National Capitalism

Creating the financial scaffolding for state-led reindustrialisation

“Venture investments tend to be focused on a few areas of technology that are perceived to have great potential. Increases in venture fund-raising which are driven by factors such as shifts in capital gains tax rates appear more likely to lead to more intense competition for transactions within an existing set of technologies than to greater diversity in the types of companies funded.

Policymakers may wish to respond to these industry conditions by (1) focusing on technologies which are not currently popular among venture investors and (2) providing follow-on capital to firms already funded by venture capitalists during periods when venture inflows are falling.”

Short-Term America Revisited? Boom and Bust in the Venture Capital Industry and the Impact on Innovation, by Josh Lerner and Paul Gompers

In January 2026, Andreessen Horowitz announced that it had raised over $15 billion across five new funds, its largest haul to date, bringing total assets under management above $90 billion. A few months earlier, General Catalyst closed approximately $8 billion for its twelfth fund. These are staggering sums that represent an extraordinary concentration of capital, at a time when broader venture fundraising has been notably weak. In 2025, US firms secured just $66.1 billion for new funds, down from $101.3 billion in 2024 and well below the 2022 peak of nearly $223 billion.

And yet, for all this firepower, many industries where capital is most needed remain chronically underfunded. Building a small modular nuclear reactor costs billions and takes more than a decade. Bringing a new cancer drug through clinical trials demands an average of $1 to $2 billion over ten to fifteen years, with a roughly 90% probability of failure. The fusion energy companies that could supply limitless clean power face development cycles stretching decades into the future. These are the technologies on which civilisational progress most clearly depends. They are also the technologies that venture capital, as currently structured, is least equipped to fund.

The question of why this is so, and whether anything can be done about it, has occupied researchers and policymakers for years. Today, as governments across the West embrace reindustrialisation, and the limitations of financialised economies become harder to ignore, it is increasingly urgent.

A growing body of academic work describes a solution (or a combination of three solutions) which would operate in harmony with private investors to strengthen the entire venture and growth ecosystem without repeating mistakes of the past:

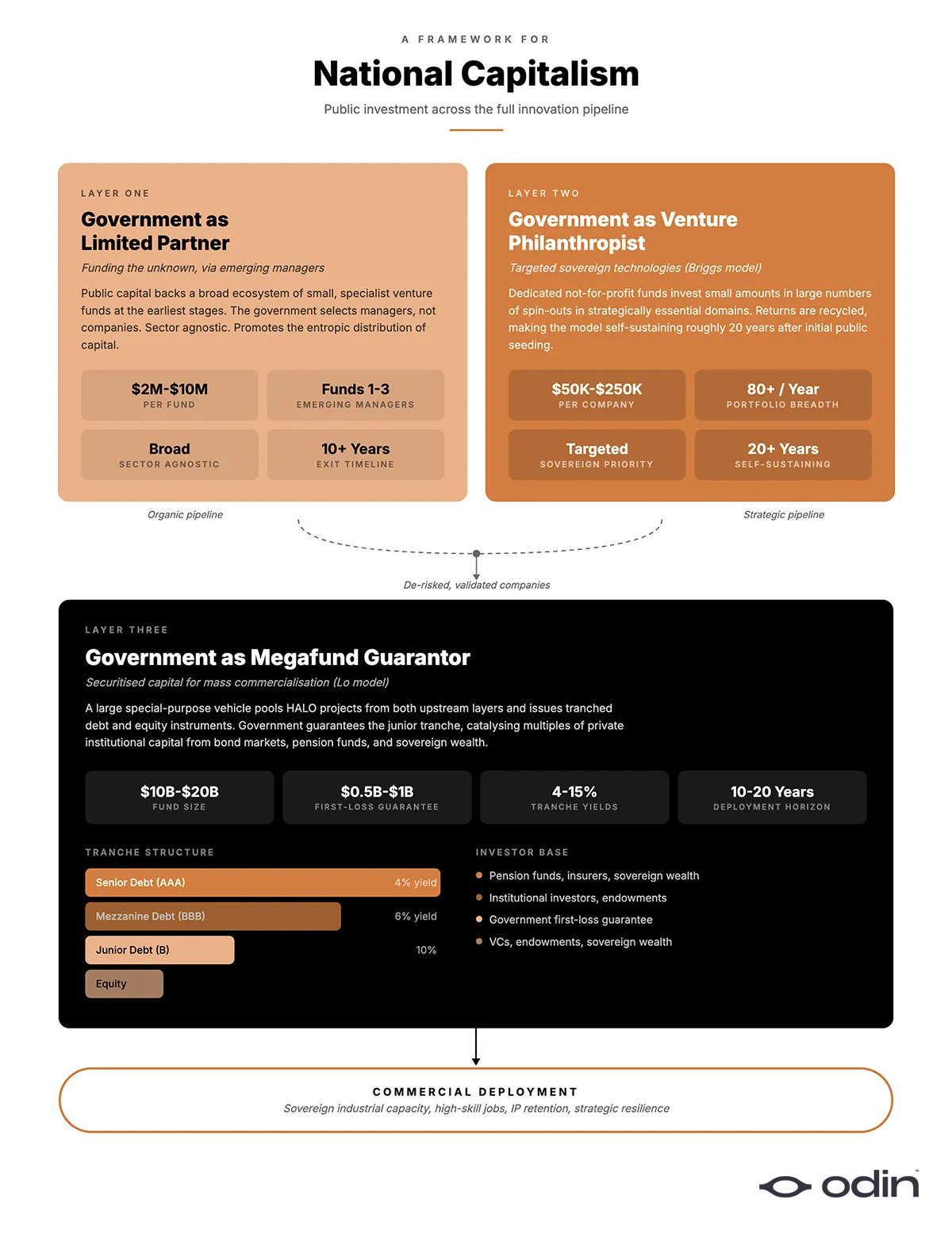

The government as a limited partner for emerging managers. Addressing the network-driven constraints in venture capital that favour incumbents, reducing competition via limiting the threat of new entrants.

The government as a venture philanthrophist for sovereign technology. Addressing the difficulty that highly novel and capex intensive ideas may have in raising capital from the general pool of venture capital firms.

The government as a megafund guarantor of growth equity and debt. Addressing the hurdle into public market by providing later stage mezzanine financing which brings down the cost of capital for strategically valuable companies.

Each pillar of this strategy exploits the government’s ability to direct investment on longer time horizons and appreciate benefits beyond simple cash returns.

Impatient Allocation

Venture capital has been, by almost any measure, one of the most potent engines of innovation in economic history. Research illustrates that a dollar of venture capital is three to four times more effective at stimulating patenting than a dollar of traditional corporate R&D. The model is powerful, for a particular kind of company.

“The estimates therefore suggest that venture capital, even though it averaged less than 3% of corporate R&D from 1983 to 1992, is responsible for a much greater share—perhaps 10%—of U.S. industrial innovations in this decade.”

The Venture Capital Revolution, by Josh Lerner and Paul Gompers

The trouble is that the model’s structural incentives push capital towards certain categories of investment and away from others. A traditional venture fund has a ten-year life. Its general partners are rewarded on carried interest, a share of profits above a hurdle rate that must be realised within that fund’s lifetime. This creates a preference for investments that can reach a liquidity event, whether through IPO or acquisition, within that time period. Software companies with low capital requirements, rapid iteration cycles, and high gross margins are a natural fit. Companies building heavy physical infrastructure over fifteen-year timelines are not.

“The decision to continue funding certain compounds or technologies is often based on the likelihood of exiting the investment at a later date. If capital market conditions are unfavorable, or if the economy is not robust, pharma companies and venture capitalists may postpone or withdraw funding until the market environment improves, irrespective of the scientific merits of the project.”

Frequently Asked Questions About Megafunds, MIT Laboratory for Financial Engineering

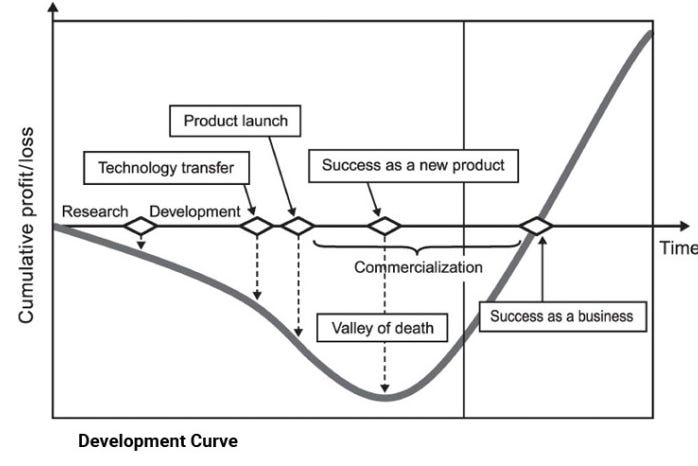

This creates what researchers call the “valley of death,” a funding gap that opens after initial proof of concept but before a technology is commercially viable. For capital-intensive, long-horizon industries, this gap can be fatal. An estimated 80% of energy startups fail not because their technology does not work, but because they cannot sustain funding through the scaling phase.

Moreover, venture capital is intensely cyclical. During booms, capital floods into whichever category of technology appears hottest, to the point of oversupply. During busts, funding for even promising ventures evaporates. Government programmes designed to spur venture activity have frequently compounded this problem by targeting sectors already awash with private capital, rather than addressing gaps in the market. As the researchers note, many policy steps have had the consequence of exacerbating the cyclical nature of venture funding, rather than smoothing it.

Far too often, the short-term appearance of a successful programme is more important than actual success in driving innovation. This is a direct reflection of venture capital’s wider problem with the incentives of generating markups for fundraising purposes.

“While there were other sectors that held enormous technological promise and where entrepreneurs were struggling to raise money (alternative energy technologies, for one), these officials were drawn, like moths to a flame, to the sectors that were already overfunded by angel investors and venture funds alike. This decision may have been rational for the ATP bureaucrats eager to ensure their program’s survival. But it was profoundly at odds with the program’s mission to identify and rectify failures in the market for funding early-stage technologies.”

Boulevard of Broken Dreams: Why Public Efforts to Boost Entrepreneurship and Venture Capital Have Failed—and What to Do About It, by Josh Lerner

Scaled Funds, Limited Appetite

You may look at the emergence of scaled venture funds and see the beginnings of a solution. Firms like Andreessen Horowitz and General Catalyst now command capital at a scale that was unthinkable a decade ago. Their limited partners include sovereign wealth funds, major pension systems, and other large institutions that are able to invest on longer time horizons. In theory, this should allow for more patient investment in capital-intensive technologies.

In practice, it does not, or at least not sufficiently. The structural incentives of the traditional limited-partnership model remain in place regardless of fund size. LPs hope for returns of 20–30%. The pressure to invest in sectors where such returns are achievable has intensified. As Ben Horowitz wrote in announcing the raise, the firm’s mission is to ensure that the United States wins “the key architectures of the future,” meaning AI and crypto.

General Catalyst, similarly, has framed its latest fund around “applied AI” and “global resilience,” with a strong emphasis on building technology stacks that can be rapidly deployed within existing industries. These are sophisticated strategies, but they remain oriented towards categories where there is already a significant concentration of private capital to drive activity.

Essentially, their strategy to achieve competitive returns at scale is not to exploit larger LPs patience to invest in longer-term projects, but instead to hold “hot” companies for longer, harvesting more of their growth in private markets before seeking an exit, which has a number of negative consequences.

The result is a venture industry with more capital available than at any point in history, yet one that remains structurally unable to fund the technologies most needed for long-term economic security and industrial prosperity. The biggest funds chase the biggest near-term opportunities, and the hardest problems remain ignored.

Sovereign Megafunds

This is where the work of Andrew Lo and his collaborators at MIT’s Laboratory for Financial Engineering offers something genuinely different. Lo’s “megafund” thesis, first developed in a 2012 paper in Nature Biotechnology and subsequently extended to fusion energy, proposes a financial structure specifically engineered for what Josh Brown, CEO of Ritholtz Wealth, has termed “HALO“ companies; Heavy Assets, Low Obsolescence.

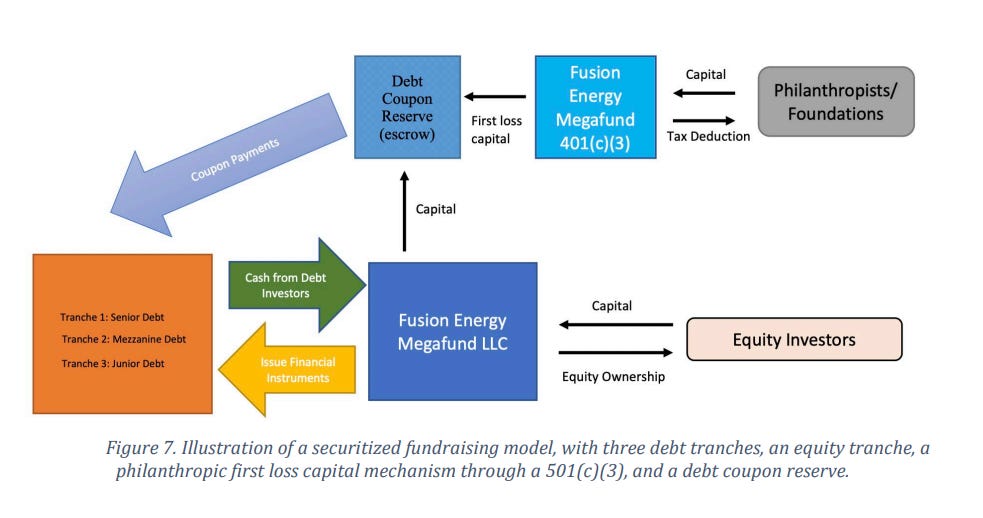

Rather than asking venture-style equity investors to bear the entire risk of long-horizon, high-failure-rate R&D, the megafund pools a large number of projects, typically fifty to three hundred, into a single special-purpose vehicle. It then finances this portfolio not through traditional LP commitments alone, but through securitisation; issuing tranched financial instruments that appeal to different categories of investor.

The senior debt tranches offer low-risk, fixed returns, similar to corporate bonds, and are designed for conservative institutional investors such as pension funds and insurers. Mezzanine debt tranches offer moderate risk and return. Equity tranches absorb the highest risk but also capture the greatest upside. The structure is analogous to mortgage-backed securities, though applied to a portfolio of research and development projects rather than home loans.

“In 2018, $254B was invested globally through venture capital financing, while the size of the global bond market stood at $102.8T, more than 400 times larger.”

Financing Fusion Energy, by Alhamdan, Halem, Hernandez, Lo, Singh, and Whyte

The pool of capital available through debt markets dwarfs the venture capital industry by orders of magnitude. By creating instruments that allow conservative institutional investors to participate in breakthrough R&D at a risk level they find acceptable, the megafund taps into a reservoir of financing that has been largely inaccessible to innovation. The ability to finance through debt also carries a lower cost of capital than equity, thanks to the tax deductibility of interest expenses, further improving the economics of the portfolio.

Lo and his collaborators have run extensive simulations demonstrating that this approach produces viable returns. Using historical oncology data from 1990 to 2011, they showed that a $5–$15 billion megafund could generate average annual returns of 8.9–11.4% for equity holders and 5–8% for debt holders, even accounting for the brutal attrition rates of drug development. Applied to fusion energy, simulations of a $10–$30 billion fund yielded projected returns of 7–12%, assuming moderate correlations between projects and occasional breakthroughs.

Crucially, the megafund also incorporates mechanisms for de-risking that go beyond simple diversification. Governments and philanthropic partners can provide “first loss capital” guarantees, effectively backstopping the most junior tranches to give private investors confidence. Lo and his collaborators have proposed that this philanthropic first-loss component would require initial funding of at least $500 million to guarantee five or more years of payments to senior tranche investors. This public-private hybrid design makes the megafund a particularly attractive instrument for government funding initiatives and large institutional LPs such as sovereign wealth funds and public pension funds, which are not only patient and well-capitalised but ideologically aligned with the kinds of positive externalities such as clean energy, public health breakthroughs, and national strategic resilience.

“We further de-risk the megafund by leveraging first loss capital guarantees from philanthropic sources and governments to fund coupon payments to senior and mezzanine bondholders in its early years.”

Financing Fusion Energy, by Alhamdan, Halem, Hernandez, Lo, Singh, and Whyte

This public-private hybrid potential makes the megafund extremely relevant to the current policy conversation. Governments seeking to accelerate energy transitions or secure domestic supply chains do not need to shoulder the entire financial burden themselves; by guaranteeing junior tranches, they can catalyse multiples of private investment. The taxpayer’s exposure is limited to the first-loss layer, while the vast majority of capital comes from private institutional sources attracted by the risk-adjusted return profile of the senior debt. The Israeli Life Sciences Fund already serves as a proof of concept for how government loan guarantees can stimulate private investment.

“The government provided some $50 million as a limited partner. Its funding serves as the first-loss capital through a preferred return scale, which allows for positive returns to other limited partners even if the fund suffers as much as a 10 percent loss. This structure has proved an attractive proposition for the fund managers (OrbiMed Israel Partners LP), who were able to raise the $172 million on top of the government's $50 million.”

Financing High-Risk Medical Research, by Melissa Stevens

Launch and run a private investment firm online, and work with over 10,000 VCs, angels and founders globally.

Set up an SPV or fund vehicle in less than a day, with Odin.

The Discovery Layer

One important qualification is that Lo’s megafund is not designed for inception-stage companies. It operates at the point in the cycle where the technology has been validated at some initial level but still requires massive capital to scale.

This is where small VC firms and emerging managers play a critical role, forming what can be considered the “discovery layer”, the initial interface between capital and innovation. Investors who find, fund, and develop the raw ideas that will eventually become candidates for megafund investment. A seed-stage investor working with a university spin-out developing novel fusion confinement technology, or a pre-seed fund backing a team designing advanced reactor components, are doing the essential work of making scientific breakthroughs “legible to capital”.

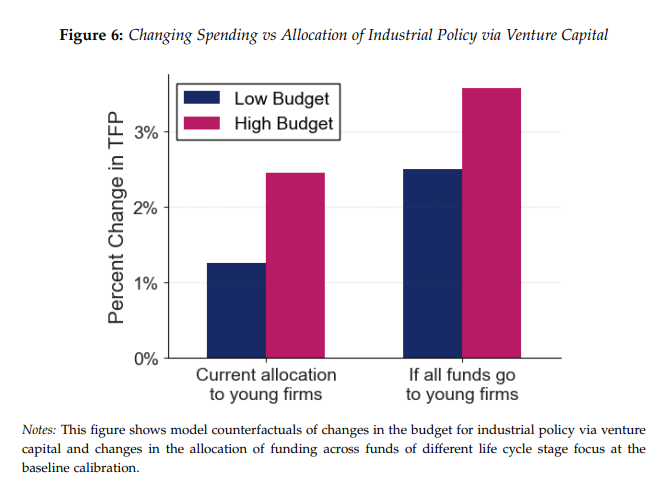

Research consistently supports this view. A 2025 study of government venture capital investment across Europe found that redirecting allocated capital towards early-stage investments produced the same productivity uplift as doubling the total capital allocation. The authors documented that government-linked VC financing had its strongest and most persistent effects when focused on young firms, despite the fact that public VC portfolios were systematically skewed towards later-stage companies. Separate research across other EU member states demonstrated that where governments fund emerging fund managers, they may produce above-market success rates and stronger job creation.

Indeed, a 2025 report by the Institute for European Policymaking and the ifo Institute reinforced this finding, showing that the EU’s roughly 100 billion euros of Horizon innovation funding had disproportionately flowed to large corporations with modest innovation records, while single-recipient grants to small, independent firms yielded the best long-term results.

“Any new Framework Program should thus focus on funding ideas, not companies. The key is not more money, but rather leaving space for disruptive innovation by encouraging bottom-up initiatives, especially by small independent companies.”

Funding Ideas, Not Companies, by Fuest, Gros, Mengel, Presidente, and Rujan

A healthy innovation ecosystem, then, would feature small funds scouring early-stage companies for breakthrough potential; developing those ideas through initial prototypes and regulatory milestones; and then passing the most promising candidates upward into a megafund structure capable of sustaining them through the capital-intensive scaling phase.

This complementary relationship could, if properly structured, strengthen both ends of the ecosystem. Emerging managers would have a clearer path for their portfolio companies beyond Series A, and potentially avenues for earlier liquidity, making their own funds more attractive to LPs. Megafunds would have a steady pipeline of de-risked, validated opportunities to absorb. The valley of death narrows considerably when there is a bridge waiting on the other side.

Venture Philanthropy

The megafund model and the discovery layer of emerging VC managers address the two critical stages of large-scale capital deployment and early-stage deal sourcing. There remains another category of technology for which even these structures may not move quickly or deliberately enough. When a government determines that a particular capability is strategically essential, whether in advanced materials, quantum computing, or biodefence, it may not wish to wait for a venture ecosystem to emerge around that technology.

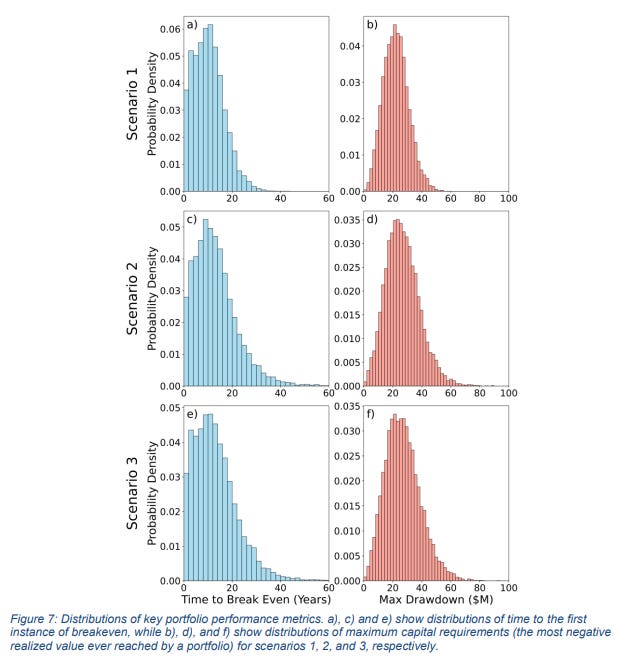

Kyle Briggs, a physicist at the University of Ottawa who works on innovation policy and technology transfer, has developed a framework for exactly this problem. In a 2026 study drawing on PitchBook data covering 9,199 university-affiliated startups across North America and Europe, Briggs simulated the long-term performance of several strategies for investing in the earliest stages of research commercialisation.

His findings reflect a growing consensus about early stage investment in venture capital, where the most important variable in determining success is not the picking ability of the fund managers, but the portfolio size. Broad investment of small amounts of capital in a large number of startups statistically outperforms concentrated investment in fewer companies, by a wide margin. The returns from emerging technology commercialisation follow a highly asymmetric distribution in which a tiny minority of investments generate the vast majority of value. Under-sampling from such a distribution, as risk-averse investors often will, dramatically reduces the probability of capturing those outliers.

“Risk-intolerance creates a negative feedback loop in which under-sampling driven by risk aversion leads to subpar returns, which in turn reinforces the risk aversion that is in fact the root cause of the problem.”

Bootstrapping an Innovation Ecosystem, by Kyle Briggs

If it is effectively impossible to predict which early-stage research commercialisation attempts will succeed, then the correct strategy is not to try to pick winners but to fund widely, tolerate high failure rates, and trust that the statistical properties of the portfolio will deliver returns over time. A high rate of failure is a positive signal, indicating that the fund is investing broadly enough to be confident that it is not missing the valuable minority.

Briggs proposes a vehicle he calls “venture philanthropy”, in which a not-for-profit entity, seeded with public funds, makes small equity investments, typically $50,000 to $250,000, into a large number of university spin-outs and early-stage deep-tech companies at founding or shortly thereafter. Returns from successful exits are recycled into the fund to support the next generation of technologies. Because there is no profit-sharing obligation and no fixed fund lifetime, there is no time pressure to realise returns, making these investments genuinely patient capital. Because the fund is structured as a charitable entity, it can also solicit private donations, sharing the risk between public and private sectors while offering tax benefits to contributors.

The UK’s Innovation and Science Seed Fund provides a real-world example. It is credited with the existence of 78% of the companies in which it invested, and claims £29 of private follow-on capital for each £1 it has deployed.

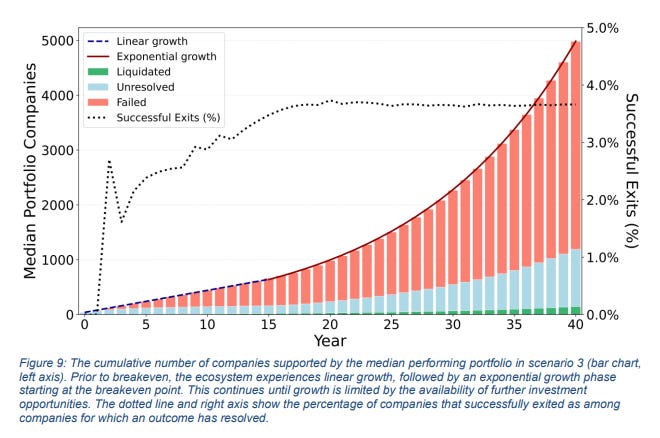

Briggs’s simulations, using Monte Carlo methods across thousands of portfolio scenarios, demonstrate that this model can be self-sustaining. In his central scenario, a fund investing $4 million per year across eighty companies annually, taking small equity positions via convertible instruments, reaches breakeven at a median of approximately twenty years. The median annualised internal rate of return rises to 11.6% by year thirty and 13.5% by year forty.

More importantly, once breakeven is achieved, the fund enters an exponential growth phase as returns from successful exits are reinvested into an ever-larger number of new companies, and the ecosystem itself begins to compound. The vast majority of individual investments, over 96%, fail. But the realised value of the successful outliers more than covers the cost of those failures, and the broader economic benefits, in job creation, talent retention, and intellectual property kept within the sovereign jurisdiction, compound well beyond the fund’s direct financial returns.

“If seeded with public funds that are then augmented with private donations, venture philanthropy shares the risk of emerging technology investment between the public and private sectors, accepting a high rate of failure, long timelines, and sub-market profits that neither the public nor private sectors would tolerate alone. Because the goal is not profit beyond the need to be self-sustaining and operationally solvent, venture philanthropy measures success in terms of talent and IP retention, training first-time founders, company and job creation, and advancement toward societal goals.”

Bootstrapping an Innovation Ecosystem, by Kyle Briggs

The decades-long timeframe, initial target returns and the sheer number of investments required to reduce variance are mostly incompatible with a private-sector-led initiative. This is precisely why the private sector has not addressed this funding gap, and many emerging technologies have no reliable pathway from the lab to the market. A competitively-minded government, willing to accept modest financial returns in exchange for the broader economic and strategic benefits of a thriving domestic innovation ecosystem, is the obvious enabler.

The American SBIR programme, which until recently funded a comparable stage of research commercialisation, is estimated to create $22–$33 of economic value for every dollar invested. If a government can achieve even a fraction of that return while simultaneously retaining intellectual property and entrepreneurial talent within its borders, the case is easily made. The challenge is they must also be willing to tolerate high visible failure rates, resist the temptation to pick winners, and commit to investment horizons that extend well beyond electoral cycles, which are not natural instincts for public institutions.

The alternative, watching scientific breakthroughs and human capital leak to other jurisdictions, is a far more expensive form of failure.

A Long Time Coming

The problem of short-termism in venture capital and in the broader economy is not new. As far back as the 1980s, researchers were warning about “capital market myopia,” the tendency of financial markets to undervalue long-horizon investments.

“The purpose in writing this article is to focus attention on a phenomenon we call capital market myopia, a situation in which participants in the capital markets ignore the logical implications of their individual investment decisions. Viewed in isolation, each decision seems to make sense. When taken together, however, they are a prescription for disaster. Capital market myopia leads to overfunding of industries and unsustainable levels of valuation in the stock market.”

Capital market myopia, by William A. Sahlman and Howard H. Stevenson

The cyclical nature of venture funding, documented extensively by Gompers and Lerner, has been a persistent feature of the industry since its inception.

What has changed is the broader economic context, and increasing financialisation. Carlota Perez, the queen of techno-economics, has argued that the prolonged period since the dot-com crash represents a historically unusual failure to transition from an “installation period” of creative destruction to a “deployment period” in which new technologies are broadly diffused through the economy. In previous technological revolutions, from the steam age to the era of mass production, a financial crash midway through the cycle prompted institutional reform that redirected capital towards productive investment. This time, that correction has not occurred.

“The most acute impediment to a golden age deployment is the continued decoupling of finance from production. The usual casino of the frenzy periods has remained in force since the NASDAQ bubble, with major variations in form, but not in essence.”

A Long Delayed Golden Age: Or why has the ICT ‘installation period’ lasted so long?, by Carlota Perez

The reason, in Perez’s analysis, is that government responses to successive crises, from the dot-com bust to the 2008 financial crisis to the pandemic, have consistently prioritised the financial system over the productive economy. Quantitative easing pumped liquidity into banks without conditions requiring productive lending. Interest rates remained at historic lows for over a decade, making speculative financial activity far more attractive than patient investment in industrial capacity. As Perez observes, since the favoured banks were not required to use the money to fund the real economy, production investment and productivity increases remained at all-time lows, while the financial world played with derivatives and synthetic instruments across the globe.

This has clear alignment with developments in venture capital over the last few decades. Cheap capital encouraged larger fund sizes and higher valuations, but did not necessarily encourage better allocation. When money is abundant and cheap, the incentive to undertake disciplined, long-horizon investment in difficult technologies actually diminishes. It is easier, and more immediately rewarding, to fund software companies with two-year paths to revenue than to fund nuclear energy companies with fifteen-year development cycles.

"[VCs] furthered the financialization of firms, allocating capital to far from ideal uses and obtaining a share of the gains incommensurate with the risk or labor invested. In sum, VCs deepened asset-driven inequalities by devising a particular handling of abundance, which materialized in building a financial infrastructure for their needs."

Solving the problem of abundance: venture capital and the making of asset-driven inequalities, by Nils Peters

Today, however, the mood is shifting. The reindustrialisation movement, accelerated by supply chain disruptions, geopolitical competition with China, and growing awareness of the vulnerabilities embedded in deindustrialised economies, has created a new political and institutional appetite for productive investment. Governments across the West are deploying industrial policy at a scale not seen in decades.

In this environment, the government’s role as an LP and a VC, alongside the megafund model, offer a framework that aligns private incentives with public goals, directing large pools of institutional capital towards the most consequential challenges.

Putting It Together

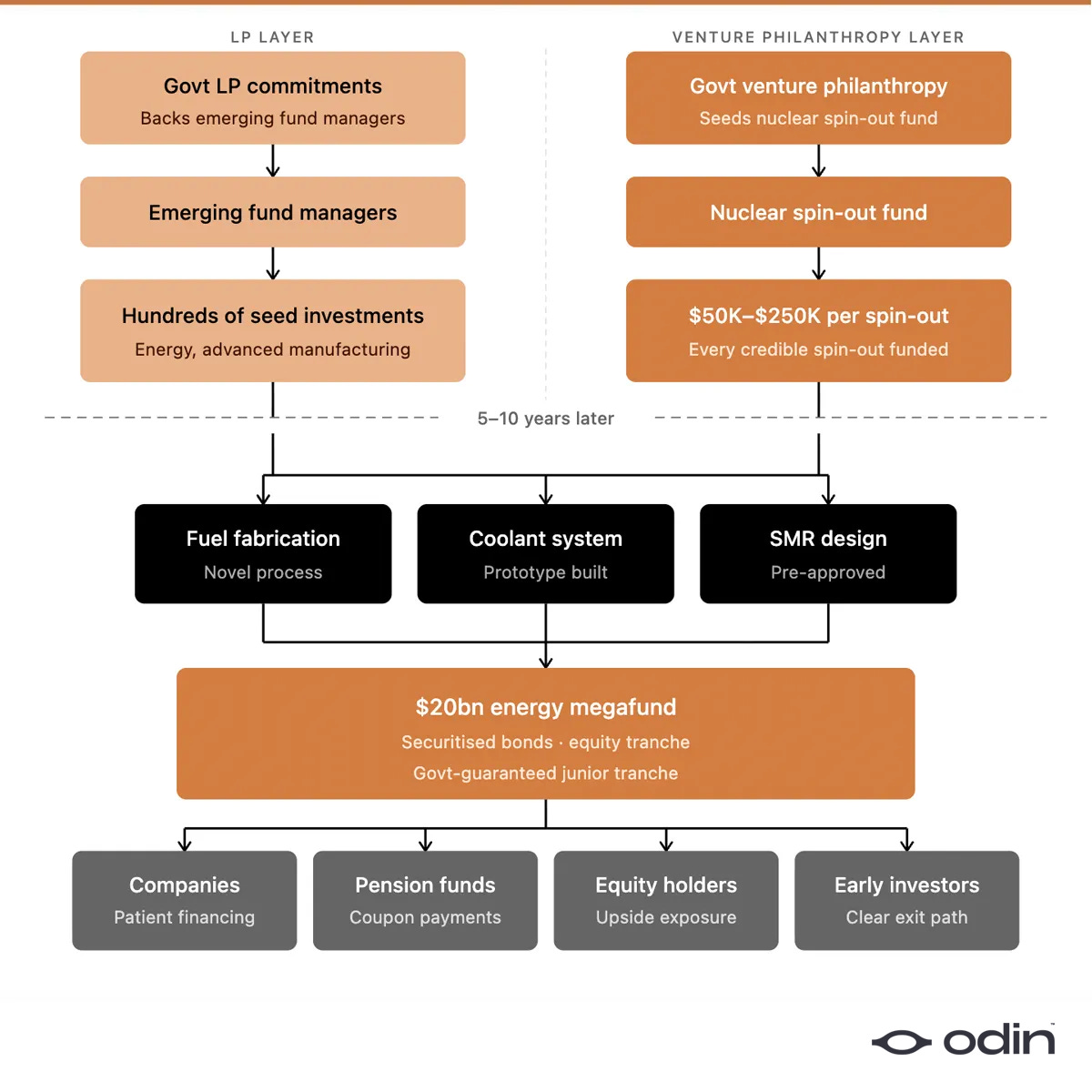

Consider how this three-layer stack would operate in practice for a government pursuing an advanced nuclear strategy.

At the LP layer, the government commits capital to a cohort of emerging fund managers who invest across a range of technologies including energy and advanced manufacturing. These managers make hundreds of seed investments across the sector, including in companies developing novel reactor components, advanced materials, control systems, and grid integration technologies.

Simultaneously, at the venture philanthropy layer, the government seeds a dedicated fund targeting nuclear technology spin-outs from national laboratories and universities. This fund invests $50,000 to $250,000 in every credible spin-out attempting to commercialise relevant research, regardless of perceived probability of success.

Five to ten years later, a handful of companies from both layers have demonstrated genuine technical progress. One has developed a novel fuel fabrication process. Another has built a prototype coolant system. A third has achieved regulatory pre-approval for a small modular reactor design. These companies now need capital at a scale that neither small VC funds nor venture philanthropy can provide.

A $20 billion energy megafund, backed by securitised bonds rated for institutional investors and an equity tranche for endowments and sovereign wealth funds, absorbs these companies into a diversified portfolio alongside fusion ventures, grid-scale storage projects, and other energy technologies. The government guarantees the fund’s junior tranche, limiting taxpayer exposure to the first-loss layer while catalysing multiples of private institutional capital. The companies receive the patient, large-scale financing they need. The pension funds receive steady coupon payments from the senior debt. The equity holders gain exposure to transformational upside. And the early-stage investors, both the emerging managers backed by government LP capital and the venture philanthropy fund, have a clear exit path for their positions, improving their own returns and making them more attractive to future investors.

The beauty of this structure lies in the fact that each layer’s weakness is addressed by another layer’s strength. Small VC funds are excellent at discovery but cannot deploy capital at scale or over long timelines. The megafund can deploy capital at scale over decades but cannot source unproven, early-stage opportunities. Venture philanthropy can fund broadly and patiently at the inception stage but produces returns too slowly and too modestly for private investors. Government LP activity can support an ecosystem of emerging managers but cannot direct capital towards specific strategic priorities.

The total public expenditure required is, by the standards of government budgets, remarkably modest. An LP commitment of perhaps $200 to $500 million spread across a generation of emerging fund managers. A venture philanthropy seed of $50 to $100 million in each of several strategically targeted technology domains. A first-loss guarantee of $500 million to $1 billion to catalyse a megafund that raises $10 to $20 billion from private institutional sources. Against these outlays, the government receives a growing domestic innovation ecosystem, strategic control over critical technology supply chains, high-skill job creation, and, over the long term, a financial return on its investments that compares favourably with most other categories of public expenditure.

What this framework demands of governments is long-term thinking, institutional patience, and a tolerance for visible failure. Most companies funded by the venture philanthropy layer will fail. Many of the emerging managers supported at the LP layer will produce unremarkable returns. Some projects within the megafund will collapse entirely. These outcomes are the necessary cost of a strategy built on portfolio logic rather than the illusory pursuit of certainty. The alternative, which most governments currently favour, is to fund a small number of carefully selected projects and companies, demand accountability at every stage, and declare success or failure on the basis of individual outcomes. It appears more responsible on the surface, but is, in fact, far more wasteful on the balance of ultimate outcomes (never mind the risks associated with adverse selection and choking innovative companies with red tape).

Right now, innovation is unable to channel public investment and large institutions to the points in the pipeline where they will have the most impact. The three-layer model described here (government as LP, government as venture philanthropist, and government as megafund guarantor) offers a blueprint for each stage of the pipeline, from the first hint of an idea in a university laboratory to the deployment of a functioning power plant or manufacturing facility. And it does so in harmony with the private venture capital ecosystem, which stands to benefit at the growth stage from government LP/VC activity catalysing opportunity, and at the early stage from megafunds expanding the aperture of what is fundable by providing downstream capital and exit liquidity.

As the world asks how to rebuild its industrial foundations, we must look at how to scaffold this movement with new financial structures.

You do the investing we’ll do the admin. Start and run your VC firm online. Everything from structuring, capital calls, fund admin, SPV’s and more at your fingertips.

This is very intelligent and well intentioned research. However, we have been living the experience of this in Europe for the past few decades. It runs into serious problems. The short version of these is 3 things:

1. Governments are very bad at choosing which technologies matter and taking a long term view. Money follows an "expert" agenda which depends on the forecasts that sound best to a section of the electorate and high end media. No-one can predicting where innovation is needed least of all governments.

2. Governments are even worse at picking which funds and/ or companies to invest in. The larger the government influence, the less likely that the capital will be well allocated.

3. the whole process becomes bureaucratic and highly illegible. Government adds a burden of compliance and direction that is unworkable. Consequently a significant portion of the money is siphoned off into an ecosystem of advisors and gatekeepers that add no value to anyone.

The amounts of money involved are tiny relative to national budgets. They provide no leverage against bigger electoral priorities - PR window dressing only.

A far better approach is for Government to use its considerable spending muscle and become a good customer for innovative companies. Leave the allocation of capital to the whole spectrum of private funds: yes VCs but also Private Equity, Public Markets, Corporate investment, angels, lenders and the rest. Just because an idea doesn't work for VC, leaves space for other forms of capital. If a genuinely strong investment opportunity exists then shape a new capital instrument to serve it.

Smart in principle. I think the danger lies in how it could be gamed by bad actors and fraudsters.

For example, Capital Pilot tried something relatively similar to the Venture Philanthropy part of this by offering startups an "investability test" that quickly rated their decks and then invested £50k in return for options (admittedly this was SaaS and not deeptech primarily).

Not withstanding their LP not coughing up all the cash, I think the big flaw with their model was shysters learning their criteria and then making up startup pitches to get the funds. I could see something happening like this with the model here.

The other challenge is that most university IP doesn't get funding for a reason: it's junk. Being able to sort the wheat from the chaff is still important, because if lots of junk gets funding, it will take talented human efforts away from the good stuff (in my mind anyway - perhaps this becomes less of an issue as the funding tide lifts and people can start to hop to the best opportunities).