goal of turning venture capital into a game of flipping jacked-up companies onto public markets?

Odin: SPVs & Fund Administration for truly adventurous capital