Survival of the Fittest

The path to scaling venture capital must avoid propping up a larger number of marginal companies and feeding fee extraction.

Accelerating the development of technology is a worthy goal. Unfortunately, venture-backed innovation has been notoriously difficult to scale; it’s often said that only a handful of great companies can be produced each year.

This has remained broadly true despite the venture industry growing almost 20x over the last two decades. This expansion has appropriated growth from public markets for a similar number of outcomes, rather than increasing the volume or scope of innovation.

So, how can the venture capital industry actually find and fund more important companies each year, without diluting the overall pool of potential?

As it happens, the friction is a feature.

Scaling Innovation

Imagine you have just been put in charge of your country’s national innovation strategy, with the goal of expanding the technology sector.

You can measure your success along a number of dimensions:

Number of startups created

Volume of venture capital available

Number of startup exits

Total market cap of new technology IPOs

Each one of these metrics, in isolation, creates perverse incentives.

Focusing on the number of startups may raise the number of marginal companies created each year, raising the net cost of failure.

Looking to raise venture capital volume will produce sloppy allocation and weaker outcomes in the long run.

Both number of exits and market cap produce incentives to encourage either faster exits or inflated exits, both of which are a drag in the long term.

Inevitably, you need to take a full systems thinking approach that can proxy the behaviour of a healthy and competitive market.

“Strong interrelationships among the ecosystem elements also reveals their interdependence and need for a systems perspective.”

Entrepreneurial ecosystem elements, by Erik Stam and Andrew van de Ven

Essentially, your goal should be to raise the total market cap of new technology companies → by increasing the number of good exits → which will require more venture capital → which is downstream from the volume of good opportunities.

The key word here is “good”, reflecting the unavoidable nature of qualitative assessment to ensure that marginal companies and poor investment decisions are consistently screened out of the process.

Multidimensional Markets

Venture capital faces the same problem; there are no easy answers to scale if your goal is driving progress rather than expanding fees. Research has consistently illustrated the distortion created when one theoretically positive metric outpaces others.

Lowering the bar for startup formation to increase the number of opportunities does not inherently increase the number of quality companies.

“Policies that reduce frictions to entry can broaden participation and encourage experimentation, but do not automatically generate high-quality outcomes. Achieving top-tier performance appears to continue to depend on the recombination of diverse human knowledge and experience.”

Generative AI Fuels Solo Entrepreneurship, but Teams Still Lead at the Top, by Hyunso Kim, Hyo Kang and Jaeyong Song

A glut of capital tends not to result in greater levels of valuable innovation, but rather more fuel shovelled into the molten core of the market.

“Increases in venture fund-raising which are driven by factors such as shifts in capital gains tax rates appear more likely to lead to more intense competition for transactions within an existing set of technologies than to greater diversity in the types of companies funded.”

Short-Term America Revisited? Boom and Bust in the Venture Capital Industry and the Impact on Innovation, by Josh Lerner and Paul A. Gompers

A surge of exits often doesn’t end up producing enduring value, and may actually represent a distressed environment dumping toxic waste.

“The IPO market has significant time variations over time and IPOs issued during the high-volume period are more likely to have worse performance on average than those issued during other periods.”

Essays On Ipo Cycles And Windows Of Opportunity, by Meng Chen

As an illustrative parallel, research makes the case that startups must scale appropriately along all dimensions to ensure long-term success. It appears that the same is true for the markets they exist in; poorly-balanced scale creates inefficiency that may be exploited by opportunists.

This points to one of the many paradoxes of venture capital; the desire to increase the surface area for opportunity while focusing intensely on the few outliers.

Incumbent venture capitalists and LPs will often warn against expanding the market by introducing more capital or supporting the entry of new firms, on the basis that it simply dilutes the limited set of outcomes.

However, it’s inevitable that great companies are missed each year because the venture market lacked coverage, conviction or originality. Most of venture capital’s great outcomes involve stories of struggling to find willing investors in the early years.

Indeed, as more emerging managers continue to prove their ability to find outliers, it’s harder to make the case that alpha in private markets is running dry.

So, how might these two opposing ideas be reconciled?

Building the Base

One of the findings of research into venture industrial strategy is that there may be easy gains if a government takes on the role of LP to support the entry of emerging managers who invest at the earliest stages.

Institutional LPs are burdened by career-related insecurity, and so bias towards larger established firms that are typically less focused on early-stage companies. This persists despite clear evidence of emerging manager outperformance.

Additional fee-related incentives drive many successful early-stage managers to grow their funds and move to later-stage investing with larger rounds and lower career risk.

As a result, the early-stage foundation of venture capital is often undercapitalised and under-resourced. At the point where it seems most important that investors are prolific, experienced and patient, there is often a shortage of all three.

The interface between capital and talent must be broad. It should cover every corner of the economy and penetrate every sector, in reach of anyone with entrepreneurial ambitions. Fundamentally, this is why early-stage VC should be the domain of many solo GPs or small partnerships who each operate in a variety of ecosystems.

However, as a result of today’s market structure, an increasing amount of early-stage capital is held by a declining number of larger firms. Additionally, each of these firms has narrowed their focus on certain consensus features in order to increase capital velocity. This is entirely opposite to the direction that the market should be moving; the resulting interface is weaker, with worse coverage. It is built on the self-serving idea that founders should pursue investors, rather than vice-versa.

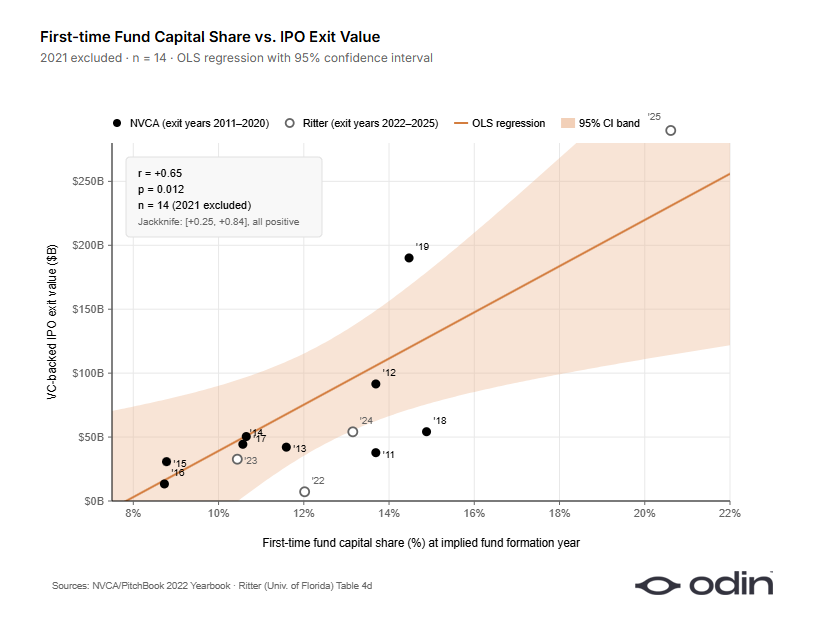

One way to test the benefits of a wider distribution is to analyse years where a larger than usual share of venture capital went to first-time funds, and see if that correlates with increased exit value in the relevant ‘age at exit’ adjusted year.

Essentially, are emerging managers a real driver of future value, through their ability to find a greater volume of generational companies at the earliest stages?

If you exclude the single outlier year of 2021 (where market conditions encouraged a wave of exits), there is a clear correlation between these two factors; a greater number of first-time funds appears to have a positive association with subsequent exit value.

Despite this, research continues to suggest that expansion in the venture market continues to disproportionately favour the already well-capitalised incumbent firms.

Allocators are sacrificing long-term outcomes and technological progress for nearer-term confidence in their decisions and limiting their perceived career risk.

Scaling Conviction

The common resistance to a market with many small firms is the resulting coordination frictions for more capital-intensive companies.

Once again, there is nuance in the market and how it influences investment behaviour.

In hot markets, venture capitalists will often complain about fighting tooth and nail to get allocation. While this sounds desirable from the perspective of coordinating capital, it’s actually reflective of gatekeeping, cronyism and narrower interest in fewer companies that will not necessarily provide better outcomes.

If you talk to venture capitalists in cooler markets, or those who deliberately avoid hotter parts of the market, they tend to have larger networks of coinvestors and more productive relationships. This aligns with research that shows a broader network is more beneficial than a deeper network.

Indeed, analysis by Pavel Prata has found that smaller venture firms have more connections per employee than larger firms, meaning that the greater capital coordination frictions may be less of an impedance.

Research also suggests that there isn’t a huge amount of organisational capital in venture capital, with most value residing in the qualities of individual partners. This has been viewed as an inherent restriction on the size of VC firms, as larger firms dilute the influence of individual partner ability.

“Our findings are consistent with the idea that the organizational capital inside a venture capital firm is limited, in turn limiting firm size. Given this, it appears that brand, process, deal flow, etc. are not critical firm level characteristics, but rather they are partner attributes.”

Is a VC Partnership Greater than the Sum of Its Partners?, by Michael Ewens and Matthew Rhodes-Kropf

Essentially, the argument is that an early-stage market with more individual investors or small partnerships would be significantly more efficient at applying that valuable human capital to find and fund outliers.

The same paper also suggests that larger firms have been formed as a means to reduce their own fundraising friction, rather than in pursuit of stronger performance. In essence, the flawed interface between GPs and LPs is chiefly responsible for the agglomeration that has eroded returns.

“Overall, the results suggest that venture capital partners are often significantly different from each other, but high quality firms are those with a group of better partners. What then is a VC firm? We suspect that the benefits of joining together may relate to fundraising.”

Is a VC Partnership Greater than the Sum of Its Partners?, by Michael Ewens and Matthew Rhodes-Kropf

For growth investment, this dynamic changes. Traditionally, as companies develop more technical proof or traction, they become more legible to investors managing larger pools of capital who are inherently more risk-averse. This is a different class of venture investing, which can operate at a larger scale and with different economics.

The graduation from early-stage to growth capital is a milestone in the maturity of a company, which is later followed by a similar graduation from growth capital to public markets as companies develop strength and become more trusted and predictable. At each step there is pricing tension that keeps the market honest.

However, that chain of events doesn’t always play out so rationally.

The Crooked Pyramid

Disrupting this tidy market logic is the rise of scaled multistage capital.

The first problem is that multistage investors get to mark their own homework. There is effectively no mechanism to keep pricing rational if the same firm can keep leading rounds for as long as an investment remains viable.

“Insider pricing rounds, when financing is led by existing investors, creates a natural conflict of interest; as many times, it’s in the insiders’ best interest to inflate the values. The inflated values allow the investors to show paper gains to their LP’s on their existing investment, which makes their LP’s happy, thereby making the GP happy. This also makes the founders happy as it’s generally easier to raise money from existing investors, and most entrepreneurs feel a higher valuation is better.”

The Growing Ponzi Scheme In Venture Capital, by Jay Levy of Zelkova Ventures

Secondly, and more relevant to the question of scaling the venture market, is the multistage firm’s ability to opportunistically allocate across any stage. Imagine a manufacturer in the middle of the hardware value chain adjusting component volumes based on market vibes rather than predictable order volume.

If a multistage GP feels like the best fundraising story is Seed capital for an emerging wave of AI startups, that’s what they will do.

If a multistage GP feels like the best fundraising story is a growth fund for a more legible set of market winners, that’s what they’ll do.

As a result, the market for capital at certain stages will occasionally expand or contract, leading to the creation or sustainment more marginal companies, or the death of otherwise deserving companies.

All of this creates a more lumpy market with more friction for founders and worse returns for LPs, because those stories are not reality.

In a perfectly rational world, the venture market is formed like a pyramid.

At the base, there are many small firms that pursue diverse idiosyncratic risk by operating on the fringes and investing in the most innovative ideas.

At the top, there’s a small group of more cautious managers with larger pools of capital, who want to help mature businesses transition to public life.

Between the two, the base narrows evenly and proportionally up to the top through intermediate capital providers. It is able to do so efficiently because success at each level creates opportunity for the next.

As a result, there is always a healthy interface layer, and there is always capital to help the best of those companies graduate up through the stages towards an exit.

Unfortunately, venture capital is neither efficient nor competitive. It is needlessly opaque and overwhelmingly driven by shallow signals and cyclical herd behaviour.

So, exits come in waves, with painfully long waits in between, as investors cling to narrative moments that may be exploited for LP attention.

Platform Distortion

Outside of the market structure, there’s a question of the startups within it and how they are shaped by the different categories of investor.

In a market with a larger number of emerging managers, solo GPs and small partnerships, there is likely to be a wider array of more novel and interesting startups in the world.

In a market with fewer, larger firms there is likely to be a much narrower and more internally competitive set of startups that will be centrally located and consensus-themed.

The former will graduate up through the layers of the market more slowly, as novel technology adds risk which may require more patient capital. The latter can move up much more quickly, although that’s largely a function of capital appetite and hype rather than business maturity or fundamentals.

On top of that, the scaled platform firms offer a range of support functions which further warp the outcome by essentially making venture capital less Darwinian.

Consider two rival propositions:

A deeptech company in some frontier category that has just received seed funding from a $5M early-stage solo GP. Each subsequent round will be a battle as the company has to prove itself to each new investor, although the list of GPs in its corner will grow.

A SoMa-based AI startup that has been “kingmade” by a platform firm that will provide them with network connections, support for core functions, social media astroturfing, media connections, a “tier 1” fund brand and the promise of downstream capital.

Which of those two environments is more meritocratic?

Which is likely to ensure capital is consistently allocated to the most important and deserving companies over time?

To repeat a consistent theme in all honest venture market analysis, alpha is implicitly found in the hardest places and least popular ideas. For venture capital to scale effectively, it must do so without losing its Darwinian nature.

It may become larger and more accessible, but the bar must not be lowered.

The Case for Scaling Venture Capital

This all makes the case that scaled platform firms (vertical scaling) are not the answer to expanding the opportunity of venture capital, as they inherently erode the process that incrementally selects for great outcomes.

A more ideal approach would be to scale the number of firms (horizontal scaling) proportionally across all levels. If you want more great exits, you need a greater number of investors at the initial interface layer, and up through each layer above.

Historically, this interface layer has been limited by information friction with LPs, incentive issues related to fee income, and cyclical markets that systematically wash out younger firms rather than the weakest performers. In order to scale venture capital properly, to accelerate the development of technology, these constraints must be addressed through innovation to the venture model itself.

It’s easy to see a future where AI significantly reduces the reporting and compliance frictions between LPs and GPs. In a world with agents, it shouldn’t be significantly more difficult to manage 20 smaller fund commitments rather than 1 larger fund commitment. At some relatively trivial breakpoint the benefit to returns will pay for whatever token burn is required, and it’s a workflow LPs will likely adopt anyway.

The fee incentives in venture capital are plainly broken, protected only by the market capture of the largest firms. It’s reminiscent of how often you’ll hear “top quartile” as the benchmark, when top quartile funds haven’t produced compelling performance since the mid-90s. The industry has changed radically over the last 25 years, and the compensation economics (along with much else) must evolve as well.

The excessive cyclicality of private markets is likely self-correcting if the underlying information frictions and incentives are taken care of. Indeed, many of the problems of venture capital today may clear themselves up with a few structural fixes.

Ultimately, the friction inherent in coordinating capital across subsequent rounds is a feature of private markets, not a bug. It is the mechanism by which marginal companies are systematically and iteratively screened out of the market.

Which is not to say that the market otherwise functions perfectly today, but the remaining issues cannot be properly diagnosed if they are masked by multistage capital.

“While the law [of competition] may be sometimes hard for the individual, it is best for the race, because it ensures the survival of the fittest in every department.”

Run your investment firm from your phone, with Odin

Brilliant....and comprehensive...as usual!