The Sick Man of Private Markets

Private equity was forced to get fit after the Global Financial Crisis. Venture capital's megafunds would benefit from a similar intervention.

In The Disappearance of the Ten-Year Fund, we looked at how little the structure of venture capital has changed since the 1940s.

In The Magical Money Tree of Management Fees, we looked at how scaling capital without modifying incentives has produced a stagnant agglomeration business.

Today, we look at the endgame; what happens when LPs decide they have had enough of misalignment and underperformance, using the example of private equity which went through a similar process in the post-GFC period.

The Intervention

“Limited partners are more and more convinced that they have mistakenly believed that the boilerplate ‘two and twenty’ rule ensures a proper alignment of interest and incentives.”

Recasting Private Equity Funds after the Financial Crisis: The End of ‘Two and Twenty’ and the Emergence of Co-Investment and Separate Account Arrangements (2013)

In the aftermath of the Global Financial Crisis, the private equity industry faced a growing lack of confidence from its own investors.

As every other market crashed, PE holdings were held at relatively high marks and opportunities to sell disappeared. So, the denominator shifted, making PE an uncomfortably large and increasingly risky share of LP exposure.

The LPs, who were concerned by the lack of distributions and the misalignment of PE managers, began to put pressure on the industry to improve its product.

Gradually, the industry relented. Managers embraced better practices through the adoption of ILPA principles, economics began to improve, and a healthier balance in the LP-GP relationship was found.

There is much to be learned from this example.

There were two main areas of change: fund economics and co-investment rights.

Fund Economics

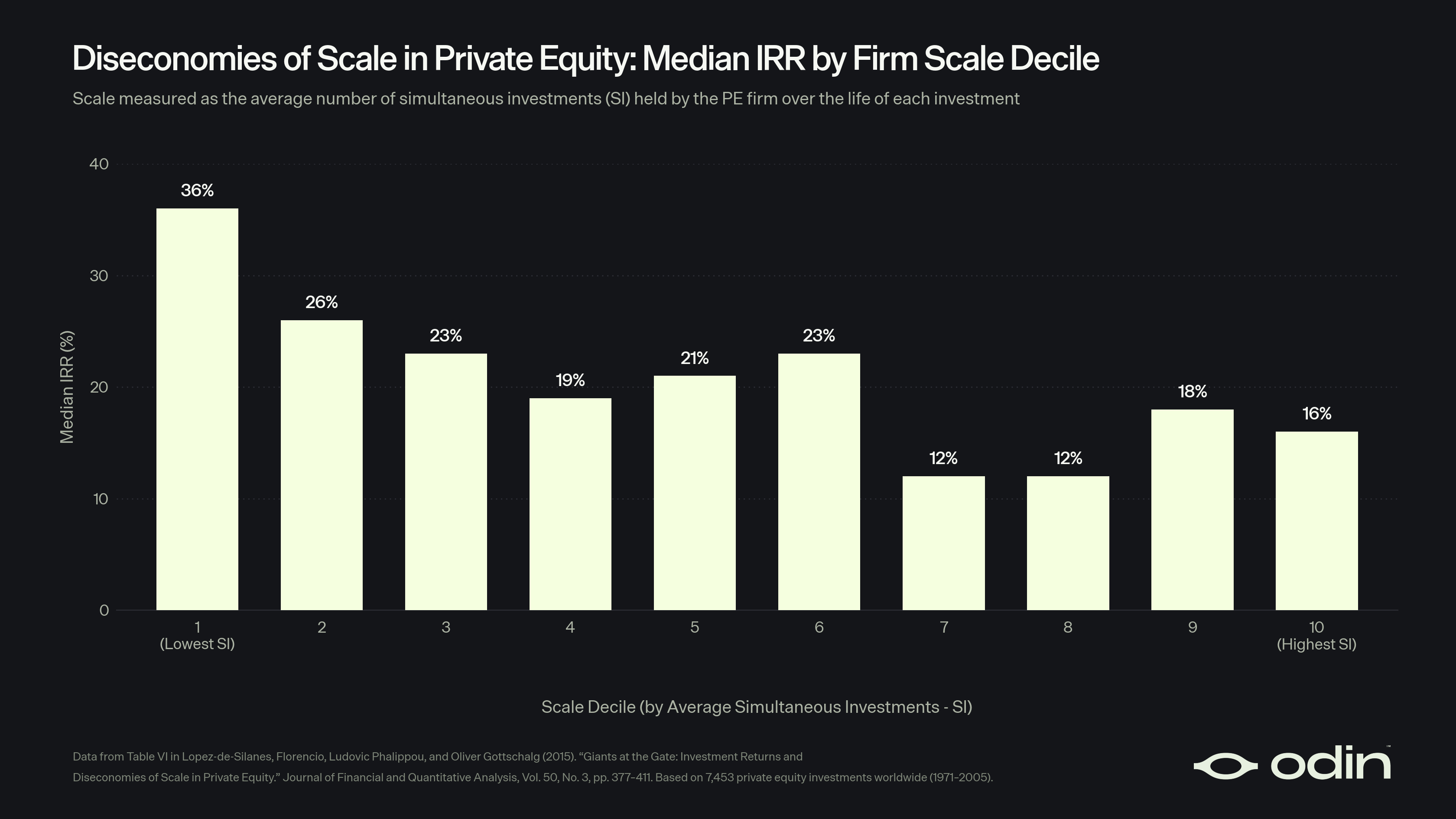

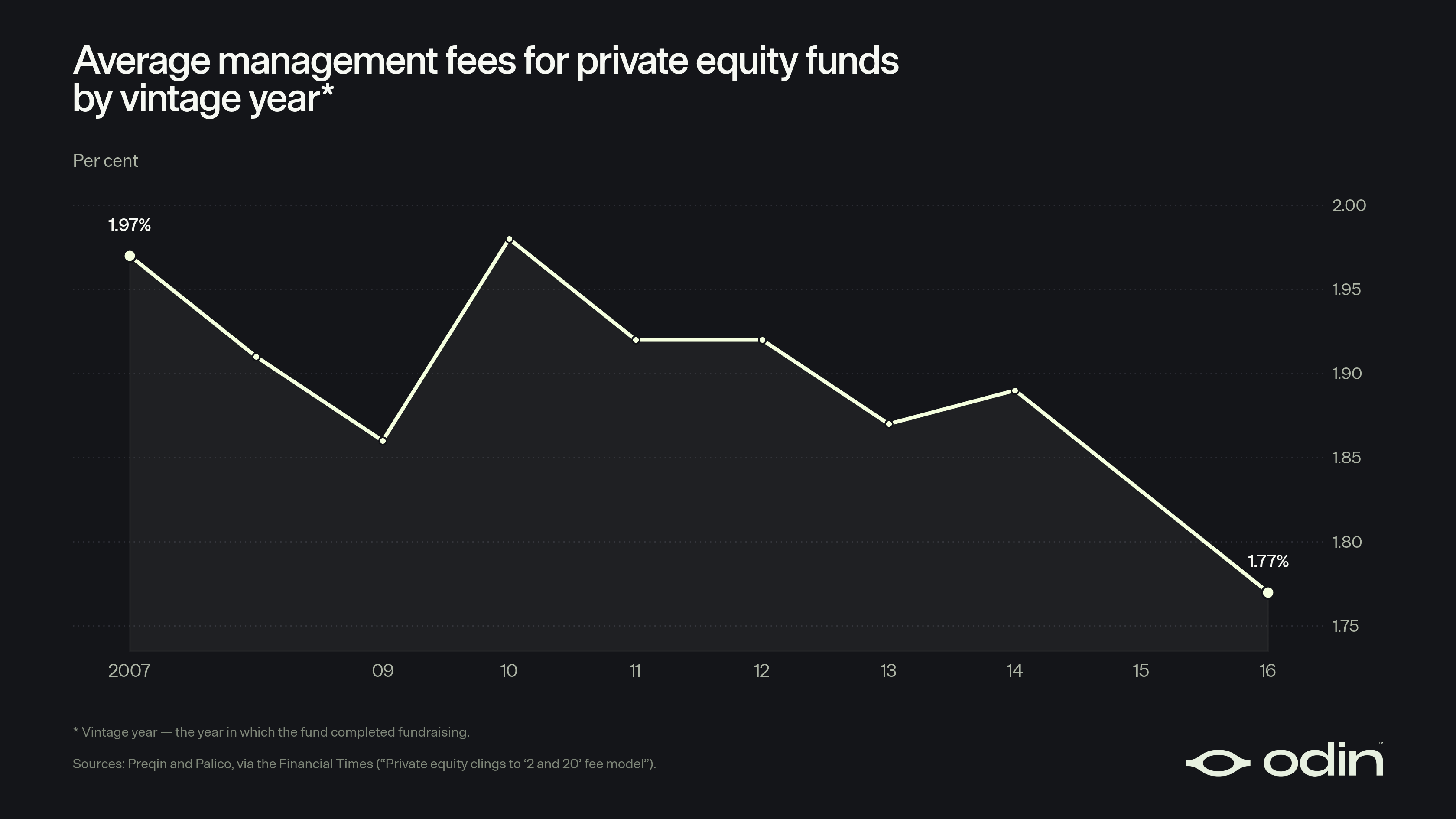

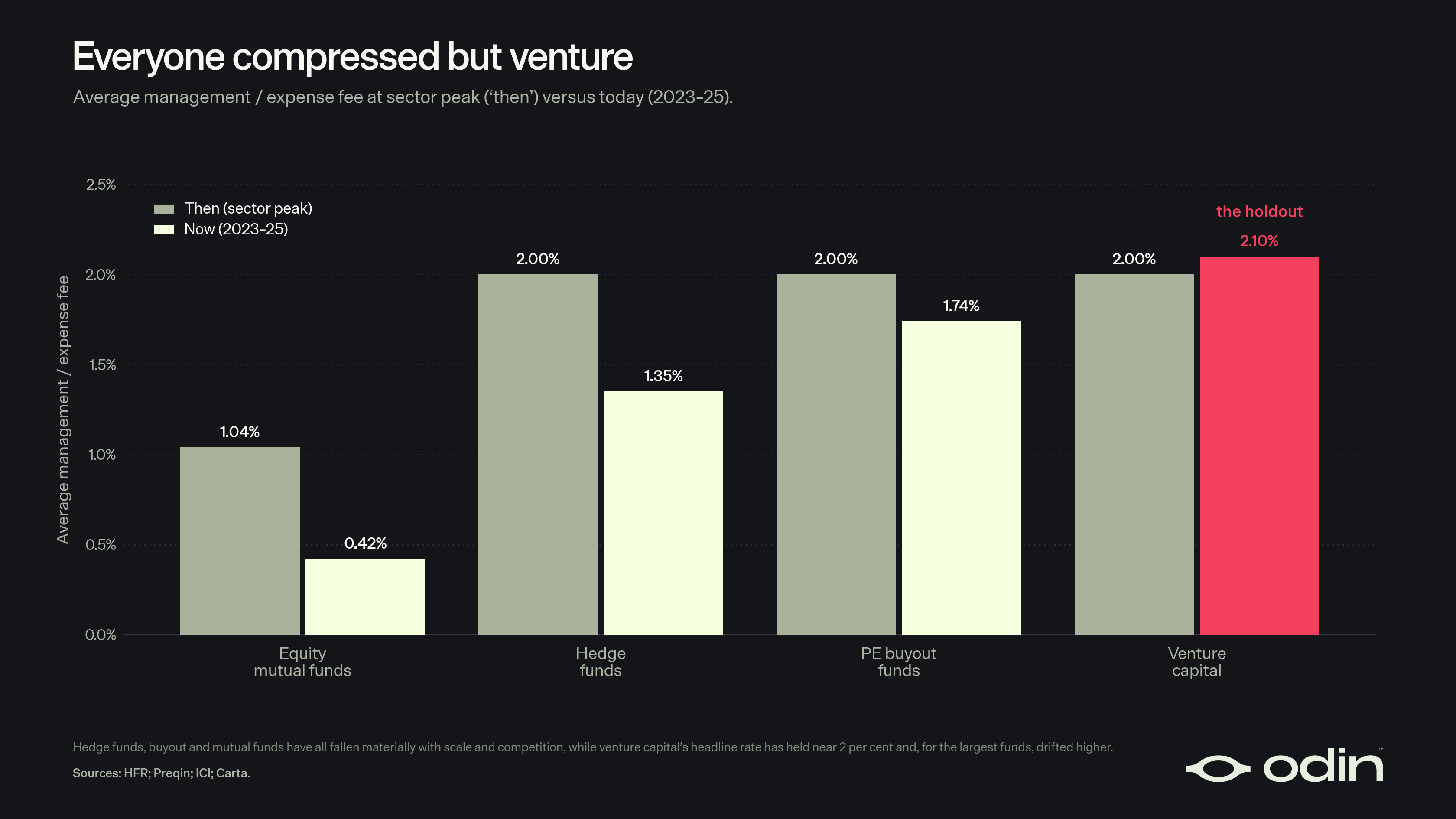

The first major change was that it became less common for management fees to scale linearly with fund size; larger funds shifted down to fees of 1.5%–1.75% as a reflection of the elementary truth that scale erodes returns.

“Performance does not appear scalable: Investments held by private equity firms in periods with a high number of simultaneous investments underperform substantially. Results are consistent with the theoretical literature on organizational diseconomies linked to firm structure. Private equity firms’ actions do not appear to be mechanical or easily scalable.”

Giants at the Gate: Investment Returns and Diseconomies of Scale in Private Equity (2015)

Beyond that, PE managers also began offering faster and more aggressive step-downs (fee percentage) and scale-downs (fee base). It became more common for fees to shift from a basis of total committed capital (fund size) to invested capital (deployed capital minus exits and shutdowns) after the initial investment period.

In summary, fee income started to more clearly reflect the actual work being done.

“Management fees should be based on reasonable operating expenses and reasonable salaries, as excessive fees create misalignment of interests.”

GPs were encouraged to provide a model of where their management fees would be spent, in order to justify their economics. There was no longer an assumption of a one-size-fits-all 2% fee.

On top of that, preferred return hurdles (usually around 8%) became ubiquitous to ensure that investors could produce returns that at least beat the opportunity cost of the investment (e.g. versus “safe” alternatives) before earning any carried interest.

Co-investment Rights

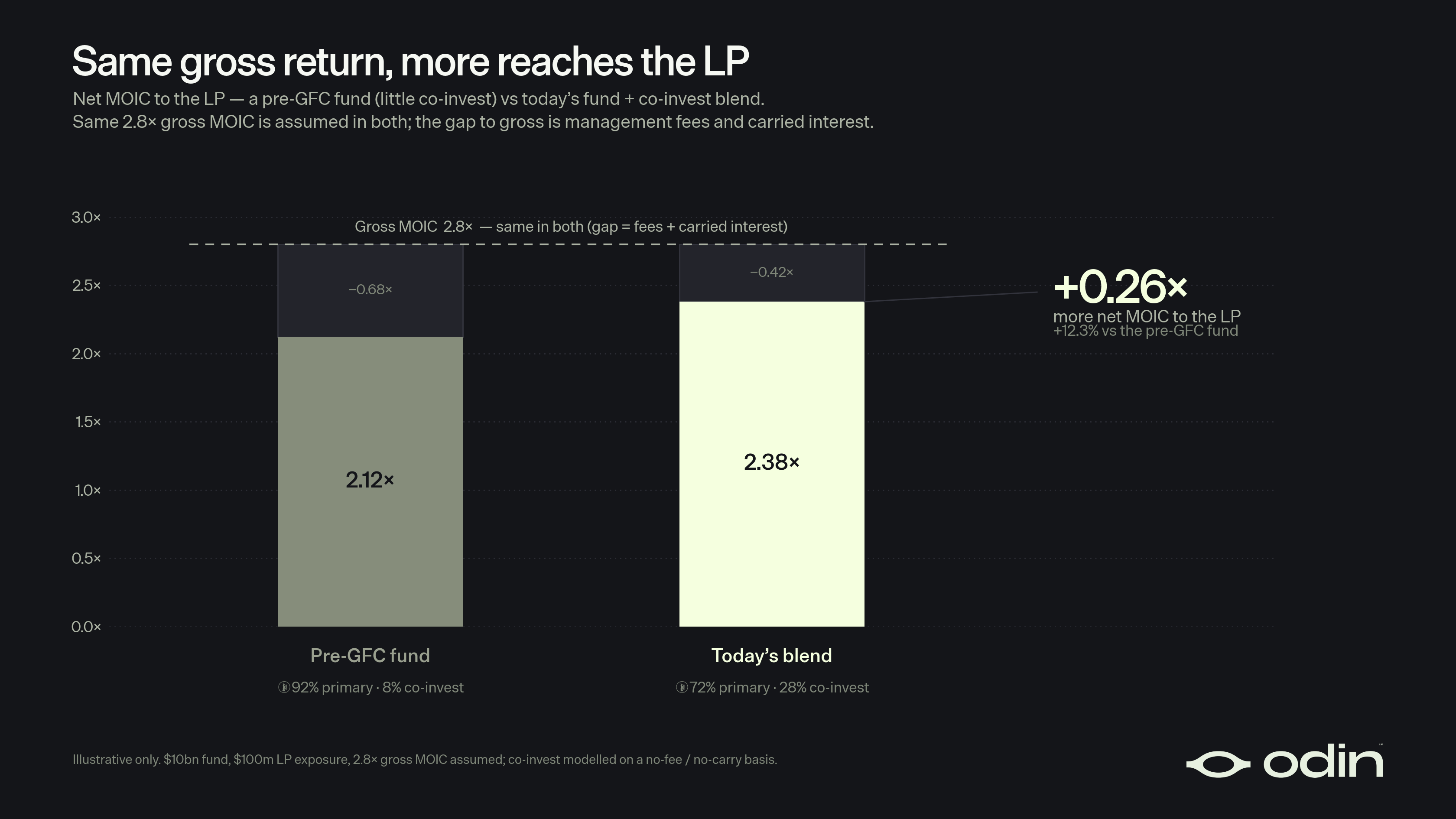

The second major change was that LPs looked to escape fund economics entirely; investing more capital on a deal-by-deal basis with little to no additional cost. So, LP agreements were altered to formalise meaningful co-investing as part of the product.

Particularly for larger firms, investing greater volumes of capital in more mature companies that carried less risk, it made sense that LPs fill more of that allocation directly. In doing so, they would eliminate the drag of fund economics and force GPs to compete for the right to manage capital directly.

Research confirms the efficacy of this move; PE LPs that build portfolios of at least 10 companies via co-investments will improve their net returns versus just putting all of that capital directly into the fund.

“Co-investments generally have lower costs to investors. We simulate net returns to investors and demonstrate how reasonably sized portfolios of co-investments significantly out-perform fund returns.”

Adverse Selection and the Performance of Private Equity Co-Investments (2016)

Better Incentives, Better Outcomes

As a result of these changes, PE GPs were no longer so clearly incentivised to raise larger and larger funds. Not only did the economics of fees and carry change, but there was also a clear path for LPs to address company funding needs directly.

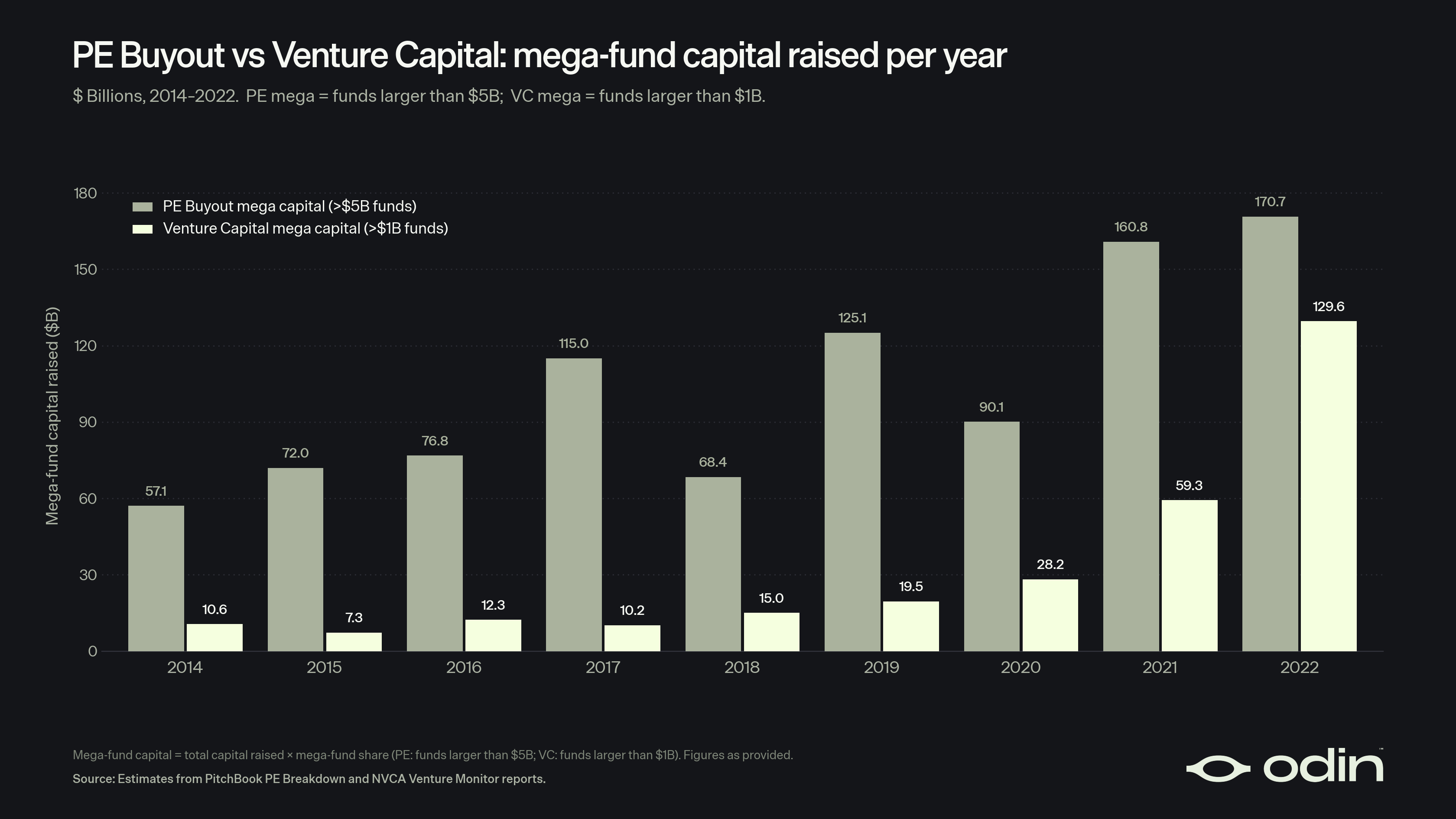

So, while ZIRP had an exponential inflationary effect on VC megafunds (>$1B), the impact was far less significant on PE buyout megafunds (>$5B).

Not only did funds remain a more rational size in PE, but the cost of capital for companies at the scaled end of that market was reduced through the lower fee drag. This produced a healthier environment for everyone involved, with stronger performance.

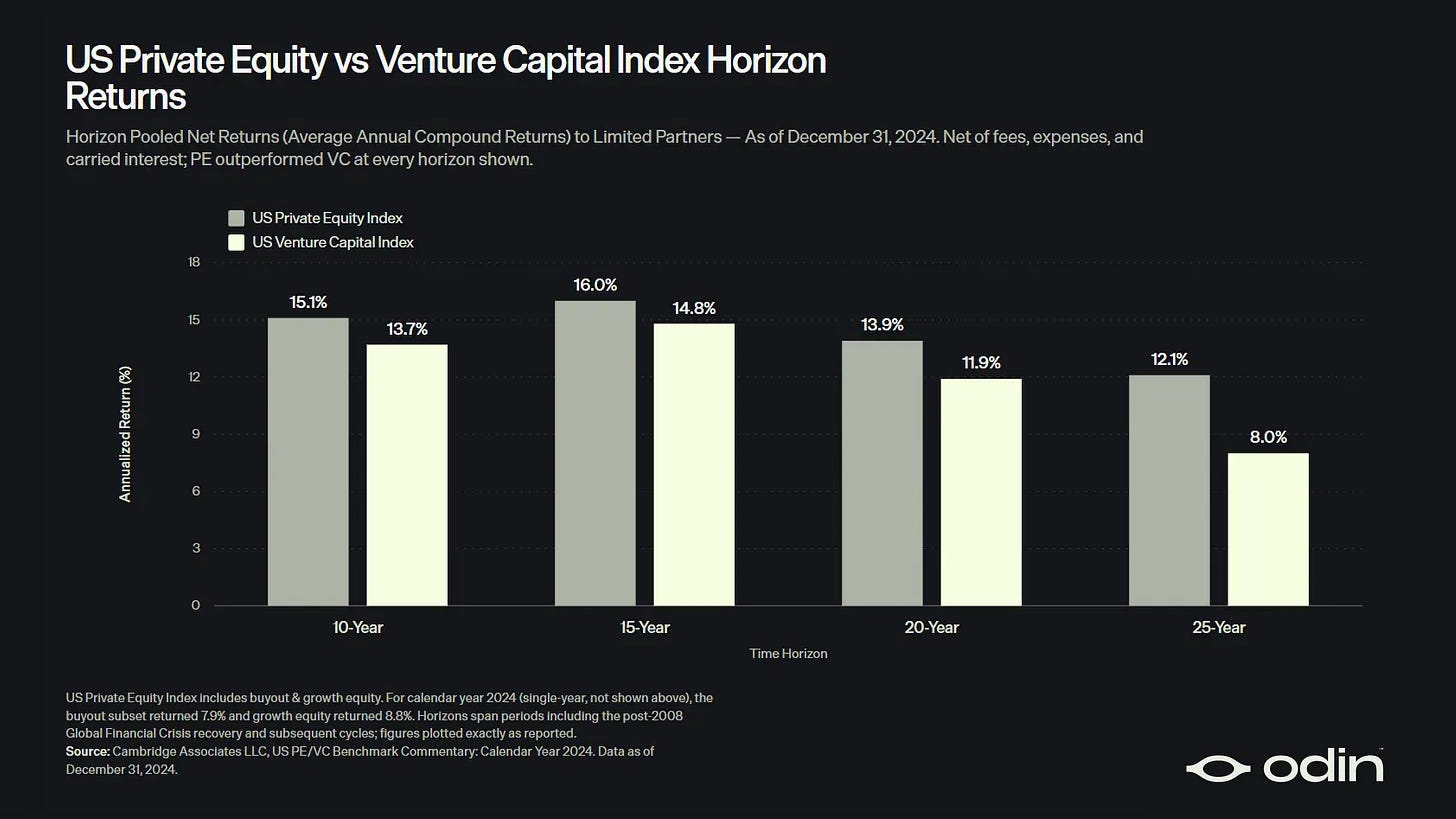

Indeed, private equity has consistently outperformed venture returns on every horizon measured in Cambridge Associates benchmarks released in 2025, despite much of the attention being on venture-backed companies in recent years.

To apply Munger’s famous maxim, “show me the incentive, and I'll show you the outcome”, if you create incentives that reward performance then you get performance.

If you create incentives that reward scale, scale is all you will get.

The Laggard

The emergence of the VC megafund has been a largely unchecked phenomenon, resulting from the influx of large LPs (e.g. sovereign wealth) in the late 2010s. This represented a dramatic shift in the capital environment from VC’s boutique roots, with no matched evolution of the market structure.

So, today, for a set of obvious and well-studied reasons, the venture market remains twisted by incentives.

Fundamentally, increasing scale drives down returns, which should be compensated for with lower fees. Especially as that excess scale is fed to a handful of late-stage, relatively mature opportunities, with the commensurate effect of delaying or destroying exits. This feels like an obvious argument to make, and an easy fix.

In fact, fee income did feel some pressure in the post-ZIRP years, for the same reasons as PE’s GFC moment; denominator headaches and a weak liquidity environment. Even Sequoia chose to cut management fees. But the moment didn’t last long enough to stick. It’s just too easy to smash any nuance about economics with the trump card of the Power Law obscuring how these incentives shape the industry.

Meanwhile, co-investment activity has grown since 2022, and is an emerging preference amongst more sophisticated LPs, though it has yet to become a standardised offering across the industry.

“We plan to selectively increase our co-investments alongside our highest conviction managers, on a fee-advantaged basis, in a sub-set of late-stage technology companies that are emerging category leaders, have demonstrated product-market fit and have proven attractive unit economics.”

Partners Capital, Insights (2026)

Before co-investment rights can shape behavior, they must be an expected practice; understood as a feature of a good fund, led by a properly aligned manager who cares about maximising returns. This also requires more work for LPs. Reiner, Jenkinson and Schemmerl’s paper describes a similar payoff to PE, where co-investing produces stronger returns for an LP’s VC strategy, but after making at least 20 investments — rather than the 10 for PE.

The future of fees is more challenging. On one hand, it is clear that fees should scale with performance, not fund size. Particularly because increasing fund size will erode performance. The current setup is a paradoxical mess. On the other hand, LPs are trapped in a prisoner’s dilemma where nobody wants to be the one that puts their foot down first and risks being blackballed by “top” firms. Especially when access to scaled venture allocation via a megafund is more about the short-term career incentives for institutional allocators than it is about long-term performance.

The notion that performance should be reflected by increasing the fee base (fund size) rather than the fee size (percentage) is particularly pernicious in downturns. When the market cools, managers respond by cutting fund size, meaning less capital is available to deploy in an environment that is likely to offer better value. If percentage was the obvious lever in a downturn, rather than fund size, firms would have to run leaner but would be less constrained on deployment, paving the way for a rebound.

The Case for Change

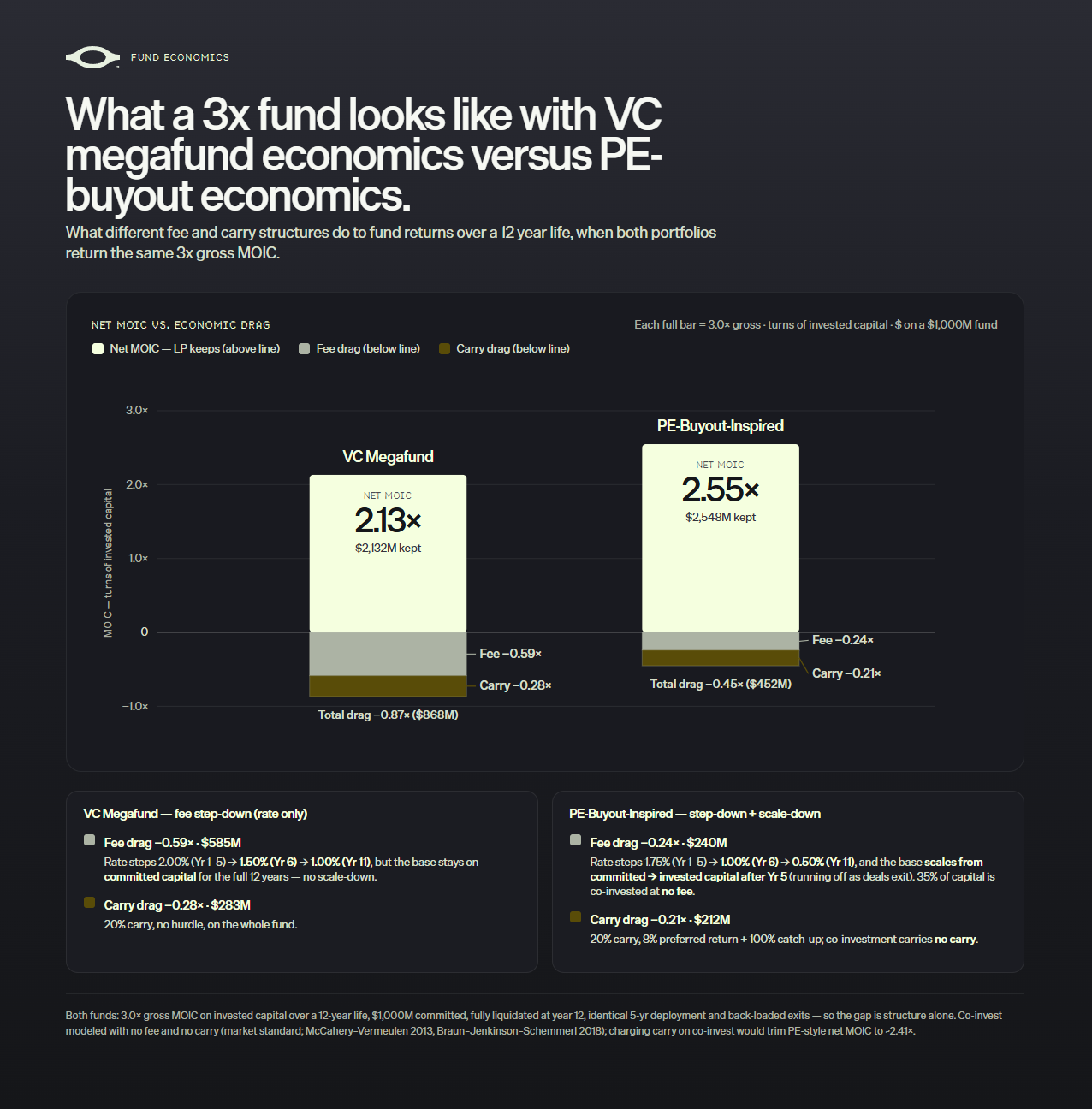

The case for change is simple: As VC megafunds have reached a similar scale and risk profile to the PE buyout strategy, they ought to shift to PE buyout economics.

This case can be tested quite easily, by applying the lessons and structural changes of PE buyout, as described in the McCahery and Vermeulen paper, to VC’s megafunds; adopting similar non-linear fund scaling, step-downs and scale-downs, alongside stronger co-investment rights.

There are serious gains to be made; an estimated +0.42x lift in net MOIC and an additional 2.6% net IRR versus the performance with current fund economics. It’s a straight shot to improve incentives and returns.

But, it’s worth emphasising the systems logic.

There is an easy case to be made with relative individual fund performance, but focusing too much on that comparison is to miss the forest for the trees.

LPs should want better standards, across the industry, because it would correct the incentives which determine everything from where VCs invest to how they think about exits. It’s a deep and systematic improvement to a strategy that has lost its way in recent years. An end to mindless agglomeration and stagnation.

The current venture capital market structure reflects money for pensions, endowments and sovereigns that is being left on the table because the strategy is captured by incumbents and funded by cowards.

Explore this topic in more detail in our memorandum on evolving VC market structure, The Barbell.

Run your investment firm from your phone, with Odin