Harnessing Conviction

The challenge of backing emerging managers in venture capital, and the many parallels with early-stage investing

“You know, I think track records are really overrated. Some of Yale’s best investments have been with people that don’t have a track record. We took a couple of people out of proprietary trading at Goldman Sachs 25 years ago. If they had had a track record, it wouldn’t really matter because Goldman Sachs has a very different form of organization and a different way of giving resources to the people that are making investment decisions. But we didn’t even have those numbers. And it was really just a decision that this was a woman and this was a man that we thought were going to produce great returns, and they’ve done a really good job for the university.”

A common perception of venture capital is that of passive limited partners paying sophisticated managers to invest on their behalf. For some parts of the market, this is accurate. Particularly in mature segments, where managers have a clear track record to illustrate their performance and a scaled service designed to meet LP needs.

Where that doesn’t match reality is the emerging manager category, covering the first three funds of a new GP. Here, LPs have to make a judgement on potential that is remarkably similar to that of an early-stage investor. This means understanding all of the same principles of risk, with no shortcuts to success and much greater expected volatility.

Is that extra burden of work worth it? Well, the parallel stretches into performance. As with venture capital, those that embrace risk often reap the greatest reward. Emerging managers not only serve a vital role in the innovation ecosystem, but they also offer strong performance. Indeed, many of the most impressive outcomes have been debut funds.

Opportunities Worth Funding

When evaluating a potential pre-seed investment, there’s little to go on except the combination of the people and the idea. This has been explored by researchers through the lens of entrepreneurs as “designers of problems worth solving”, to encompass both aspects. Extending this concept to emerging managers, addressing the same challenge, they may be viewed as “designers of opportunities worth funding”.

In a practical sense, this means identifying managers who have found a novel way to frame venture capital’s central challenge. Those who understand the mechanics of the industry well enough to have produced a strategy that is differentiated and clever. There must be some reason for LPs to believe it will beat the mediocre median.

The need for this level of qualitative analysis, in both cases, reflects the lack of metrics to examine. The founder offers a proposition with no precedent or evidence, while an early-stage GP offers a portfolio of such propositions. Both are, to some extent, outliers. It is their idiosyncrasy that gives them the ability to build or recognise what others have not or cannot. That is their edge.

The two relationships also share a similar horizon of uncertainty. Until investments turn into realised outcomes, neither the GP nor the LP can be sure that they are making good decisions.

In venture capital, this uncertainty produces predictably bad investments, as investors seek the false confidence of “obvious” signals or patterns. Founders that went to the prestigious university, worked at the right company, or have the desirable personal characteristics. Insecurity encourages decisions that are superficially defensible; a trade-off against the outlier potential that venture capital requires.

“Few data points and long feedback loops make for slow learning, while the extreme uncertainty makes it difficult to learn the right lessons. In this business, it is too easy to confuse luck with skill. Cognitive psychologists Daniel Kahneman and Amos Tversky have shown that humans are prone to thinking errors—cognitive biases—when assessing uncertain events or making decisions in the face of uncertainty.”

Applying Decision Analysis to Venture Investing, by Clint Korover

LPs suffer from the same problem, for the same reasons. The difficulty in selecting managers, combined with the long wait for any validation, results in the same overweighting of superficial traits. GPs who went to the right universities, span-out of the right firms, or have the sheen of a natural salesman. Generally, allocators prefer highly-networked deal-guys with a pedigreed background. Unfortunately the industry is already filled with this archetype, and the data isn’t looking good for them.

Indeed, research shows more diverse investment teams tend to outperform. For example, increasing the share of women on the team by 5 percentage points (e.g., from 10% to 15% female hires) is connected to a 4.7% increase in success rates. Which is not to say that women make better venture capitalists, but merely that the firms which less obviously fit the Patagonia-wearing archetype are more likely to be judged on actual merit. Often held to a higher standard than their peers.

If your job is to identify outliers, which is the case for both GPs and LPs in the emerging manager category, there are no shortcuts. Understanding emerging managers through a qualitative framework like “designers of opportunities worth funding” keeps the focus on useful data, avoiding the comfort of pattern matching.

Alpha Isn’t Easy

As with founder background, or GP profile, the trap of chasing the obvious signals for confidence extends to the thesis itself. Be wary of any manager pitching the easy thing, because generating outperformance is definitionally not easy.

In 1998 the easy thing was an internet firm. In 2026 it might be the physical AI thesis. Capital flows toward the obvious idea because the obvious idea feels easy to price, easy to find downstream investment, and easy to defend if it fails. Critically, it’s far harder to explain why you passed, if it succeeds.

As a result, it takes a remarkably stubborn manager with unusually strong conviction to avoid the gravity of consensus.

“An early rise in market heat often gives rise to herding behavior, both due to resource providers taking others’ actions as credible signals of attractive opportunities and psychological biases toward relying on social proof.”

Windows versus waves of opportunity: How reputation alters venture capital firms’ resource mobilization, by Alicia DeSantola, Pavel Zhelyazkov and Benjamin Hallen

Along the way, a non-consensus founders will see their peers raise money more easily. Non-consensus emerging managers will see peer firms generate more impressive metrics and expand their fee income. Non-consensus LPs will see other allocators celebrating exposure to hot companies and impressive growth in their paper wealth. None of it matters. When it comes to investment, history really only remembers cash returns (or major cash destruction).

This can be a difficult truth to hold onto, because the industry is increasingly built around selling the confidence of simple ideas; whatever it takes to keep the capital flowing, and the party going. Every conversation, podcast or post is either aimed at marketing to LPs or marketing to founders, rather than offering a truthful reflection of the market.

For example, the line that a venture capitalist’s job is simply to “invest in great people” is a wild oversimplification. Any manager who repeats it without caveat or clarification likely hasn’t developed any real conviction of their own. However, as a sales pitch it presents venture capital as a simple product, accelerating capital velocity and reducing scrutiny.

The Persistence Problem

Venture funds are long-dated instruments, and they have been getting longer. The classic ten-year structure has become a twelve to fourteen-year structure once the standard extensions are used, and the time to fully return capital can stretch up to twenty years. The consequence for an LP is that a fund’s interim marks tell you very little about its eventual returns, and aren’t usefully predictive until around year eight.

Even when data on a previous fund is available, it’s no guarantee of performance. Persistence in venture returns is statistically significant, but slight. This is particularly obvious when looking at more recent data, as the expansion of private markets and influx of managers has further weakened performance over time.

Research indicates that top-quartile VC funds repeat top-quartile status ~45% of the time based on fully realised performance data, but only 33% of the time based on data known at the time of investment. This matches with Pitchbook analysis suggesting ~35% of top-quartile funds will repeat their quartile status in a subsequent fund based on the data about one previous fund.

In summary, having a couple of funds that look good based on current marks is a very different proposition from a legacy firm with twenty years of audited outcomes, where track record truly becomes meaningful. Again, this has a close analogue on the other side of the table. The successful serial founder is somewhat more likely to succeed a second time, but not vastly more than first-time founders or those with a past failure.

Fundamentally, an LP evaluating emerging managers is making a forward-looking judgement based on qualitative information, without the comfort of any hard numbers. As with the early-stage VC, this takes conviction and sophistication.

Cheap Talk

“The only thing that matters in this business are actual, realized, and distributed returns to LPs — which is why Sequoia Capital, one of the most respected venture capital firms, specifically tells its LPs to ignore unrealized gains and focus only on the cost of the investments and the actual gains distributed to LPs.”

When Is a “Mark” Not a Mark? When It’s a Venture Capital Mark, by Scott Kupor

There’s a phenomenon in hot venture markets whereby investors are more easily seduced by “cheap talk”, where founders describe huge future growth potential to inflate their ability to raise capital. This sets them on the slippery slope of trying and failing to meet challenging expectations with increasing desperation.

The equivalent of this for an LP results in what the Kauffman Foundation described in their 2012 report as the “n-curve”. Typically, venture fund IRR would produce a j-curve (an initial dip, followed by subsequent growth), but GPs were found to inflate initial performance metrics to meet expectations and make raising subsequent funds easier. Inevitably, those inflated metrics would crash later in the fund’s life, thus the n-shape of the NAV profile.

This deception is a well-studied feature of private markets, covered in a number of studies that show GPs systematically inflating metrics at around the time of fundraising.

“Our results are consistent with GPs managing reported performance in a way that maximizes the probability of raising a follow-on fund.”

Interim Fund Performance and Fundraising in Private Equity, by Brad Barber and Davis Ayako Yasuda

Fortunately, LPs are often smart enough to detect inflated metrics and deceptive GPs are less likely to close a subsequent fund.

“Using a large dataset of buyout and venture funds, we test for the presence of reported return manipulation. We find evidence that some underperforming managers inflate reported returns during times when fundraising takes place. However, those managers are less likely to raise a next fund, suggesting that investors can see through the manipulation on average. In contrast, we find that top-performing funds likely understate their valuations.”

Do Private Equity Funds Manipulate Reported Returns?, by Gregory Brown, Oleg Gredil and Steven Kaplan

This aligns with related findings from 20VC, whose data suggested that managers who were honest and transparent with their reported performance would ultimately deliver the strongest returns.

“The best managers mark down their portfolios fastest. There is a direct correlation between the best performing DPI managers and the speed and accuracy with which they mark down their positions.”

The lesson here for LPs is that strong growth in early marks is not a valuable signal to drive funding decisions without careful scrutiny, and it may even be a negative signal if it reflects managers chasing “hot” investments, rather than good ones.

Certainly, there should be no prejudice against managers whose companies get off to a slow start, as constrained early funding may actually be associated with stronger future potential.

Hyperfluency

There’s a large body of research about what makes a good founder, and identifying good venture investment opportunities, some of which applies to selecting emerging managers through the parallels discussed in the sections above.

However, emerging managers are still operating within a known industry, rather than inventing new categories. Consequently, the risk is lower, the scale of extreme outcomes is smaller, and there’s a little more “ball knowledge” that a prospective manager can be tested on.

This knowledge can be classified in six main areas:

Their approach to origination; sourcing potential investments

What they understand about monitoring and capital formation

How they view capital requirements and constraints

The fundamentals of idiosyncratic and systematic risk

The end-customers of VC (M&A and IPO dynamics)

The trickiest part of evaluating managers on these criteria is that there isn’t necessarily a right answer; idiosyncrasy can’t be scored with a checklist. Instead, the ideal answer is thoughtful, differentiated, and not obviously wrong. Just like startups, there are no patterns that predict success, but there are patterns that predict failure.

To put this in context with an example:

Imagine a hypothetical emerging manager. Someone who recently worked at one of the major AI labs and has now decided they want to pivot their career into venture capital.

They decide to raise a $10M debut fund, with a generalist thesis. They would have an easier time selling LPs on their “access” edge in AI, but they recognise while it’s the frontier today it may not be tomorrow. At $10M, they’re making smaller investments, which many peers warn them just isn’t enough to compete in this market, but they know it’s enough for the startups they’re interested in.

When asked about their fund horizon, they can clearly articulate the bifurcation of companies that will exit earlier versus positions that may be sold to larger firms, allowing a return on capital within the 10-12 years of the fund’s life at a compelling multiple.

When asked about competing against other firms making bigger investments, they explain that more capital doesn’t produce a higher rate of success, and actually it’s often toxic to the development of a startup. A capital constrained business that develops greater efficiency has a cleaner shot at an earlier exit.

When asked about their generalist thesis they can clearly articulate the lessons from past cycles, and the dangers of undiversifiable systematic risk versus the opportunity for alpha in idiosyncratic risk.

When asked about how they source opportunities, they have a clear and unique strategy for origination which includes university networks, online communities and data-driven sourcing tools.

For a new manager, this reflects a thorough understanding of the role of venture capitalist; to find and fund experiments that are relatively cheap and have a huge payoff if they work out. It shows they’re not greedy, and are motivated by returns rather than fees. Finally, it demonstrates they understand market dynamics, exits and the basics of entrepreneurial finance. This level of competence and clarity is what will give them the conviction to take unpopular but highly profitable positions.

For an LP, recognising all of this requires a similar familiarity. Just like screening pitches, it’s not something that should be farmed out to a junior allocator or automated through simple heuristics. However, the more you understand these principles, the more quickly and efficiently you can use them to aid selection.

Human Capital

Beyond the qualitative signals, there is some value in understanding the background of an emerging manager and what it might imply about their potential.

The most common bias amongst LPs is to believe that former founders have a particular edge, having experienced entrepreneurship first-hand. This is what could be called the “player-coach fallacy”, where people assume that the best coaches were former professional players. It turns out, this isn’t true, as they are quite different skill-sets.

There’s a specific study on this question, and how it relates to venture capital, based on analysis of 13,000 firms. Overall, former founders produced a lower rate of success than professional investors. While successful founders outperformed, it’s worth recognising that that group is likely to outperform at anything they attempt.

Another area of interest is the professional background and qualifications of an investor. Here, research from a couple of sources indicates that skills like engineering or law may be helpful in the mix of a small firm, when reviewing certain opportunities. On the other hand, a generic MBA may actually be a negative signal due to encouraging risk aversion. Again, there are no easy boxes to check, but you can consider the background of a manager as a part of their story, to see if it contributes to the coherence of the strategy they describe.

In a similar manner to evaluating founders, the strength of an emerging manager is likely what makes them unique rather than the attributes which fit a pattern. Outlier returns come from outlier people, and it’s the “spiky” qualities which may offer the greatest signal.

Network Capital

It’s often stated that venture capital is a relationship game, and (as we’ve covered recently) these relationships increase the surface area for biases that warp investment decisions.

This spreads up to the LP layer, where an LP is 1.78x more likely to select an emerging manager if there is an existing personal relationship. For contrast, they’re otherwise only 1.21x more likely to invest in a GP with a personal relationship, so this increase reflects the relationship compensating for additional uncertainty.

The paper also finds that an LP is 4.73x more likely to invest in a manager if there has been a prior LP-GP relationship, which reflects the significance of having some historical perspective, even if it’s just a professional relationship rather than performance data.

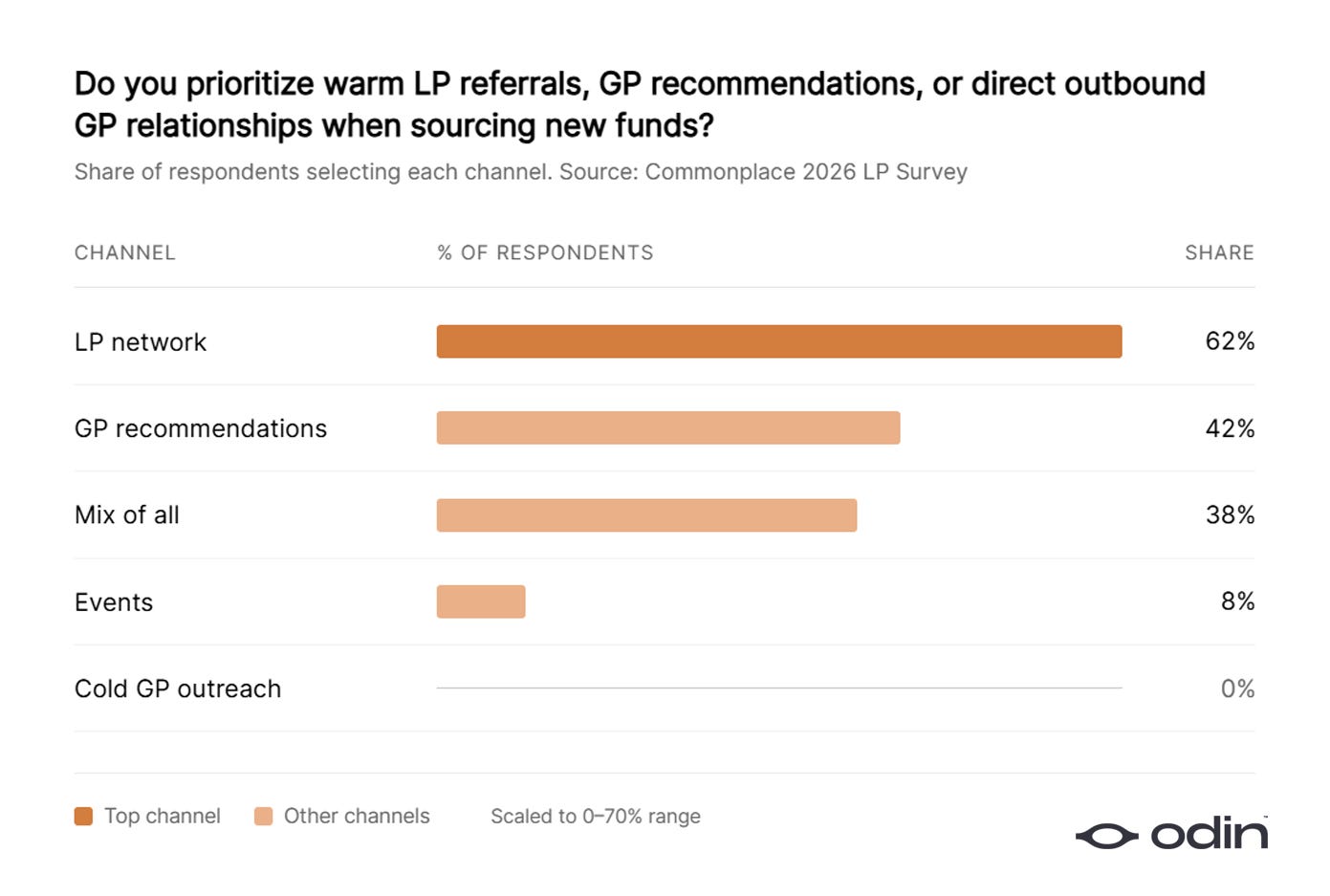

According to a survey by Commonplace, LPs prioritise referrals from within their network when looking for new managers. This is another parallel with the early-stage investor, where there’s a typical preference for referrals from other investors.

Again, there are downsides to relationship-driven investing. Just like the equivalent founders, strong but poorly networked managers (often those from non-traditional backgrounds, underrepresented groups, or outside major hubs) get filtered out early.

So, LPs that focus on leads sourced through their peer network are likely seeing a skewed and incomplete set of emerging managers. The very best opportunities may be invisible unless they actively expand their network or develop other channels.

Finally, while the strength of a manager’s network with other GPs is beneficial, there’s an important nuance to how that network is structured and thus how it influences performance.

Based on the premise that larger, broader networks are beneficial, and deeper relationships are not, relationships begin to look less like a sustainable moat for GPs. Effectively, any manager that builds a large network of other managers with aligned interests (relatively easy if you maintain a good reputation) has theoretically greater potential and less fragility than one leaning on privileged relationships with a handful of “tier 1” firms.

Founder Friendly

Another lens on the quality of managers, also often misunderstood, is founder NPS score. Essentially, how positively do founders rate their investors, and how does this relate to performance? Asymptotically, this might be negatively correlated.

In recent years, “founder friendly” has increasingly meant “moves quickly and doesn’t go hard with due diligence”, as larger firms seek to hoover up more competitive deals and give founders leeway to pursue high-risk strategies for growth.

“To compensate founders for their risk exposure, VCs offer an implicit bargain in which the founders agree to pursue high-risk strategies and in exchange the VCs provide them private benefits. VCs can promise to give founders early liquidity when their startup grows, job security when it struggles, and a soft landing if it fails.”

Risk-Seeking Governance, by Brian Broughman and Matthew Wansley

This direction clashes with past research that connects VC monitoring with a greater rate of innovation and successful startup exits. On the other hand, the recent laissez-faire attitude enables faster growth of paper value, from which founders and investors can enrich themselves through secondary transactions despite weaker ultimate outcomes.

This might explain why data from 20VC indicated a negative correlation between NPS and DPI, as investors who care more about exits might be more hands-on with founders than those just seeking to exploit market failure.

“There is an inverse correlation between the NPs of the manager, and the DPI provided. Most often, the higher the NPs, the lower the DPI, and vice-versa. There are core misalignments between founder and GPs that often aren’t spoken about, but most notably around liquidity timing and availability.”

The lesson for LPs is that, like early markups, NPS (and a general focus on founder friendliness) is not necessarily a positive signal. Just like DPI beats TVPI, successful companies beat friendly founder relationships. Which, of course, is not to say that anyone should be careless with how they treat founders. Wasting a founders time or interfering unnecessarily in their business remain cardinal sins in venture capital.

In summary, managers should understand that their role as a fiduciary means monitoring investments appropriately, and doing what yields the best possible exit, rather than the shortcut of bleeding inflated valuations with secondaries.

Mercenaries and Missionaries

To conclude, another popular framework for understanding founder quality and determination, applied to emerging managers; the mercenaries and the missionaries.

A mercenary will always choose the path that allows them to most easily access capital, whether they are a founder raising from VCs, or a GP raising from LPs. Their major constraint is the friction in that relationship, and they will do everything they can to reduce it, which might mean fitting a certain pattern and offering a certain narrative. Their career risk concerns will lead them to take less idiosyncratic risk (more likely to chase consensus), which will erode the quality of outcomes. They’ll compensate for weaker exits by exploiting inflated NAV for greater fee income and secondary liquidity. Essentially, they are rent-seeking chameleons.

On the other hand, a missionary has by definition chosen to embrace a hard problem, and will find a way to make it work regardless of difficulty. Their major constraint is the time and energy required, and they will do everything they can to maximise output and bring their vision to life. This is sheer determination at work, and it is how new ideas and new technologies are forced into the world. For an emerging manager, this might mean a ramen diet for the first few years while their portfolio slowly demonstrates value that may encourage LP interest. These are the people that venture capital needs more of, to surface the most important opportunities and increase the volume and velocity of profitable exits.

Over the last fifteen years, the market has been shaped by mercenaries to meet the demands of short-term opportunism. LPs would benefit from considering how they can better identify and reward the missionaries, particularly when looking at emerging managers.

It’s not an easy path, but then there’s no such thing if you’re seeking alpha.

Launch and run your VC firm from your phone, with Odin

very interesting! lps essentially making founder-style bets, just with a longer feedback loop. defo a better lens on this than the usual cheerleading 🙌